Kishore Biyani is smiling again. The poster boy of the retail revolution in India is

starting a new business called Big Bazaar Direct . The e-commerce initiative involves setting up a network of franchisees who will take the Biyani-led Future Group's Big Bazaar retail chain to the doorsteps of consumers. The venture, says the company, will usher in the next retail revolution. While that may be a tad too optimistic, the new business certainly means Biyani has overcome the difficulties he was facing until recently.

What makes Biyani bullish? Until a year-and-a-half ago, Future Group was burdened with massive debt. But the company was not generating enough cash. That not only made repaying the debt difficult but also put a question mark on the company's survival. What did Biyani do? In April last year, he sold his profitable Pantaloon retail business to Aditya Birla Nuvo for Rs 1,600 crore. A month later, he sold his financial services business to private equity player Warburg Pincus for Rs 590 crore. And this year, he sold a 22.5 per cent stake in his life insurance joint venture with Italy's Generali for Rs 300 crore. The

sale of assets helped him prune the debt to Rs 3,500 crore from Rs 10,000 crore two years ago, and put him back on track.

In debt-laden Corporate India there are several instances like the Future Group. While financially stressed companies globally are shedding assets - French retail giant Carrefour and Canadian gold producer Barrick Gold to name two - the trend is most visible in India. Corporate houses such as GMR Group, Anil Ambani's Reliance Group, Videocon Industries, Adani Group, GVK Group and Jaiprakash Associates have either sold some assets and stakes in the companies or are planning to do so in order to ease their debt burden.

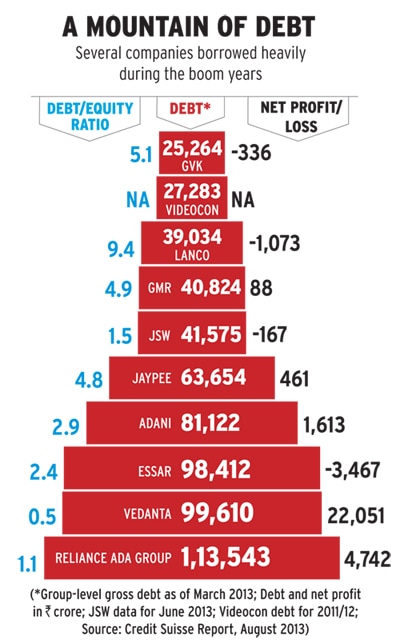

The debt trapA recent Credit Suisse report shows the collective borrowings of 10 large corporate houses rose 15 per cent in 2012/13. Anil Ambani's Reliance Group has a debt of Rs 1,13,543 crore on its books while London-based mining tycoon Anil Agarwal's Vedanta Group owes Rs 99,610 crore (see A Mountain of Debt). What raises alarm bells is the worsening interest coverage ratio at some companies. The ratio indicates a company's ability to pay interest on its loans. Companies with a ratio of more than one are considered to be generating enough operating income to meet their interest obligations. The ratio was 0.7 for GMR, 0.6 for Lanco Infratech, and 0.4 for GVK.

The interest coverage ratio is worsening because, while the debt is growing, interest rates remain high and revenue growth is slipping. The weighted average lending rate of state-run banks was 12.06 per cent in June 2013, compared with 12.65 per cent in March 2012, despite the central bank cutting its main lending rate by 125 basis points. According to ratings firm CRISIL Ltd, revenue growth at 1,500 listed companies was 15 to 18 per cent in 2011/12 but has fallen steadily since then. "Growth has plummeted to 3.8 per cent in the April-to-June quarter of this year," says Prasad Koparkar, Senior Director, CRISIL.

What brought Corporate India down to its knees? An economy going through its worst phase in a decade, tepid consumption and high interest rates all can be blamed for the current mess. A weak government that has delayed critical reforms in a range of sectors including financial services, mining, labour, land acquisition and energy has added to the problems. But, perhaps, the most important reason why many corporate houses that were in the fast lane until a few years ago are now struggling to survive is past exuberance.

Sachindra Nath, Group CEO at Religare Enterprises Ltd, puts things in perspective. Corporate growth was funded purely out of debt, he says. "The hypothesis was that with debt they will grow the business.

The equity valuation subsequently will go up and they will raise further capital," says Nath. This calculation went horribly wrong as the economy slowed and capital markets turned choppy.

Wake-up callAashish Mehra, Partner and Managing Director for Asia Pacific at consultancy Strategic Decisions Group, says irrational exuberance, poor risk assessment and overconfidence among companies that they will be able to manage things if they go wrong led them on the path to self-destruction. "Business houses went overboard with their investments during the boom of 2000-2007, choosing to live beyond their means," he says. "When they realised they might be stuck with a few lemons and they were unable to manage them, that turned out to be a wake-up call and forced them to put up a 'on sale' tag."

