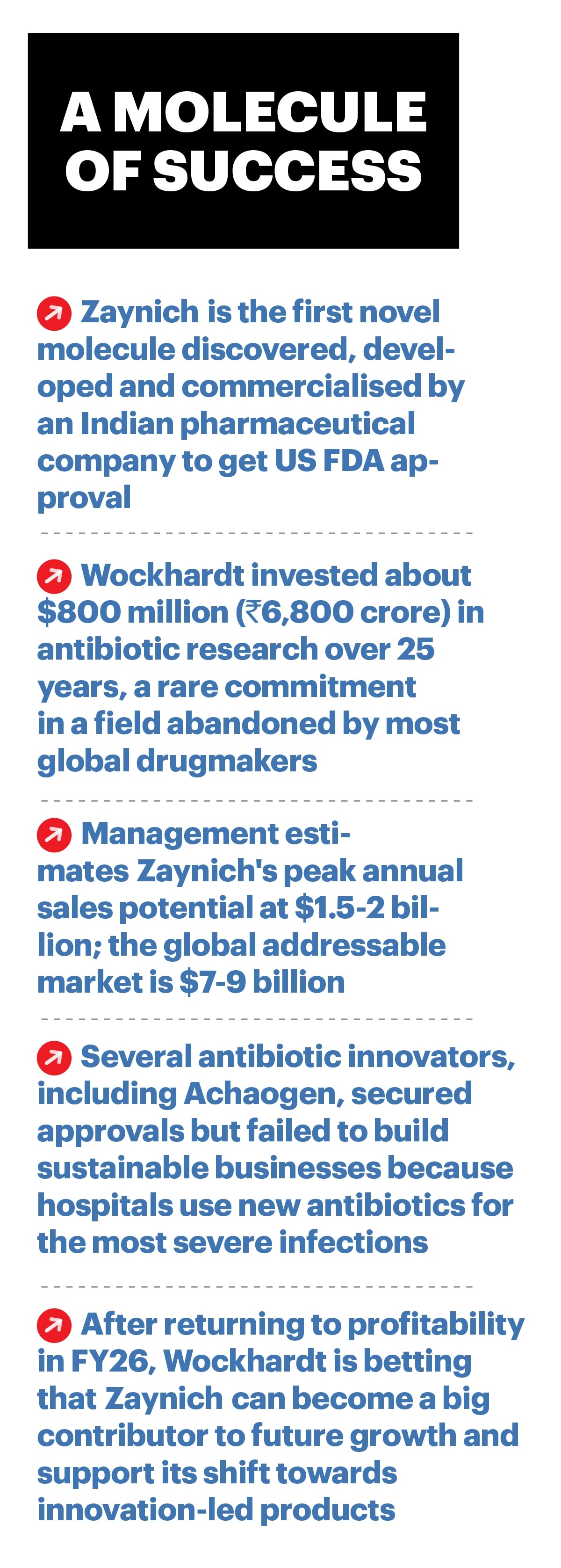

In May 2026, Wockhardt’s antibiotic Zaynich became the first novel molecule discovered, developed and owned entirely by an Indian firm to receive US FDA approval. For an industry that built its global reputation on generics and biosimilars, it was a historic moment. But Habil Khorakiwala, who bankrolled this 25-year programme, knows the harder part is still ahead.

After all, he has just seen the company through one of its toughest periods. Wockhardt returned to profitability in FY26 after years of losses. Debt has been pared down from Rs 3,213 crore in FY20 to Rs 1,859 crore in FY25. The base business—formulations, insulin and UK operations—is stable and growing. Can Zaynich, a novel antibiotic approved for complicated urinary tract infections and designed to tackle multidrug-resistant Gram-negative bacterial infections, be the drug that drives Wockhardt well into the future. Can it justify two decades of investment and make Wockhardt’s turnaround sustainable?

