For the banking sector, just looking to come out of the NPA crisis - gross NPAs fell after seven years, from 11.2 per cent in 2017/18 to 9.1 per cent in 2018/19 - the good news may be short-lived. More stress is emerging in agriculture, Mudra small loans, unsecured retail loans and telecom where banks and non-banks have as much as Rs 27-31 lakh crore locked up (See New Stress Points). The total balance sheet of banks and non-banks is Rs 190 lakh crore, equal to India's GDP, and any blow-up in these segments could threaten the stability of the financial system as well as the already vulnerable economy.

"TBS-II (the second wave of the twin balance sheet) crisis is the reason for the current economic troubles," Arvind Subramanian, former chief economic advisor, has argued in a 38-page paper titled "India's Great Slowdown: What happened? What's the way out?" India, according to Subramanian, is facing a four balance sheet challenge. Non-banks and real estate firms have joined the earlier two villains, banks and infrastructure companies, under TBS-I. "TBS-II will lead to an even bigger damage to the economy," warned Subramanian, who has co-authored this paper with Josh Felman, former India head of the International Monetary Fund.

Economic growth is slowing. Worse, policymakers are still to figure out if the problem is structural or cyclical. Any delay or confused response will compound the problems. A case in point is the recent Rs 1.45 lakh crore corporate tax cut, which addresses supply-side issues but leaves demand-side problems unaddressed. To top it up, there is no room for either monetary easing (inflation is rising, rate transmission is in a mess and government interest rates are sticky) or fiscal stimulus (government revenues are well short of the target, mainly due to the slowdown). According to Uday Kotak, MD & CEO of Kotak Mahindra Bank: "Savers in India are not used to lower interest rates because of higher small savings rates. How will they accept the dramatic lower bank deposit rates?"

Net-net, banks have little to look forward to in 2020 in terms of asset quality. Subramanian, in his paper, has highlighted another dangerous sign - the interest on corporate debt is accumulating much faster than the revenue the companies are generating. "The corporate cost of borrowing now exceeds the GDP growth rate by more than four percentage points," he said. Clearly, this stress will, finally, show up on bank balance sheets, and especially vulnerable will be small enterprises which have taken Mudra loans, agriculture sector (rural distress, farm loan waivers), the struggling telecom sector and, in case of big job losses, unsecured borrowers, too. The RBI's latest financial stability report warned that gross banking NPAs could spike to 10 per cent in the next nine months from the present levels of 9.3 per cent if the situation deteriorates further.

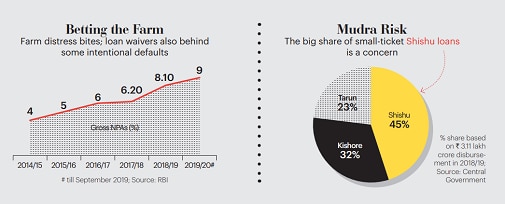

Mudra Loans - Chickens Come Home to Roost

Pune in Maharashtra is bearing the brunt of cautious financiers. Many banks and non-banks have either stopped or reduced lending to small and micro entrepreneurs in this automobile hub. "Factory shifts are down to three a week. Ancillary units are sacking temporary workers. The entire ecosystem of suppliers and dealers has been hit," says a banker. The situation is the same in other industrial hubs. The worst-hit are entrepreneurs who have taken collateral-free Mudra loans of up to Rs 10 lakh.

For SBI, gross NPAs in the Mudra category touched 18.5 per cent in September 2019. For Punjab National Bank, the figure was 22.71 per cent, while for Union Bank of India, it was 18.50 per cent. "While such a massive push (under Mudra) would have lifted many out of poverty, there have been concerns about the growing level of NPAs among these borrowers," RBI Deputy Governor M.K. Jain said at a microfinance conference in Mumbai in last November. The deputy governor told bankers that they need to focus on repayment capacity at the appraisal stage and closely monitor these loans through their life cycle.