In the last few years, corporate growth was funded out of debt. The hypothesis was that with debt they will grow the business and subsequently equity valuation will go up for raising more capital. A subdued stock market, however, changed everything: Shachindra Nath, Group Chief Executive Officer, Religare Enterprises

A prime example of irrational exuberance is Vijay Mallya's Kingfisher Airlines, which began operations in 2005. It took on debt to buy planes and acquire a low-cost airline in 2007. By 2011 it became India's second-largest carrier by market share. But it never made a profit and, by early 2012, wasn't generating enough cash to service loans, make tax payments or pay staff salaries. Soon, employees struck work, the tax department froze its accounts and banks refused to lend more. The airline was ultimately grounded, but not before it weakened its parent UB Group and forced Mallya to sell a controlling stake in flagship United Spirits to Diageo Plc in November 2012.

Naresh Goyal, founder of Jet Airways, has fared no better.

Jet's debt crossed Rs 12,000 crore last year. In April, Jet sold a 24 per cent stake to Gulf carrier Etihad Airways.

The aviation sector, however, is not the worst affected. Companies in infrastructure, real estate and energy sectors lead this race. Hyderabad-based infrastructure conglomerate GVK Group is looking to raise about Rs 2,200 crore by selling a stake in GVK Airport Holdings to trim debt. The cash-strapped group operates Mumbai and Bangalore airports. Finance chief Issac A. George says the company hopes to finalise a deal by December.

GVK's southern rival GMR Group sold a 74 per cent stake in a highway project in September for Rs 222 crore to a fund of infrastructure financier IDFC. This was the second sale of a road project within six months by the Bangalorebased infrastructure group founded by G.M. Rao. The company had in March sold its Singapore power plant. More assets could be put on the block. Madhu Terdal, Group Chief Financial Officer at GMR Group, says the corporate house continues to focus on creating liquidity and reducing debt.

Also in September, Jaiprakash Industries, the Delhi-based builder of roads, dams and townships, sold its Gujarat cement assets to UltraTech Cement. The sale of assets with a cement production capacity of 4.8 million tonnes a year will help Jaiprakash cut its debt by Rs 3,600 crore. But it isn't enough to ease the Rs 56,000 crore debt burden substantially, and the company is also planning to sell some of its hydroelectric power plants and land.

In Gurgaon, DLF, is also striving to cut debt. The country's biggest property developer had diversified into the hospitality sector in 2006 after tying up with global hotel chain Hilton International. In 2007, it bought a controlling stake in Singapore-based hotel chain Amanresorts International for $400 million. But the plans didn't work out. The hotels industry suffered a jolt after the global economic crisis led to a fall in tourist traffic.

Simultaneously, demand for property dropped and raising funds became challenging. DLF's net debt shot up to Rs 22,725 crore in 2011/12 from Rs 10,323 crore in 2007/08. The company embarked on a debt-reduction programme in November 2011 when it bought out Hilton from their joint venture to make the asset sales easier. Last year, DLF sold four land parcels, where it had planned to build hotels with Hilton, to a Kolkata-based consortium for Rs 567 crore. It is also looking for a buyer for Amanresorts. The efforts have helped cut its net debt to Rs 20,369 crore.

Asset sales are happening in the energy sector, too. In June, Videocon Industries sold its 10 per cent stake in a Mozambique gas block to a consortium of Oil & Natural Gas Corporation and Oil India for $2.48 billion (about Rs 17,000 crore). The sale will help the consumer electronics company led by Venugopal Dhoot to slash its debt to Rs 10,000 crore from Rs 27,000 crore. Another energy company buried under a pile of debt is Suzlon. The Pune-based wind turbine maker in September sold a majority stake in its China arm to a local company for about Rs 177 crore to battle its Rs 13,000 crore debt. Lossmaking Lanco Infratech is restructuring its debt and looking to sell some of its power plants.

Some companies fell into the debt trap while growing their overseas businesses. Brothers Malvinder and Shivinder Singh expanded their Fortis Healthcare hospital chain in the past few years through overseas acquisitions by borrowing money. Recently, the company sold its businesses in Vietnam and Australia, which helped prune its debt to Rs 3,284 crore from Rs 7,000 crore. The company's focus is on improving operating performance though it could evaluate more options for divestment if required, says Group CEO Vishal Bali.

There is always an aversion to selling assets. But refinancing options by way of overseas borrowing or domestic debt are also drying up: Prasad Koparkar, Senior Director, CRISIL

Shree Renuka Sugars is another company which expanded its global footprint in recent years. The company ventured into Brazil with the acquisition of two loss-making companies in 2010. The sugar maker is now saddled with Rs 7,590 crore of debt, of which Rs 5,190 crore is on the books of the Brazilian companies. The company's problems mounted after a drought in the South American nation hurt output. The Brazilian real's steep drop against the US dollar has made debt servicing even more difficult. The company is now looking to sell some Brazilian assets including a power plant.