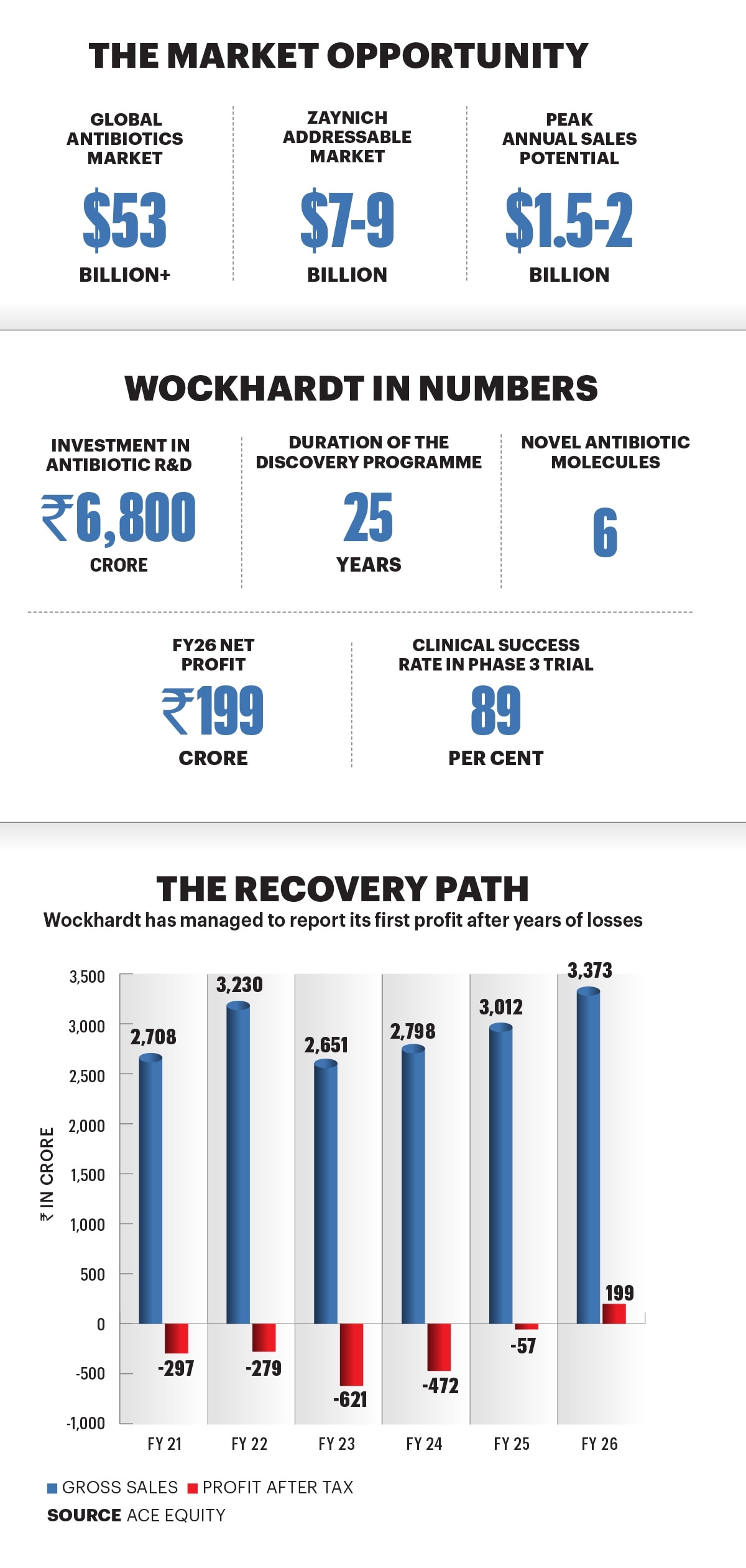

The management has pegged peak annual sales potential at $1.5-2 billion. The global addressable market is $7-9 billion. While these are significant, they are also—as the history of antibiotic launches will attest—numbers that have humbled companies far larger than Wockhardt.

