It’s been a difficult four months since the US and Israel attacked Iran on February 28. India may have started the crisis from a position of strength and enjoyed a brief Goldilocks moment of high growth and low inflation, but the ensuing days have thrown up unforeseen challenges for both policymakers and industry.

The closure of the Strait of Hormuz choked not just crude oil flows but also impacted import and export of critical raw materials and finished goods. Together, these cast a shadow on global growth prospects and fuelled inflationary pressures. The volatile geopolitical environment also led to a flight of capital and was partly responsible for the sharp depreciation of the rupee and challenges of the current account deficit.

Though the interim peace deal between the US and Iran in June has led to resumption of shipping through the Strait of Hormuz, the mood remains grim amid concerns about the longevity of the peace deal and questions over how long it would take for supply chains and prices to normalise. Meanwhile, the prospect of a super El Niño resulting in deficient rainfall this year and affecting the agrarian economy is cause for further worry.

This mood of pessimism pervaded in the BT-C Fore Business Confidence Survey of 500 CEOs and CFOs for the second quarter of financial year 2026-27 (Q2FY27).

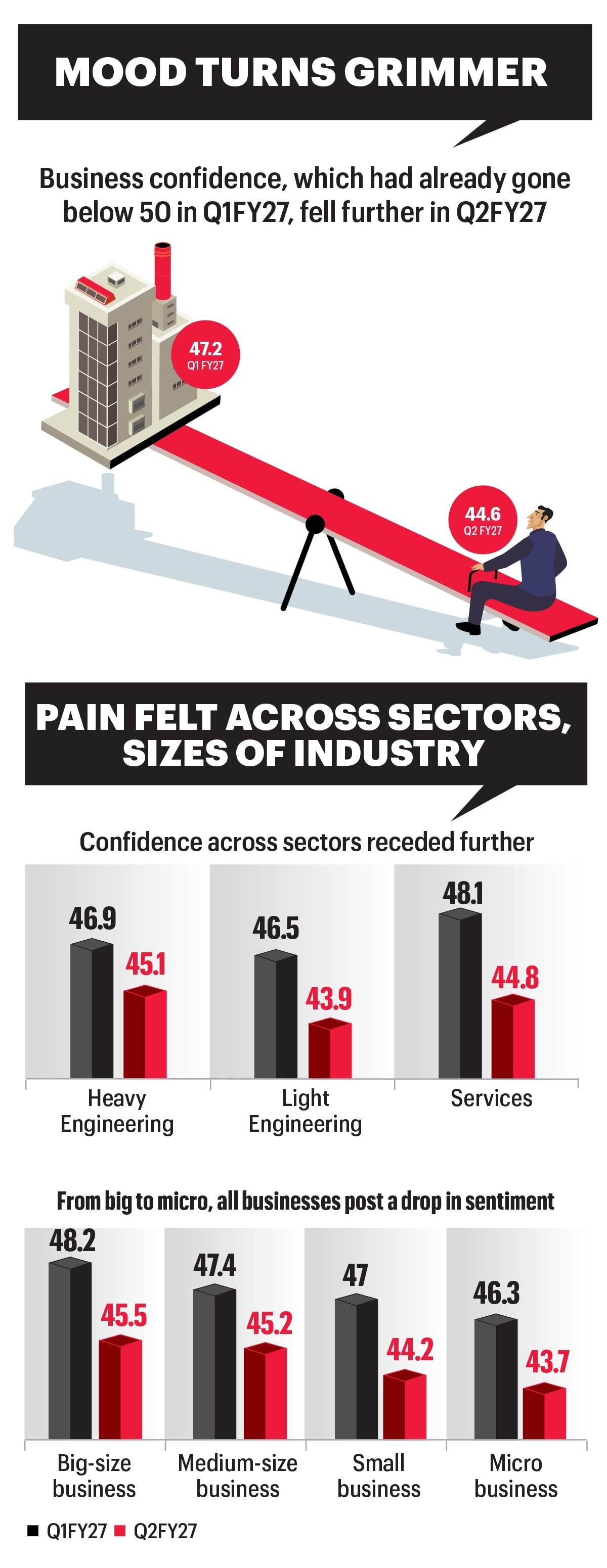

The Business Confidence Index (BCI) contracted to 44.6 for the July–September quarter on a scale of 100, down from 47.2 in the previous quarter. A reading below 50 shows that sentiments have soured and are in the red.

