In a Jan Aushadhi store in Patna, Bihar, a strip of paracetamol costs Rs 3. An antibiotic course that might cost several hundred rupees at a private pharmacy is available for a fraction of that amount.

The government’s generic medicine network, which has crossed 10,000 stores, has become one of the most visible symbols of India’s healthcare ambitions by bringing medicines within the reach of millions. The medicines may be inexpensive, but the raw materials used to make them are heavily imported, largely from China.

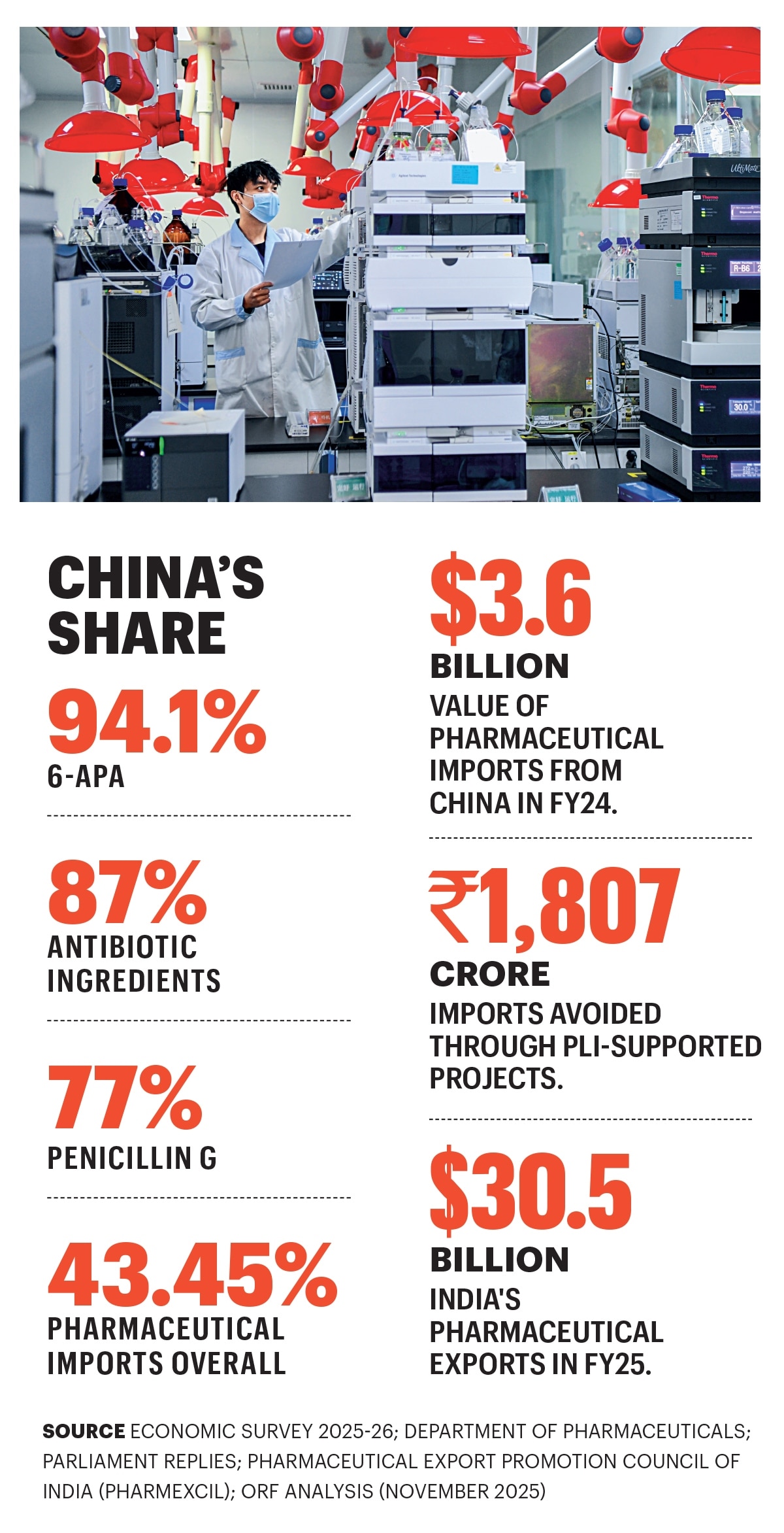

India supplies generic medicines to more than 200 countries. Pharmaceutical exports reached $31.1 billion in FY26, 16 times the $1.9 billion in FY01. But this has been accompanied by a worrying rise in raw material imports. Industry estimates suggest that 70-80% active pharmaceutical ingredients (APIs) used by Indian pharmaceutical companies are imported, with China accounting for the bulk of those supplies.

“China operates massive, fully depreciated mega plants and controls the basic upstream chemicals. Domestic key starting materials and intermediates remain significantly more expensive. As a supplier of affordable medicines, Indian pharma cannot sacrifice its cost competitiveness. Until it builds a fully integrated ecosystem, from basic raw materials to cheap utilities, the reliance on imported inputs will remain an economic reality rather than a choice,” says Salil Kallianpur, pharma analyst and former Executive Vice President at GSK. China accounted for 43.45% of India’s pharmaceutical imports by value in 2023-24, amounting to $3.6 billion, according to the Pharmaceutical Exports Promotion Council.