A tough Bet

“Zaynich is the first drug from the Indian pharmaceutical industry to receive US FDA approval after being discovered and developed in-house,” Khorakiwala tells BT. Wockhardt’s decision to invest in discovering the drug came at a time when antibiotic research had lost momentum and many large drugmakers were pulling back from the field.

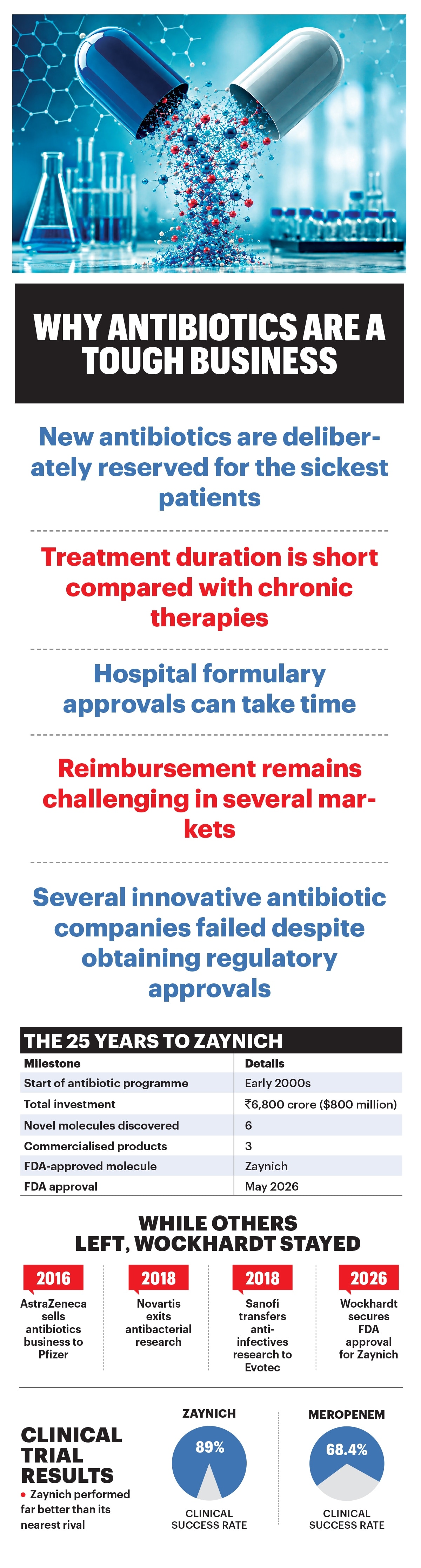

Developing a new antibiotic requires years of investment and involves high risk as the outcome is uncertain. Also, hospitals and physicians restrict the use of new drugs to slow antimicrobial resistance. That is why AstraZeneca sold its antibiotics business to Pfizer in 2016, Novartis exited antibacterial research in 2018, and Sanofi transferred its anti-infectives arm to Evotec. Others redirected resources towards oncology, immunology and rare diseases where potential profits are much higher.

Wockhardt saw the same landscape and drew the opposite conclusion. “It became clear that large pharmaceutical companies were stepping away from antibiotic research. But new antibiotics are still needed because bacteria continue to develop resistance,” says Khorakiwala.

The company invested approximately $800 million, roughly Rs 6,800 crore, in antibiotic research and development over two decades. The programme, led by Dr. Mahesh Patel, Chief Scientific Mentor, and Sachin Bhagwat, Chief Scientist for Drug Discovery, who co-invented the zidebactam-cefepime combination, produced six novel drug candidates after testing thousands of molecules on multiple bacterial targets. Three have already been commercialised: Zaynich, Emrok and Miqnaf. The remaining three, Odrate, WCK 4282 and Foviscu, are at various stages of clinical development.

The troubled Years

The commercial significance of Zaynich is inseparable from the difficult path Wockhardt took to bring it to the market. A series of acquisitions between 2003 and 2009 led to a massive debt burden and, finally, corporate debt restructuring. Then, in 2013, US FDA import alerts shut down the company’s ability to export to its most lucrative market. For years, income from domestic formulations, insulin and the UK business serviced debt, while the antibiotic research programme continued in the background.