Interestingly, official data tells a different story. The government has put gross Mudra NPAs at 2.86 per cent of the amount disbursed in 2018/19. Is it hiding the true extent of Mudra NPAs? Partially, say experts, adding that the correct denominator should be loans outstanding as old loans get repaid and new ones are added. Secondly, the deputy governor is probably more concerned about public sector banks (PSBs) than private sector banks, NBFCs and small finance banks as the private players are giving Mudra loans profitably. Thirdly, the average hides the fact that the PSBs have higher NPAs. Lastly, the higher lending target year after year increases loans outstanding, the denominator, which gives a lower NPA figure. The target for Mudra loans was Rs 1.80 lakh crore in 2016/17, Rs 2.44 lakh crore in 2017/18 and Rs 3 lakh crore in 2018/19. A similar issue had distorted the picture between 2004/05 and 2010/12, when huge year-on-year rise in corporate lending led to banks showing low NPA ratios. The real position came out when lending slowed drastically.

The weak link in the chain is the flawed PSB model of tapping individual banking correspondent agents (bank Mitras) for sourcing the Mudra business. Private sector banks use their corporate banking correspondent model. Another weakness of PSBs is their inability to evaluate a project and underwrite based on risk, a point highlighted by the RBI's Jain in his microfinance speech.

To escape the coming crisis, PSBs need to learn from private sector banks and microfinance players, which are successfully lending to micro entrepreneurs based on customer segmentation. "They follow a joint liability group (JLG) of mostly women entrepreneurs, a Mohammed Yunus Model," says Sudip Bandyopadhyay, who runs a fast-growing microfinance business - Intitrade Capital - with operations in eight states. Many private sector banks start with loan exposure of Rs 10,000 or Rs 15,000 and slowly build a database of creditworthy customers. "Micro lending will always be susceptible to economic cycles whereas the JLG model provides a cushion because of the nature of the business and social pressures to pay up," says a private sector banker.

One can say in defence of PSBs that they have legacy issues and have to focus on liabilities (opening bank accounts) as part of the government's financial inclusion drive. "Micro lending is not their cup of tea," says a micro lender. At present, a large part of Mudra loans are less than Rs 50,000. Most PSB Shishu loans go to first-time entrepreneurs or those with limited track record of business. "This is a relatively risky space," says a private sector banker. Also, in branch banking, PSB staffers tend to lend to those who have deposits in the branch. There is also a geographical bias. For example, Rajasthan is emerging as an upcoming centre for many NBFCs and private sector banks for financial services business. "The local political community also puts pressure on banks. We try to withstand these pressures but PSBs have nowhere to go," says the private sector banker.

A research by Bank of America says though Mudra loan NPAs do not appear to be a meaningful threat at current levels, a severe deterioration in asset quality could have a significant impact on banks if macro risks go up. And the macros, as we know, have been turning for the worse. GDP growth has fallen for eight straight quarters now.

Unsecured Retail Loans - A Ticking Bomb

A year before the government went into the Mudra loan overdrive, banks, facing the prospect of big corporate loans turning bad, started building retail assets as the segment had low NPAs historically. Between 2013/14 and 2018/19, retail loans of banks and non-banks doubled to Rs 48 lakh crore. But what is worrisome is the rising share of unsecured retail loans in bank credit which jumped from 24 per cent in 2014/15 to 33 per cent in 2018/19 (Rs 7 lakh crore out of Rs 22.20 lakh crore retail loans). While unsecured loan data for global banks is not available, the higher share of household debt to GDP in the US, the UK and China shows rising unsecured retail loans. The household debt in India is 11-12 per cent of GDP. This is 87 per cent in the UK, 75 per cent in the US and 54 per cent in China.