Though not exactly comparable with earlier data because the BCI was revamped in the previous quarter to reflect views on the upcoming quarter, a quick scan of historical data shows that the confidence score for Q2FY27 is the third-lowest since the survey began in 2011.

Prior to this, the BCI was at a record low during the Covid-19 pandemic with a reading of 43.2 in the April–June 2021 quarter and 43.8 in the October–December 2020 quarter.

The latest survey was conducted between June 2 and 13, right before the peace deal between the US and Iran was firmed up, but it revealed that the outlook across business sizes and sectors had turned bleaker in Q2 compared with Q1.

Amongst sectors, light industry—comprising food products and beverages, textiles and furniture, amongst others—registered the lowest confidence at 43.9. In terms of size of businesses, micro industries remained the worst impacted with a reading of 43.7 for the second quarter of the fiscal.

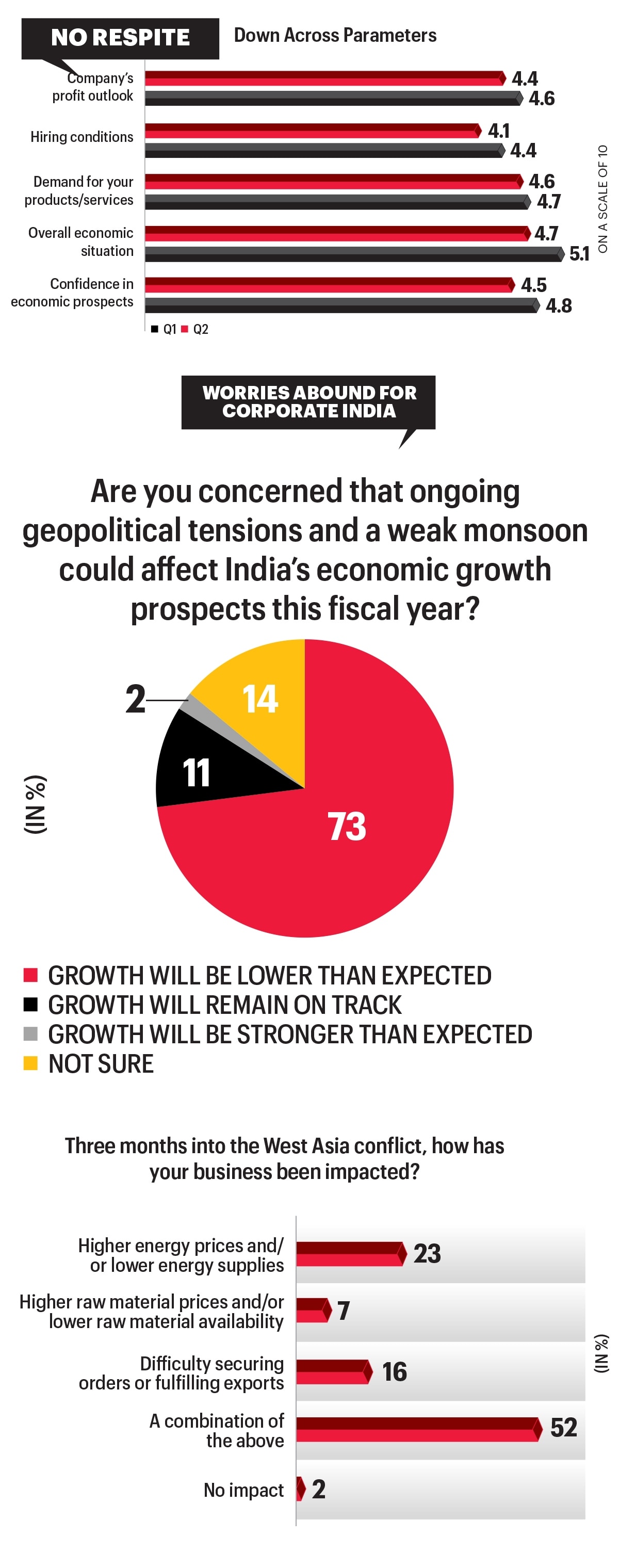

Since businesses were less confident about Q2 than the preceding quarter in terms of economic outlook, consumption demand and profits, their hiring plans for Q2 were also muted.

Woe of Aftermath

Discussions with industry sources and experts indicate that while the war may have ended, Q2 will remain challenging for companies as they battle price rise and wait for supply chains to return to normalcy.

The US and Iran signed an initial peace deal on June 17 with a 60-day time-frame to negotiate a final deal. The war has halted for now, with occasional violations, and the Strait of Hormuz has opened. Crude oil prices, which had surged to over $120 per barrel, have cooled to pre-war levels and Brent crude price fell to around $70 on July 2. Qatar plans to restart and ramp up its LNG production to full capacity. For India, all this translates into lower prices and easier supplies. That will help reduce pressure on the current account and fiscal deficits and, perhaps, ease inflation.

The rupee has strengthened as a result of the ceasefire and a slew of measures announced by the Centre to boost foreign investments in government securities.

Madan Sabnavis, Chief Economist of Bank of Baroda, notes that everybody seemed to have been cautious in Q1 and nobody wants to invest as of now. “El Niño will impact incomes and ability to spend. Everybody is in a wait-and-watch mode,” he says. Much of the corporate outlook for Q2 will also depend on the Q1 performance. While conditions have begun to normalise, a full recovery is likely in the second half of the year.