“Establishing a drug discovery programme takes considerable time,” says Khorakiwala. “It takes about ten years just to build such a programme across approximately 15 different scientific disciplines. A further seven to ten years is a normal timeline for any pharmaceutical company to bring a drug to approval.”

Zaynich belongs to a new class of antibiotics; new antibiotic classes emerge once in around 20 years. It is designed to treat serious multidrug-resistant Gram-negative bacterial infections, which are becoming increasingly untreatable in hospital settings as existing drugs have lost their potency. The drug works through a dual-action mechanism.

“Competing products exist, but they typically address one or two organisms, whereas Zaynich covers the entire Gram-negative space,” says Khorakiwala. “It kills bacteria rapidly and comprehensively.”

The Phase 3 ENHANCE-1 trial, conducted across 530 patients in 64 hospitals and research centres in the US, Europe, Latin America, China and India, tested Zaynich head-to-head against meropenem, one of the most widely used heavy-duty antibiotics in clinical practice. Zaynich achieved clinical recovery and infection elimination in 89% of patients, as against 68.4% for meropenem.

Drug-resistant infections were associated with nearly 4.95 million deaths globally in 2019, according to the landmark GRAM study published in The Lancet, a figure researchers say has worsened since. The US alone reports more than 2.8 million antimicrobial-resistant infections annually, resulting in over 35,000 deaths, according to the CDC. The FDA had signalled its view of Zaynich’s importance well before approval, granting it Priority Review, Fast Track designation and Qualified Infectious Disease Product status, the last of which also confers ten years of additional market exclusivity after approval, which delays generic competition and extends the revenue runway.

According to the 2026 Antimicrobial Resistance Benchmark, only three large research-based pharmaceutical companies are actively engaged in innovative antimicrobial R&D: GSK in the UK, and Japan’s Otsuka Pharmaceutical and Shionogi. Wockhardt has joined this small group.

The Arithmetic

Strong clinical data has never guaranteed commercial success in antibiotics. For Wockhardt, the history of the field offers both a warning and a benchmark.

American firm Achaogen spent 15 years and $1 billion developing Zemdri for drug-resistant urinary tract infections, secured FDA approval, but filed for bankruptcy less than a year after the launch.

Several other antibiotic innovators have followed a similar trajectory. The pattern is consistent: hospitals reserve newer antibiotics for the most severe infections, treatment durations are short, reimbursement negotiations protracted and hospital formulary decisions slow to move

“The company looks well prepared on the product side, but the next few years will be very important. As the products are launched at a larger scale, especially in the US, execution and following regulations will be the key. The company has taken initial steps by hiring senior people like a CCO, market access lead, and Chief Medical Officer, but how well they execute will be important to watch.”

“In the US, it will need investment in the first three–four quarters and will break even only after that. Also, the management expects revenue growth to be slower than earlier expectations,” says Abhijeet Porwal of Deven Choksey Research. “On the other hand, the UK market looks more stable. The government has already committed to pay GBP 20 million per year for Zaynich, which gives a steady and assured income. This has almost no execution risk. The market may not have fully recognised this yet,” he adds.

Khorakiwala does not dispute the commercial challenge but says the comparison with failed Western antibiotic companies is misleading. "We have invested approximately $800 million for the antibiotics programme and have six drugs to show for it. Developing a single drug at a major pharmaceutical company can cost approximately $2.3 billion. Our approach has been frugal innovation.”

With foundational R&D costs already absorbed into past balance sheets, future revenues from Zaynich will flow at substantially higher margins. When asked whether the economics can work, Khorakiwala is unambiguous. “The molecules they pursue need to generate $1.5 billion to $2 billion in opportunity, which is inadequate for their level of investment and return expectations. For them it is not viable. For us, it very much is.”