"There is easy availability of credit from non-banks and fintechs. There is also a mindset change among people towards credit," says Harshala Chandorkar, Chief Operating Officer, TransUnion CIBIL. Anup Bagchi, Executive Director (Retail), ICICI Bank, says the segment per se is not bad. "Banks have large databases. We look at transaction data extensively apart from the credit bureau score," he says. Banks say they mostly tap existing customers with a good repayment record. At the largest private sector bank, HDFC Bank, unsecured personal loan and credit card book is 27 per cent of retail assets. Similarly, the portfolio of small finance banks is mostly unsecured. NBFCs and fintechs, too, are taking big positions in unsecured loans.

Among these players, non-banks are taking a bigger risk by giving small loans, tapping new customers and lending to even gig workers and those with low credit rating. "For the first time, NBFCs are facing challenges on both sides of the balance sheet. There has been shrinkage across sectors on the assets side even as the liabilities (funds) market has dried up after the IL&FS debacle," says a market expert. If the growth cycle stops, there could be a situation of low credit growth, falling incomes and rising delinquencies. The RBI's recent report on "Trends in Banking" has warned that the slowdown in consumption is expected to restrict growth of retail assets "even as the possibility of defaults in the retail segment rises as growth slows down". At a macro level, there is also an issue of growing household debt. In the last six-seven years, there has been a rise in financial liabilities of households as percentage of GDP from 3.3 per cent to 4.3 per cent. Net financial savings fell from 7.2 per cent to 6.6 per cent of GDP during the period.

However, Chandorkar of TransUnion CIBIL doesn't see huge delinquencies in unsecured loans. "The higher growth or denominator certainly has a part to play at the moment (in showing lower NPAs), but we don't see any sign of alarm," says Chandorkar. Similarly, Ramesh Iyer, Vice Chairman and MD, Mahindra Finance, whose company operates in rural areas, says customers are willing to discharge their liabilities by paying on time but they are not ready for acquisition of assets at the moment.

For banks and non-banks, the unsecured loan segment has been a saviour in the absence of huge demand from companies as well as secured retail segments such as auto and real estate. A recent ICICI Bank report on retail assets powered by ratings agency CRISIL says retail loans of banks and non-banks are estimated to double from Rs 48 lakh crore to Rs 96 lakh crore in the next six years. Interestingly, just the three unsecured segments - personal loans, credit cards and consumer durables - are expected to show a compounded annual growth rate of 20 per cent-plus in the next six years. This will substantially increase the share of unsecured loans in retail assets. And if the economy goes further down, mass retail defaults may become a reality. "Flat growth in income will not trigger massive defaults. What can trigger defaults is sources of income getting choked," says Shyam Srinivasan, MD & CEO, Federal Bank. ICICI's Bagchi agrees. "There can be some impact if there is a prolonged slowdown," he says. Retail NPAs for banks were around 1.8 per cent in 2018/19. The figure is low because of high share of secured housing loans. This might change as unsecured loans emerge as a new growth engine for banks.

Agri - Loan Waivers Spoiling Credit Culture

"If there is a fantastic crop, it is a sign of disaster for us lenders. The farmer doesn't get the right price and there is wastage because of inadequate post-harvest infrastructure."

That used to be the common grievance of bankers for a long time. But now a bigger worry is farm loan waivers. "It is becoming a pattern in state elections. The farmers are happily defaulting on expectation of relief from governments," says a banker. A couple of weeks ago, the newly-elected Maharashtra government joined the loan waiver bandwagon. In the just concluded Jharkhand elections, the Congress had promised a waiver of farm loans up to Rs 2 lakh. An RBI report has revealed rise in NPAs in close to a dozen states that have promised farm loan waivers in the last three years. "The waiver could be indicative of the presence of moral hazard with borrowers defaulting in anticipation of a waiver," states the RBI report. The report adds that this behaviour adversely affects credit history of borrowers and their prospects of getting fresh loans.