Share pledges, loan refinancingSelling assets, especially those core to a company's business, is rarely the first choice for founders. "There is always an aversion to sell assets," says Koparkar of CRISIL. Financially stressed companies initially try to cut costs, defer expansion plans, sell or pledge shares to raise funds, and refinance loans. When these options fail, companies sell their assets. "There is no one-size-fits-all solution," says Michael J. Surface, Leader-Advisory at consulting firm PricewaterhouseCoopers (PwC) India. "It depends on the company and its liquidity position."

Companies where founders pledged shares have another problem to worry about. Suzlon's founders have pledged almost their entire stake in the company while promoters of Jaypee Infratech have put more than 80 per cent of their holding as collateral with lenders. The pledging turned counter-productive when companies' stock market valuations dropped. For instance, the market value of Shree Renuka, where founders have pledged about 39 per cent of their stake in the company, has fallen to about Rs 1,200 crore from Rs 2,700 crore five years ago. Similar is the case with Videocon. Its founders have pledged twothirds of their stake and its market value has slumped to about Rs 5,600 crore from nearly Rs 10,000 crore in 2007.

Some companies have managed to refinance their loans from local and overseas lenders. In January 2012, Anil Ambani's Reliance Communications refinanced its foreign currency convertible bonds of $1.18 billion from three Chinese lenders. But not everyone is as successful as Ambani in refinancing loans. Suzlon defaulted on its overseas bonds last year, though it also managed to raise fresh debt this year to repay existing loans.

"The refinancing options have dried up," says Koparkar. "A weak rupee has only increased the cost of hedging [overseas loans]."

Cautious banksMany debt-laden companies have delayed interest payments or defaulted on loans. This has pushed banks' bad loans higher. Gross bad loans at Indian banks have jumped to 3.92 per cent of total loans in June 2013 from 2.36 per cent in March 2011. According to the Reserve Bank of India (RBI), stress tests suggest gross bad loans may rise to 4.4 per cent by March 2014 in a severe stress scenario.

Banks have also seen a rapid rise in loan restructuring. The size of restructured assets as a percentage of gross advances of banks has more than doubled to above six per cent as of June 2013 from 2.6 per cent in December 2010. Kuntal Sur, Director for advisory services at consulting firm KPMG, says debt restructuring is not unusual during economic downturns but it needs total commitment from the founders of a company to succeed.

The level of restructured debt has reached alarming levels at some lenders such as Central Bank of India and Indian Overseas Bank. Central Bank of India's restructured portfolio is at Rs 14,000 crore to Rs 15,000 crore, says Executive Director R.K. Goyal. "Our restructured portfolio is a bit higher because of exposure to discoms [power distribution companies]. If you exclude the discoms, the restructured assets are about Rs 6,000-7,000 crore, which is equal to three per cent of our total advances," he says.

Promoters do not have a divine right to stay in charge regardless of how badly they mismanage an enterprise, nor do they have the right to use the banking system to recapitalise their failed ventures: Raghuram Rajan, Governor, Reserve Bank of India

Rising defaults and debt recasts have made banks wary of lending. "Banks are sitting on a lot of liquidity but they are cautious about where they invest and who they invest with," says PwC's Surface. Avinash Gupta, Senior Director at business services firm Deloitte Touche Tohmatsu India, says banks are looking for better quality assets. "You can't keep pushing the can down the road," he says. "Sometimes you will have to stop and keep looking for better assets."

Banks are also putting pressure on overleveraged corporate houses to let go of some assets. And this pressure is unlikely to ease. The new RBI governor has made his stand clear. Banks must improve the efficiency of the loan recovery system, Raghuram Rajan said on September 4, the day he assumed office. "Promoters do not have a divine right to stay in charge regardless of how badly they mismanage an enterprise, nor do they have the right to use the banking system to recapitalise their failed ventures," he added.

So, what is in store for debt-laden companies? "Those who lack management capability and financial strength may have to get out of the business and completely rethink the portfolio," says Suresh Subudhi, Partner and Director at Boston Consulting Group. Companies with strong management will need to churn their business portfolio, he says.

They must retain cash-generating assets and sell cash-sinking assets to improve revenue growth and enhance profitability, he adds. Mehra of Strategic Decisions Group agrees. While divesting assets, the key question companies face is whether they should sell the lemons or the crown jewels. "It would be a pity to be left only with a lemon portfolio by divesting the crown jewels," he says. "Perhaps the answer is in the right combination." There are some who are optimistic about the future. "Liquidity is improving and the government has cleared many stalled projects," says Goyal of Central Bank of India. The asset sales will release the funds as well as management bandwidth for corporate houses to focus on their main businesses. Nath of Religare says corporate houses are no longer overenthusiastic and are thinking through their business plans. Retail pioneer Biyani has shown how to make tough decisions and come back. It's time for others to take a cue.

With inputs from Niti Kiran, Ajita Shashidhar, Manisha Singhal, Ajay Modi, Suprotip Ghosh, E. Kumar Sharma, Anilesh S. Mahajan, and Manu Kaushik