In its Economic Outlook for FY27, Bank of Baroda pegged GDP growth at 6.4-6.6% and inflation at 5-5.2%. “The impact of the war will be felt for the next six months,” said the report released on June 24. It assumed that oil price will average $80–90 per barrel in FY27.

Government sources underline that the economy is still robust and domestic demand remains strong, as is evident from indicators such as bank credit, GST collections and UPI transactions. Revisions of estimates of GDP growth, inflation and deficits will be undertaken later in the year when the situation further stabilises.

For now, the Reserve Bank of India has pegged GDP growth at 6.6% this fiscal and inflation at 5.1%, although expectations are that both could be higher than that.

On the domestic front, the strength and distribution of the monsoon is being closely monitored by policymakers and firms to get a pulse of rural households.

Rumki Majumdar, Economist at Deloitte India, says India is likely to see a slow transition to normalcy in Q2FY27 as the impact of the peace deal slowly sets in. Volatility with respect to commodity prices, supply constraints, and rupee valuation will likely subside, she says. Overall, prices may see some elevation due to the lagged effect of the war, the impact of supply disruptions on input prices for Indian manufacturers and the slower recovery of crude oil prices, as several countries will rebuild their exhausting reservoirs.

One of the biggest downside risks would be the impact of El Niño and poor monsoon rains on agricultural output. A rainfall deficit will impact crop production and livelihoods of farmers, she notes.

“Overall, confidence of corporates may remain muted in the short term and businesses will remain cautious for the next six months or so. Concerns over US tariffs also continue until a trade deal is finalised and signed,” says Majumdar.

The Forecast

These concerns were also evident in the responses of companies to survey questions about the challenges they face at present and their plans for the future.

The war impacted almost all businesses in some form or the other. As the conflict continued past the three-month mark, 52% of businesses reported that they faced a combination of challenges emanating from it, including higher or lower prices and supplies of energy and raw materials and difficulty in securing orders or fulfilling exports. Only 2% of respondents said their business was not impacted in any manner by the war.