For some products, the dependence is deeper. Government data shows that Chinese imports accounted for 77% of India’s Penicillin G imports in FY24. For 6-APA, a critical antibiotic intermediate, the figure was 94.1%.

Why the Dependence?

Over three decades, Indian pharmaceutical companies, operating in highly competitive markets, turned to lower-cost Chinese suppliers. As Chinese companies scale up and integrated chemical manufacturing ecosystems, supported by cheaper utilities, infrastructure and financing, importing APIs became more economical than making them domestically.

COVID-19 exposed the vulnerability of the model. Supply disruptions and export restrictions pushed API security higher on the policy agenda. “India’s pharmaceutical industry is uniquely positioned to strengthen its global leadership by progressively reducing supply chain dependencies,” Rajesh Agrawal, Commerce Secretary, said recently.

APIs, however, are one part of the picture. Every API begins much earlier with chemical intermediates, key starting materials and specialty chemicals. China’s advantage extends across this entire chain. Large industrial clusters bring together multiple stages of production, creating efficiencies in logistics, scale and costs. In India, much of that ecosystem is fragmented, says Kallianpur. As a result, even when an API is made in India, a substantial portion of the upstream supply chain may originate abroad.

Industry executives say API production alone will not solve the problem. An Indian manufacturer receiving incentives to produce a critical antibiotic API may still rely on imported intermediates for raw material.

The challenge extends to the wider chemicals industry too. India is strong in areas such as agrochemicals, dyes and dye intermediates. Yet, it imported chemicals worth more than $54 billion in FY25, according to industry estimates. The domestic chemicals market was around $250 billion in 2024. The dependence is particularly high for pharmaceutical intermediates and key starting materials. Industry assessments indicate that critical products such as paracetamol, ibuprofen, clavulanic acid, penicillin G and amoxicillin continue to rely heavily on imported intermediates and raw materials, with dependence ranging from 50% to 80%.

A China+1 Opportunity?

Global supply chains are being reassessed. The United States has taken steps to reduce dependence on Chinese pharmaceutical supplies through measures such as the BIOSECURE Act and a 2025 executive order calling for a Strategic Active Pharmaceutical Ingredients Reserve. Europe is pursuing similar objectives through the Critical Medicines Act.

India supplies 65-70% of WHO vaccine requirements and hosts one of the largest networks of US FDA-approved manufacturing facilities outside the US. The country is also home to 10 of the world’s top 25 generic pharmaceutical companies, according to the government.

“When we say we are the pharmacy of the world, it’s not rhetoric. In the US, 60% of the medicines consumed are made in India, and the same holds true for many other markets,” says Sharvil Patel, Managing Director, Zydus Lifesciences. He calls for greater localisation of supply chains. “Companies must indigenise certain capabilities and build supply chains within key markets to reduce external dependencies,” he says.

Global customers looking to diversify away from China are increasingly examining supply chains in their entirety rather than focusing only on where the final product is made. “Indian pharmaceutical companies are expanding beyond traditional markets, building a strong presence across emerging geographies while reinforcing their foothold in regulated markets,” says Namit Joshi, Chairman, Pharmexcil. An Indian supplier heavily dependent on Chinese intermediates may not be able address those concerns.

The industry’s ambitions remain high. Piyush Goyal, Union Commerce and Industry Minister, said recently that India’s pharmaceutical sector, currently around $60 billion, is poised to double within five years. That growth is expected to increase demand for APIs, intermediates and key starting materials.

Growing demand is one reason. Another is more patients entering the formal healthcare system through schemes such as Ayushman Bharat. The Jan Aushadhi network continues to expand. Hospital infrastructure is spreading across Tier II and Tier III cities. Each of these developments will increase demand for medicines and, in turn, the ingredients needed to manufacture them.

A COMPLETE SUPPLY CHAIN

The government responded in 2020 with launch of the Production Linked Incentive Scheme for bulk drugs, backed by an outlay of Rs 6,940 crore. The programme targeted 41 strategically important products and was complemented by plans for bulk drug parks in Andhra Pradesh, Gujarat and Himachal Pradesh.

According to government data, manufacturing capacity has now been created for 26 key starting materials and APIs. Among the most closely watched projects were facilities producing Penicillin G in Kakinada and Clavulanic Acid in Nalagarh. These were not produced in India for more than two decades.

“The PLI Scheme is a step in the right direction, but financial incentives alone cannot instantly erase China’s structural advantages,” says Kallianpur.

Even as domestic capacity expands, imports continue to rise. Pharmexcil data shows bulk drug imports during the first two months of 2024-25 increased 13% compared with the corresponding period a year earlier.

Import growth has broadly kept pace with export growth. Between 2001 and 2024, exports of finished medicines climbed from just over $1 billion to about $23.3 billion. Imports of APIs and intermediates rose from roughly $1.8 billion to nearly $26 billion, according to Trade Map data analysed by ORF.

India has established itself as the pharmacy of the world. Whether it can reduce its dependence on imported ingredients may determine how secure that position remains.

@neetu_csharma