Right now, at stake is Rs 13-14 lakh crore agriculture loans. Gross sector NPAs shot up from 4 per cent five years ago to 9 per cent in the first half of 2019/20. For PSBs, the situation is worse. SBI's farm sector NPAs rose from 5 per cent three years ago to 14 per cent in the first half of 2019/20. Bank of India ended the first half of the year with a figure of 17 per cent. IDBI Bank's farm sector NPAs have touched 15 per cent. Rural distress and lack of post-shipment infrastructure are adding to the crisis. PSBs are worse off as they are given targets for lending to the agriculture sector. The government recently increased the collateral-free farm loan limit from Rs 1 lakh to Rs 1.60 lakh in what cannot be good news for banks.

The banks' agriculture portfolio, which historically has had high NPAs, also suffers from structural issues. The RBI report pointed out diversion of farm credit for other purposes. It mentioned that states such as Kerala, Tamil Nadu, Telangana and Karnataka got more agricultural credit higher than their farm sector GDP.

Similarly, bulk of agri loans are for the pre-harvest period. Post-harvest is one area where the government is yet to provide enough incentives. "There is a huge anomaly in the market with credit largely going for pre-harvest activities," says Sudip Bandyopadhyay. The RBI report suggests direct benefit transfer. Another solution is giving loans with gold as collateral.

Telecom Sector - Bankruptcy Looms Large

The bankers are staring at huge haircuts in Aircel and RCom. Two years ago, Aircel, with dues of Rs 45,000 crore, had filed for voluntary liquidation. Similarly, RCom was dragged to bankruptcy by operational creditor Ericsson in May this year. The telecom arm of the Anil Ambani group owes close to Rs 50,000 crore to financial creditors. The banks have already made a provision of 40 per cent for these two accounts. They will have to write off a substantial amount in 2020 in a 60-70 per cent haircut scenario.

As if this was not enough, the new AGR liability of Rs 92,641 crore has come as a death knell for the other telecom players, especially Vodafone-Idea and Bharti Airtel, both of which are anyways spending huge amounts to counter the Reliance Jio juggernaut. "If a default happens in the current lot of telecom players, we won't recover anything," says the CEO of a large public sector bank.

He has a point. The presence of RJio is forcing Vodafone-Idea and Bharti Airtel to keep investing in upgrade of towers and spectrum in spite of cash flow pressures. Vodafone Idea booked a loss of Rs 54,765 crore in the first half of 2019/20 due to provisioning for AGR dues. Bharti Airtel reported a loss of Rs 25,816 crore due to the same reason. The stock of Vodafone-Idea has tanked, which closes the option of raising money by selling equity shares. "We will shut shop if we don't get relief...because I think there is no company in the world that can pay that kind of fine in a few months. Just doesn't work like that," Aditya Birla Group Chairman Kumar Mangalam Birla had said after the AGR ruling. Vodafone-Idea's AGR liability is Rs 28,300 crore while Bharti Airtel has to cough up Rs 21,700 crore.

Probably aware of the implications of a big default, the government has provided some relief to the telecom sector by offering a two-year moratorium on spectrum fee, which is about Rs 42,000 crore. In addition, the telecom players have agreed to increase tariffs. The government is even talking of setting a floor tariff to prevent predatory pricing. As per the RBI, banks have a fund-based exposure of over Rs 1.30 lakh crore to the sector. The bankers, however, argue that their major concern is bank guarantee which they have given on behalf of the operators to the DoT for payment of licence fees. "I hope my bank guarantee doesn't crystallise," says a banker. The auction of 5G spectrum will put further pressure on the companies due to prohibitive pricing.

The danger signs have been visible for long. The number of telecom players is already down to four from over a dozen a decade ago. Tata Teleservices, Aircel, Videocon, RCom are all gone. In case of a bankruptcy, the bankers' worry is the eventual liquidation considering they don't have any collateral except spectrum. As per the RBI guidelines, they have to make 100 per cent provisioning in case of liquidation. The only positive here is the NCLT ruling that the banks can sell spectrum in the Aircel case. The DoT, however, has challenged this in the appellate tribunal.

One can only hope that the economy recovers sooner than expected and these risks don't materlialise.

@anandadhikari