Drive a Jaguar or a Land Rover made of Corus steel—that’s the message the Rs 2,51,543-crore (by revenues in 2007-08) Tata Group sent out to Old Blighty when it struck up a price tag of almost $16 billion to buy two UK businesses in a span of a little over a year, between January 2007 and March 2008.

For a while, the Tatas were globalisation’s biggest disciples and their logo a badge of pride on the sleeve of the patriotic Indian. Then came the global downturn. Stock prices came crashing down, making yesterday’s buyouts suddenly look obscenely dear, prices of many of the products (like steel) of the acquired companies slipped, and the debt resorted to fund these buyouts threatened to burn holes in the balance sheet.

Analysts estimate the debt of the Tata Group at a whopping Rs 1,00,000 crore; although they did term it ?gmanageable?h, the figure in isolation is enough to drive investors.and financiers.into a blue funk. At present, Tata Motors is scouting around to refinance $2 billion of loan taken to acquire Jaguar-Land Rover (JLR) by June. A small stake in Tata Consultancy Services has already been liquidated to generate some funds. Last month, Standard and Poor?fs (S&P) downgraded the company?fs credit rating to B+ from BB-, on concerns of deteriorating cash flows and significantly high debt levels. As for Corus, reports indicate that a major restructuring is on the cards, with the future of plants in Spain, the Netherlands and France being reviewed.If “go global” was the rallying cry for India Inc. in the boom years, then “hunker down” is the motto of today. Digesting the mega deals stitched in the boom years is turning out to be more difficult than anticipated. And it’s not only the Tatas; a host of other corporations are struggling to cope with their multibillion-dollar baggage. Consider:

As large Indian companies scramble to refinance and repay the debt taken to buy overseas companies, the archetype of the ambitious Indian overseas acquirer seems gloriously undone. Many of these deals were premised on plentiful liquidity, the India story continuing to shine and the world continuing to consume more products and services.

So what happened to India Inc.’s big slayers? Did they fall short in terms of scenario planning? Was India Inc. too aggressive in the valuations then? Some of the big deals, especially in 2008, were certainly at top-deck valuations. Says Debu Bhattacharya, Managing Director, Hindalco Industries: “The changes caused by the global economic meltdown are well beyond the ‘contingency adversities’ that we had planned at the time of valuation.

R.S. Butola, Managing Director, ONGC Videsh, concedes: “In hindsight, financial logic went against us.” However, he also adds that when you are acquiring assets of this kind, you have to take a threeyear call on what will be the prevailing price then, based on prospects. “Production is still small and needs to be ramped up. The possible reserves with this company are very high.” Butola’s point is that the strategic logic of the Imperial deal remains intact.

That is also the case with Novelis, which controls 19 per cent of the world’s flat-rolled aluminium products. “Yes, it was an expensive buy in 2007, but it was worth the price paid. If we were to recreate assets of the kind and size as Novelis, it would cost us much more than the $6 billion we priced it at. And, it would take years to get the assets produce the same quality and cater to the wide and large customer base that Novelis has,” explains Bhattacharya.

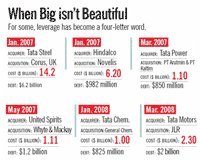

What went wrong

|

“In capital structures that relied on shorter duration funding and with little equity, in the current economic scenario there is almost no elbowroom for manouevre,” says Aditya Sanghi, Managing Director, Investment Banking, YES Bank. More damaging, perhaps, has proved the over dependence on bridge loans—interim financing until a more permanent route is found—resorted to by almost every one. “If there are any lessons learnt from the mega deals it is this: longterm funding should be tied up as soon as possible,” says Sunil Mehra, Managing Director, Corporate Finance and Advisory, Standard Chartered Bank.

However, no amount of right financing structures could have helped if the underlying financial logic was flawed. Ashutosh Agarwala, CFO, Strategic Finance, GMR, says that even if the asset has been overpaid for, and there is leverage, what is perhaps not sustainable is a situation “where the balance sheet of the acquiring company is continuously getting loaded by additional commitments in order to repay the acquisition-related commitments”. GMR, which acquired a 50 per cent stake in Dutch power utility InterGen for $1.1 billion, closed its deal financing last October. “It was important to make sure that the valuations are aligned to the most conservative scenario and that the risk is ring-fenced,” he adds. Much will depend on how corporate India handles the risk associated with buyouts in subsequent quarters. And therein will lie the tale of the winners.