Mumbai-based brothers, Dhruv and Piyush Khaitan, founded a digital payments venture in the 1990s. To leverage the experience in payments business, they established NeoGrowth in FY13 to lend to small businesses. They understood the problems that retailers faced in raising growth capital, and created an underwriting method based on card swipe data along with flexible repayment options.

"We decided to lend to consumer-facing small businesses and leveraged their PoS (point of sale) swipe data for credit assessment. We knew digital payments would continue to grow at a rapid pace over the next few years. We resolved to participate in that growth," says Khaitan, Founder and MD, NeoGrowth.

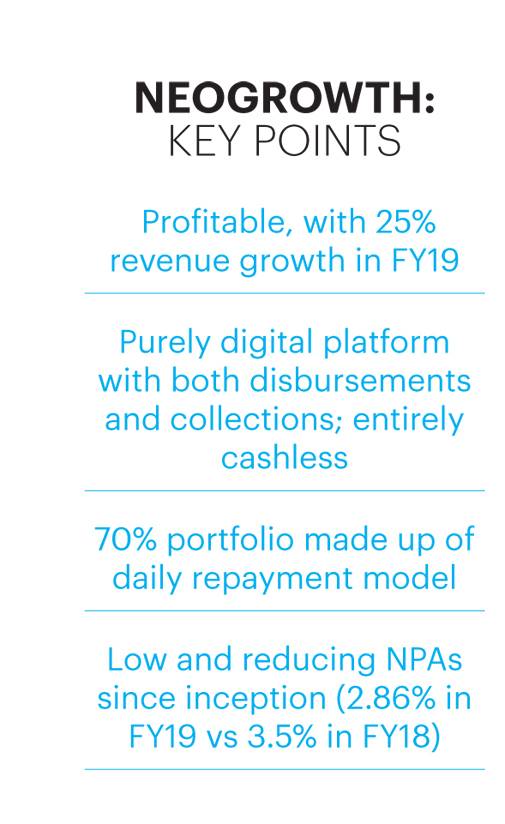

The fintech firm recorded profits of Rs 4 crore on revenues of Rs300 crore in FY19. Even during the NBFC crisis that shook the backbone of the financial system, NeoGrowth managed to stay afloat. It crossed Rs 1,000 crore as asset under management (AUM) in FY19 and has grown 60 per cent since then. With an average loan ticket size of Rs 12 lakh, the company has disbursed over Rs 5,500 crore since inception. Its loan amount ranges from a minimum of Rs 1 lakh to a maximum of Rs 70 lakh at interest rates of 20-24 per cent.

It has raised Rs 500 crore till date from investors including Omidyar Network, Aspada Investment Company, Khosla Impact, Accion Frontier Inclusion Fund managed by Quona Capital, IIFL Seed Ventures Fund and Leapfrog Investments. It has also raised funding from a mix of overseas and domestic lenders and borrowings from banks. "Till now, we have raised close to Rs 1,600 crore of debt capital. Some of our debt investors are Blue Orchard, FMO (Dutch Sovereign Entity), Symbiotics, responsAbility, SIDBI and RBL," says Khaitan.

Creditworthy

The journey started when the brothers founded Venture Infotek in the 1990s to provide technology to process transactions for retailers who accept credit cards. "We were in close touch with owners of shops and restaurants. One thing that struck us was how difficult it was for them to raise finances. Banks asked for large collateral, which they did not have," says Khaitan. He saw an opportunity in this and decided to bridge the credit gap for borrowers who were creditworthy but were denied funds as traditional underwriting methods didn't find them creditworthy. They divested Venture Infotek in 2010 and NeoGrowth was set up to start lending to retailers, restaurants, apparel shops, kirana stores, petrol pumps, groceries, pharmacies and MSMEs.

Banks typically do balance sheet assessment of the borrowers. Khaitan knew that to make a difference, he had to figure out newer ways of credit assessment. "We had to move away from balance sheet assessment; we started studying the nuances of cash flow-based lending. We developed algorithms to analyse bank statements of merchants, and their daily debit and credit card transactions to get a sense of their sales," says Khaitan. The firm's process is closely linked with the card swipe machine. While it is the banks that instal the PoS machines, the fintech firm collects card data from merchants to analyse and extend loans.

