A sombre silence fills the ninth floor of the

DLF Centre building on the bustling Sansad Marg in New Delhi. It's clearly not business as usual at the corporate headquarters of India's largest real estate company, which is at the centre of a political storm. A huge M.F. Husain mural adorns the dome-like ceiling above the entrance.

The art, based on the urban landscape of the national capital, reminds visitors of the company's long-standing ties with the city from which it derived its name (Delhi Land and Finance) and much of its early fortune. The building houses the office of Rajiv Singh, DLF's Vice Chairman and son of its founder, K.P. Singh.

Singh is an embattled man these days. His company's

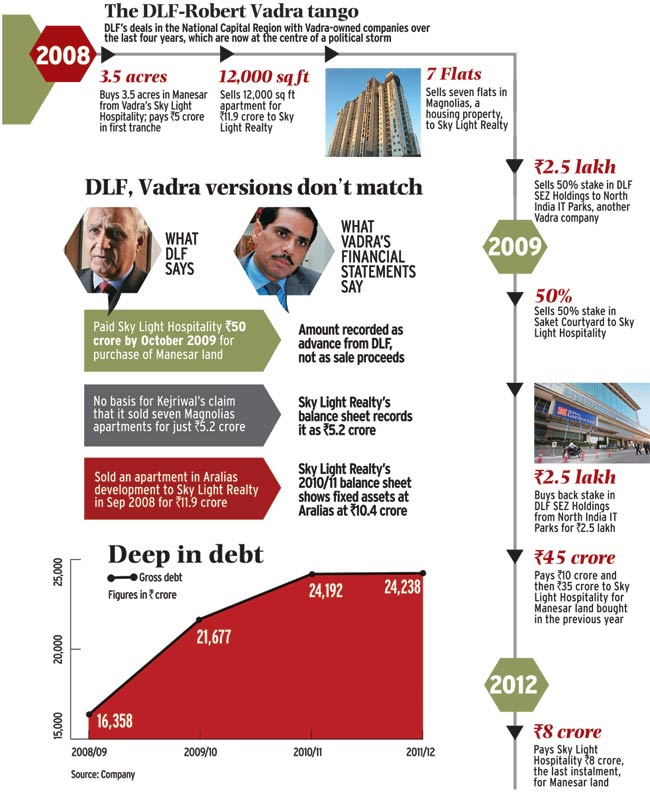

business dealings with firms promoted by Robert Vadra , the son-in-law of Congress chief Sonia Gandhi, have been portrayed as an example of crony capitalism by newly minted politician Arvind Kejriwal.

But these allegations are perhaps not the 53-year-old scion's worst headache. His

company is deep in debt. As of June 30, 2012, gross debt stood at Rs 24,259 crore - nearly 2.4 times the total income and 20 times the net profit of the last financial year. In fact, the debt climbed steadily over the past four years.

Rising debt translates into higher interest outgo. An analysis of the last financial year's performance shows that DLF's operating cash flows were Rs 2,492 crore, and the interest outgo was Rs 3,013 crore, which means that interest payments added up to Rs 521 crore more than the cash generated from operations. In addition, the company spent money to acquire land and on capital expenditure, which increased overall debt.

"DLF's core business is not generating enough cash to meet debt obligations, which is a big concern for us," says Kejal Mehta, analyst at Mumbai-based brokerage Prabhudas Lilladher.

"There has been no capital formation from DLF in the past few years," says Ambar Maheshwari, Managing Director (Corporate Finance), Jones Lang LaSalle India. "All its income generation is going to pay off interest to banks." It is at this crucial juncture that DLF finds itself in the middle of a political storm, with Kejriwal alleging that deals between Vadra's companies and DLF were not above board. This is not the first time DLF's corporate governance has been questioned, but the timing could not have been worse.

There are inconsistencies between DLF's initial media statements about the value of its deals with Vadra's companies, and what the financial statements of the companies show. DLF declined to respond to emailed questions about the inconsistencies.

So far, there has been no announcement of investigations into the nature of the deals, but the issue is unlikely to subside quickly. About 10 days after Kejriwal's press conference where he made the allegations, Haryana bureaucrat Ashok Khemka publicly expressed doubts about the legitimacy of one of the transactions.

DLF has already had one brush with a regulator. In August 2011, the Competition Commission of India (CCI) fined DLF Rs 630 crore on charges of abusing its dominant market position. DLF got a stay order from the competition tribunal against that order.

In March this year, Canadian firm Veritas Investment Research released a scathing report on DLF, claiming that its accounting policies were "conflicting" and aggressive. The report said that "we do not believe the disclosed book equity and asset base. We believe that via its dealings with DAL, from financial year 2006/07 to financial year 2010/11, the company inflated sales by at least Rs 11,236 crore and its profit before tax by Rs 7,233 crore."

