Rs 545 crore: the blob of debt the Mumbai-headquartered Wockhardt Ltd has to wipe out. Six months: The time it has to do that. Circa 2004: The year the pharma major’s current woes can be traced back to. Of course, the scenario didn’t look so gloomy then. When the company raised $110 million from the global markets five years ago by floating foreign currency convertible bonds (FCCBs), the management perhaps never thought it would have to repay it one day. Any FCCB issuer would hope its bonds would get converted into equity. But with its stock price today (as on May 6) quoting at just 18 per cent of the conversion price fixed then, the bond holders will be in no hurry to rush to Dalal Street. The nervous drug-maker, hit by Rs 139 crore losses for the year-ended December 2008, is desperately seeking out ways to rid itself of the FCCB albatross before it comes up for redemption in October this year.

A Wockhardt spokesperson says a clear picture on how the company would deal with the FCCB payout will emerge once the corporate debt restructuring (CDR) taken up by a clutch of banks is through. Wockhardt isn’t the only Indian company that’s been laid low by the FCCB time-bomb. A host of Indian companies, which range from pedigreed large-caps like Tata Motors, Videocon Industries and Suzlon Energy, to their lesser-known counterparts like Aksh Optifibre, Subex Ltd and Marksans Pharma, are staring down the FCCB barrel.

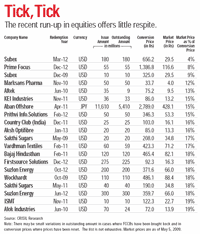

With the current market price of almost all these companies nowhere near their conversion price—CRISIL has come up with a list of around 45 companies where the market price as a percentage of the conversion price is lower than or at 20 per cent as of end-March—a number of these promoters are in a spot.

FCCBs are essentially foreign currency-denominated debt with a maturity period of three-to-five years. The investor has the option of converting the bond into equity. He would typically convert it into equity and sell it for a premium if the stock is trading above the conversion price, which is the price at which the bond is to be redeemed. In the eventuality of non-conversion, the bond has a coupon rate and a redemption premium. If the scrip is trading below conversion price, the investor would hold the bonds as a debt paper and go for redemption on maturity. Either way, the investment is protected. These bonds are freely traded in overseas markets and whether they are selling at a premium or discount depends on how the company’s scrip is doing on the Indian stock markets. The attraction of FCCBs is in the option of converting them into equity. Few are interested in debt in view of low returns. The company issuing such bonds, too, prefers conversion to redemption.Why issuers love FCCBS

Why investors love FCCBS

|

As these FCCBs were at very low coupon rates, replacing them with bank debt means an increase in annual interest cost for companies, which in turn will impact profits. The redemption premium will hit their net worth, too.

The RBI's buyback lifeline...

And the options before India Inc...

|

Many bonds, issued during the boom period of 2003 to 2007, are trading at discounts as high as 50 to 60 per cent. By buying them at a discount, Indian companies can earn twin benefits of making a gain by paying off a foreign loan at a discount and not having to carry the mark-to-market losses for the redeemed FCCBs. In addition, they also save on redemption premium payable on maturity.

& CFO, Hotel Leela Venture")

Way to go

In the prevailing hostile climate, do Indian companies have a strategy to surviving the FCCB juggernaut with minimal damage? A section of chief financial officers is betting on a stock market comeback. Some companies like Reliance Communications, Hotel Leela Venture, Jubilant Organosys, to name just three, have bought back a part of their FCCBs at huge discounts and lightened their balance sheets.

Hotel Leela Venture, for instance, has bought back onefourth of its euro outstanding due for expiry in September 2010 and one third of its dollar bonds set for expiry in 2012. “Both euro and dollar put together, we have bought back bonds worth $50 million (Rs 250 crore). We will see how things shape up and decide on further buybacks of our euro issue. As for our dollar issue, we still have a lot of time and will decide according to the situation,” says V.L. Ganesh, Director, Finance, & CFO, Hotel Leela Venture.

Price resetting is an option, and according to CRISIL’s Sridhar, “Only those companies that cannot raise debt from the market may opt for resetting of prices.’’ If the payouts develop into a crisis, there could be other options. Bhatt of Elara Capital thinks some companies may issue new bonds in exchange of old ones on new terms.

“Investors may find this far more acceptable than fighting court cases in India. This is a new territory for everyone. Eventually these bonds will get restructured as no one wants court cases.” In fact, Suzlon Energy’s latest attempts to issue fresh bonds on new terms for its $200 million tranche issued in October 2007 were overturned by bondholders.

When the BSE Sensex soared by 731 points—a seven-month high— on May 4 to polevault into 12,000 territory, many promoters in the line of the FCCB fire may have sensed a turnaround. But it will take many more such bouts of no-holds-barred bullishness—for which few fundamental triggers exist—to transform their despair into hopefulness.