To judge credit worthiness, NeoGrowth collects 10 major and 30-40 minor data points to create a scorecard. "It took us a year-and-a-half to create the required tech that helps figure out whom to lend to and how much." Their repayment model involves daily, fortnightly, or monthly options. According to the company data, 70 per cent of the loan portfolio is on a daily repayment mode. "When we started NeoGrowth we spent a lot of time understanding the needs of borrowers. We realised it is difficult for small businesses to make monthly payments. For instance, if they have borrowed Rs 6-7 lakh, repaying Rs 2,000 daily is a better proposition than Rs 50,000 a month," he explains.

This simplified the repayments procedure too. Borrowers don't have to remember and initiate account transfers. "We have built a digital model in which money comes automatically from the bank account of the merchant to us daily. The acquirer bank that has deployed the PoS has to settle transactions with merchants every day. So, the bank directly sends the required amount to NeoGrowth every day," he says.

What happens if there is a default? "We have a calibrated process. We call and understand the reason for non-payment. For instance, one borrower had been regular with repayments but couldn't do it for a few months because the road leading to his store got blocked due to a flyover construction. We understood his challenge. For such genuine borrowers, we have the option of loan deferment and rescheduling," says Khaitan. For wilful defaulters, NeoGrowth has a collection team. In some cases, they have gone for litigation and filed suits. "These are time-consuming processes but in certain cases we have to do it." NeoGrowth's default rate is less than 3 per cent.

Reaching Milestones

NeoGrowth has taken its business forward at a fast pace. Its loan book as on January 31, 2020 stood at Rs 1,307.5 crore. With 13,000-plus customers and 1,000-plus employees, it is now present in 21 cities and claims to have an over 60 per cent renewal rate. On technology, it has invested heavily in analytics and machine learning, which has helped it reduce the turnaround time for loan sanctions. "It used to take seven days to sanction a loan. Now we sanction loans up to Rs8 lakh in minutes and more than that in 48 hours. The self-learning scorecard system that gets updated daily helps us take more informed decisions and quicker."

The company has also collaborated with a number of platforms for customer origination, information, analytics, collections and risk management. It has over 500 channel partners. NeoGrowth has received ISO 9001:2015 certification, among the first few players in the MSME lending space to do so. The company takes pride in the fact that 80 per cent of its loans go to first generation entrepreneurs. Besides, 12 per cent of total disbursements in FY19 were towards businesses run by women either as sole proprietors, partners or directors.

What Next?

NeoGrowth lends to 27 types of consumer-facing businesses. At least two-three businesses have been showing signs of stress. "Automobile service stations and auto ancillaries supplying to the automobile industry are feeling the effects of the slowdown. Similarly, mobile dealers are under pressure as imports from China have come down due to Coronavirus," says Khaitan.

Besides, the fintech lender is dealing with perception issues due to the NBFC crisis. "There is a misconception in the market that all NBFCs are under trouble. Only a handful of NBFCs and housing finance companies have balance sheet issues. So, even good NBFCs like us are facing the perception challenge even though we maintain robust governance standards. We publish our financial results on the website so that everyone can see it," says Khaitan.

Warts and all, contrary to the industry trend, NeoGrowth did not record a slowdown due to liquidity crunch post the NBFC crisis. They, in fact, ramped up disbursals. "We grew our business 50 per cent year-on-year and developed a loan book of `1,400 crore from `650 crore during that period." The focus is on building scalable processes that allows them to maintain 50 per cent growth year-on-year. "Digital payments and MSME financing is growing much faster than we imagined. We need to scale up while we build a robust risk management system along with retaining the right talent," says Khaitan.

Their strategy is to go "Deeper, Wider & Newer" - go deeper into existing markets, widen base across more cities and launch new products. The company wants to build a loan book of $1 billion over the next three years. Will it diversify its business beyond consumer-facing clients? Unlikely, says Khaitan. They intend to continue in the niche that they are in. "We have pioneered digital lending for MSMEs. The credit demand coming from MSME retailers is massive. We need 20 NeoGrowths to meet it."