DAL refers to DLF Assets Ltd, which was owned by the Singh family. In June 2007, DLF came out with a Rs 10,500-crore initial public offer (IPO), which made K.P. Singh the world's richest real estate baron. Soon after that, investors lost interest in the company. Within a year of listing, the stock price fell below the issue price of Rs 525 a share, and never reached that level again. Since the IPO, the stock price has declined 62 per cent, compared with a 41 per cent gain in the BSE Sensex.

The trouble at DLF began in 2009, when the company decided to merge DAL with itself. DAL was buying commercial property from DLF and collecting lease rentals from those properties. DAL was floated with the intention of listing it on the Singapore Real Estate Investment Trust (REIT) market. But that didn't happen, as the property market crashed globally. DLF later bought DAL at a much higher valuation. K.P. Singh is known in the industry for his strong business acumen.

When he first set his sights on Gurgaon in 1979, he had the colossal task of acquiring huge amounts of contiguous land. Besides, he had to deal with dozens of outdated and illogical laws.

"When I set out to buy land in this area, I was firm that we would not take the farmers for a ride," he writes in his autobiography titled Whatever the Odds: The Incredible Story Behind DLF. "The acquisition meant dealing with 700-odd families each with five to six members." He went on to say that it was difficult to persuade the Ahir community, which owned most of the land, to sell it, as "there was absolutely no culture in the community of selling land".

Singh adds: "We told them we wanted land for developing a city and asked them to invest the money in DLF and become partners with us. There were times when we bought land, handed over the money and then got them to give it back to us as investment on the same day. We offered them an interest of 12 per cent which was substantial money for them and higher than what banks were offering."

Times are tough again for DLF. Operations are lacklustre, and the need to service debt is making things harder. The company's strategy for getting out of the fix it finds itself in is to sell some non-core assets. In June this year, it divested its stake in subsidiary Adone Hotels and Hospitality for Rs 567 crore. This was followed by the sale of 17.5 acres of National Textile Corporation (NTC) mill land in Mumbai for some Rs 2,700 crore to Lodha Developers.

There are more sell-offs in the offing, such as luxury hotel chain Aman Resorts, and windmill units in Gujarat, Karnataka, Rajasthan and Tamil Nadu.

It's not just the tough economic environment that has brought things to this pass. Real estate is a business with close business-politician links and DLF has been in the spotlight for the wrong reasons. In 2005, DLF bought the NTC land in an auction for Rs 702 crore. "At an FSI of 1.33, DLF paid too high a price," says an industry expert who does not want to be identified. "It was difficult for DLF to develop this land and sell it profitably." FSI (floor space index) refers to the buildable area on a plot of land. An FSI of three means that the total floor area of a building can be three times the gross area of the plot on which it is constructed.

About five years later, says the expert, the Maharashtra government controversially raised the FSI to four. Of the roughly 70 builders who submitted their proposals, just six or seven got final approvals. That DLF was one of them, says the expert, speaks volumes of its influence. In the case of Aman Resorts, DLF has been scouting for a buyer for more than two years, but has been unable to get the expected price for the property.

DLF decided to go beyond its core markets of Delhi and the National Capital Region (NCR), and Chennai in the last financial year. Out of 13.55 million square feet (msf) sales bookings last year, some 5 msf were in Lucknow, Hyderabad and New Chandigarh. "The idea was to get a sense of other markets." says Sandipan Pal, analyst at Motilal Oswal Securities. "Besides, most of these were plotted projects, so the turnaround time was faster." As a result, DLF's average realisation price per square foot tanked from Rs 6,500 per square feet to Rs 3,900 per square feet - a drop of 40 per cent.

This year, the company has adopted a back-to-core strategy, focusing heavily on the Delhi-NCR, Bangalore and Chennai markets. DLF is expected to sell around 12 msf this financial year, and a significant part will be in the Gurgaon region, including the highend Magnolias II project.

Pankaj Kapoor, Managing Director at Liases Foras, a research and ratings agency, says the Gurgaon property market is driven by investors. "It is speculative in nature," he says. "More than 80 per cent of buying is from investors. DLF can sell more, but there has to be appetite for it."

On the commercial front, the situation is even grimmer. More than 17 per cent of DLF's revenues come from rental income from commercial and retail spaces, which are over 22 msf. Over the past 15 months, the office leasing business has not performed well. Compared to 4.38 msf in 2010/11, DLF added just 1.7 msf in the past 15 months to its leasing portfolio, largely due to cancellations by corporate clients. DLF's clients include IT and multinational companies.

Maheshwari of Jones Lang LaSalle thinks that despite all odds, DLF still enjoys strong brand equity in the market. "They haven't yet defaulted on a single interest payment which reinforces investors' confidence," he says. "It's only a matter of time before DLF gets back in shape."

With the spotlight on the DLF-Vadra link, the passage of time may just add to challenges that DLF has to face.