For investors, Zaynich is a major value-creation opportunity because the discovery costs are already behind the company. But the market will closely track the pace of US launch, hospital adoption, reimbursement and pricing because the success of the investment will ultimately be measured not by the approval itself, but by the cash that Zaynich can generate over its commercial life.

Rajesh Pherwani, Founder and Chief Investment Officer at Valcreate Investment Managers LLP, says the approval marks the culmination of years of investment by Wockhardt in antibiotic research. “Based on the numbers shared by the company, the potential returns appear encouraging and indicate a significantly shorter payback period from this stage onward,” he says.

Pherwani says Zaynich could benefit from a relatively less crowded innovation landscape in anti-infectives.

The global antibiotics market is valued over $53 billion annually, according to Grand View Research. Khorakiwala says the patient pool for Zaynich in India runs into hundreds of thousands, a significant opportunity that sits alongside the far larger US prize. “India is a very important market from a business point of view as well,” he says. Europe, where the European Medicines Agency has granted Zaynich accelerated assessment status, adds a further $400-500 million in potential peak sales.

The Launch Plan

Wockhardt is targeting a US entry by end of 2026 or early 2027. It is going in independently, a strategic choice that reflects confidence in its commercial capabilities and a determination to retain the full value of what it has built rather than licensing it away.

The US team is led by Zahabiya Khorakiwala, who currently oversees the group’s hospital segment.

For capital-intensive operational functions, the company is working with external partners while keeping commercial strategy and leadership in-house. Supply for US will target European markets through third-party contract manufacturers, specifically in Italy, whose facilities were reviewed by the FDA as part of the approval process. Khorakiwala notes that manufacturing from Europe also shields Zaynich from potential US tariffs on Indian pharmaceutical imports. “We are partnering with a company for capital-intensive areas, while keeping the intellectual work and leadership in-house,” says Khorakiwala. “The product should be available in the US around the first quarter of 2027.”

In India, Zaynich will be marketed directly through Wockhardt's existing anti-infectives field force, with launch expected around December 2026 or January 2027. Pricing will reflect the public health imperative, at 15-20% of US levels, where a 7-10-day course costs between $10,000 and $15,000. “India will be priced at an 80% discount to that,” says Khorakiwala.

While Zaynich is commanding all the attention, it has not yet generated a single rupee of revenue. The business sustaining Wockhardt through this transition is its pharmaceuticals operation across India, the UK and Ireland.

The UK business is the largest by geography, contributing 39% of consolidated revenues and growing 13% year-on-year. Ireland’s Pinewood Healthcare contributes a further 11%.

Together with India formulations, biotechnology products and insulin, this base business contributes roughly 75% of consolidated revenues and generates the stable, predictable cash flows that have funded innovation without requiring sustained external capital. EBITDA margins expanded to 18.7% in FY26 from 13.8% in FY25, driven by the exit from loss-making US generics, better supply chain efficiency and the shift towards higher-margin products.

What Comes Next

Khorakiwala says Zaynich is the opening of a new chapter. Zaynich, WCK 6777, a once-daily injectable antibiotic that has already completed Phase 1 trials in the US, is being developed for the outpatient treatment market, a segment that could prove even larger than the hospital market Zaynich is targeting.

The management is targeting revenues of Rs 6,000 crore by FY28, rising to Rs 12,000 crore by FY31, as against Rs 3,373 crore in FY26. Achieving these will depend on how quickly Zaynich gains traction in the US market.

“We are actively transforming ourselves into a more research-based company,” he says. “This is not a one-product story. A number of products are already in the pipeline globally, and our investment in antibiotic research will continue. We see clear white space globally.”

The first quarter of 2027, when Zaynich is expected to begin reaching American patients, will be the moment the financial community starts forming its view. Market access negotiations, formulary placements and the pace of hospital adoption across the United States will test whether Wockhardt’s commercial organisation is as capable as the scientific one that built the drug. The drug works. The FDA agrees. Whether the balance sheet follows is what the next three years will determine.

@neetu_csharma