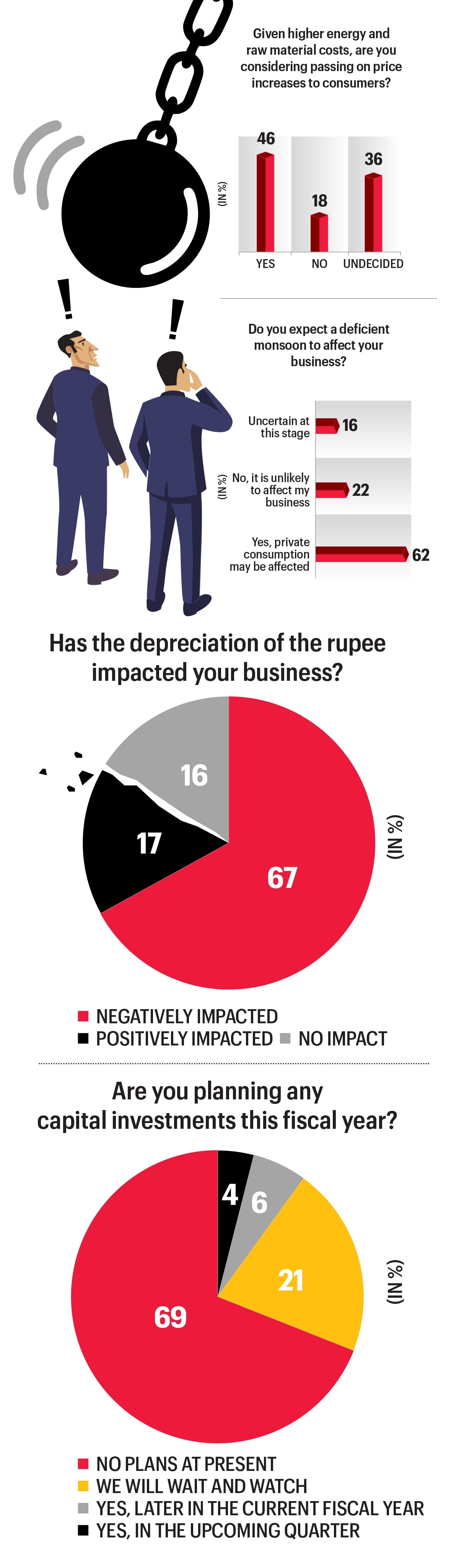

Faced with higher energy and raw material costs, 46% of businesses are also considering passing on price increases to consumers, though 36% remain undecided.

The depreciation of the rupee, which slumped to a record low of 96.9 in late May, negatively impacted 67% of businesses polled, although 17% said they were positively impacted.

As many as 73% of respondents believe that geopolitical tensions and weak monsoon would impact the country’s economic prospects this fiscal, and 62% feel that a deficient monsoon would impact their businesses as private consumption would be affected.

No wonder capital investment plans by India Inc also seem to be on hold. When asked if they are planning any capital investments this fiscal, 69% of respondents said they had no such plans at present, while 21% are in a wait-and-watch mode. Only 4% of respondents are planning investments in Q2, and 6% later in the current year.

A big shift in the current unpredictable environment is unlikely in the immediate future. However, there are expectations that this will spur the government to implement more reforms as it tries to bring foreign investor interest back to India.

Plus, the operationalisation of several of India’s trade agreements may bring new opportunities, while the interim trade pact with the US—if it is finalised—would lift sentiments as well. The free trade pact with Oman that came into effect on June 1 has already opened new routes and ports for India’s exports to West Asia and other parts of the world. Now, the operationalisation of the UK trade deal on July 15 will also bring a new market for Indian goods and services.

Hopes are pinned on Q3 being better as it ushers in the traditional festive season that sees higher demand and leads to more production and hiring by companies and fires up the economy’s growth engines.

But for now, it is still red alert!

@surabhi_prasad