Less than three days after a deadly clash between Indian and Chinese forces at Galwan Valley in the East Ladakh region led to the death of 20 Indian soldiers on June 15 last year, a video of a group of men in Coimbatore shouting anti-China slogans and smashing their smartphones went viral on social media. The same day, another group, this time in Surat, was seen doing the same to a TV set.

The Galwan clash was the deadliest between the two Asian giants in over 45 years and further strained the already fragile relations. Besides the military standoff, China’s role in the spread of the coronavirus pandemic and the economic distress that it has brought with it globally resulted in a significant backlash among the business community and consumers across India. Calls for a boycott of Chinese products, not entirely new in India, became shriller.

“Our target is that by December 2021, we should reduce imports from China by up to Rs 1,00,000 crore ($13.3 billion),” said Praveen Khandelwal, National Secretary General, Confederation of All India Traders (CAIT), one of India’s largest trader bodies. “The Indian consumer does not want to buy Chinese goods any more. He is concerned with the spread of the virus and its impact on the Indian economy and the transgressions by the Chinese army on our border. We support them in this cause and will encourage them to buy local products.”

With more than 40,000 trader bodies, representing over 70 million retailers and wholesalers, as members, CAIT came up with a list of 3,000 items that are currently imported from China, but can be easily substituted by “Made in India” alternatives. From toys and T-shirts to handicrafts, coffee mugs, watches and spectacles, Chinese goods are omnipresent in Indian markets, a lot of them classified as unorganised merchandise. So much so that it had even Finance Minister Nirmala Sitharaman wondering aloud why even Lord Ganesha idols have to be imported from China.

“There is nothing wrong in imports that would spur production and create job opportunities and it can be done definitely,” she said while launching the big-bang Atmanirbhar Bharat Abhiyaan initiative last year. “But today, why even Ganesha idols are imported from China…why such a situation...can’t we make a Ganesha idol from clay, is it the situation?” In order to complement this swirl in nationalistic consumerism, the government announced tariff measures for goods from China while putting investments from across the border under the scanner.

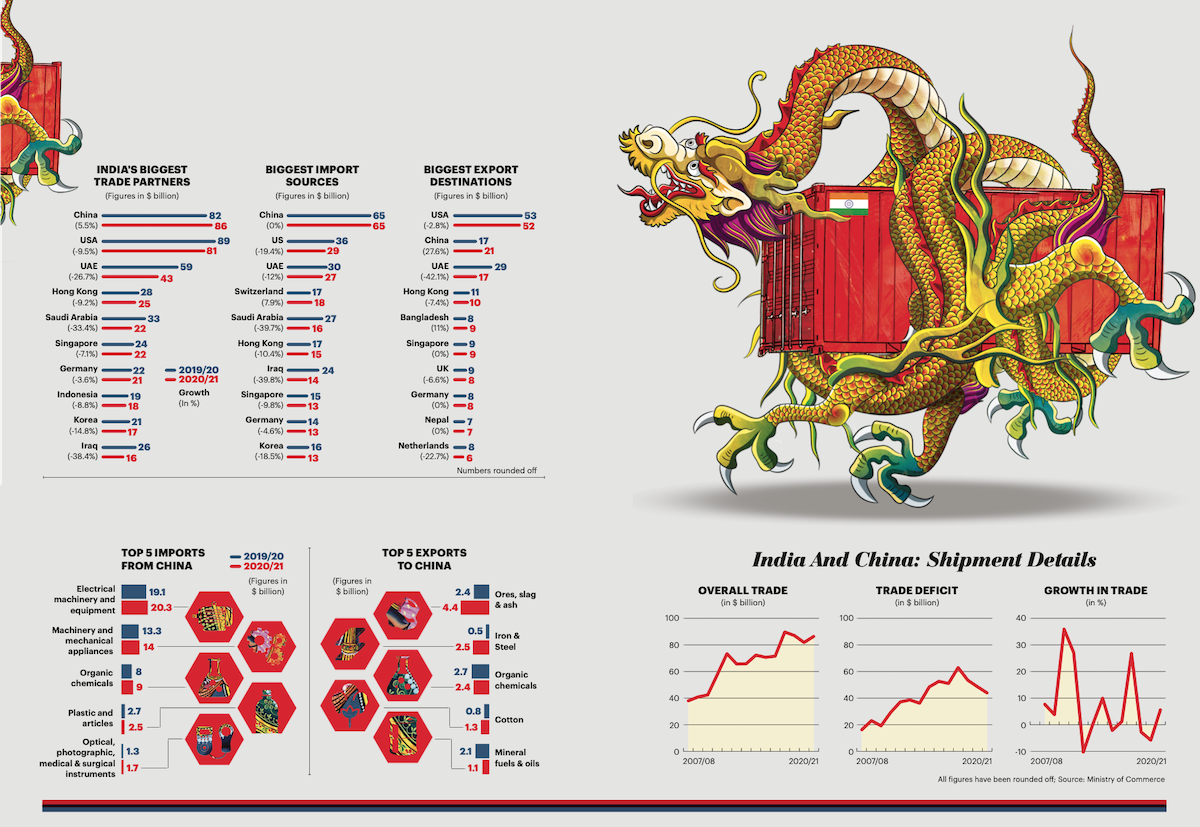

However, it is clear that this anti-China sentiment has not sustained. In FY21, when India’s trade with the world declined due to the pandemic, its dependence on China did not diminish. In fact, with bilateral trade of $86.4 billion, mainland China overtook the US to emerge as India’s largest trading partner. With 5.53 per cent growth, it was the only major country to record a rise in trade with India. Indo-US bilateral trade contracted 9.5 per cent to $80.5 billion. India’s overall trade declined more than 13 per cent to $684.77 billion. Ironically, India’s bilateral trade with China had contracted in each of the two previous fiscals.

Reducing dependence on China is an aspiration not just for India but much of the world. But FY21 shows just how difficult it could be.

The Gulf Of Trade Deficit

The most debilitating aspect of India’s trade ties with China is the huge trade deficit. This is in stark contrast to the healthy surplus with the US. China is by far India’s biggest source of imports at over $65 billion, and for all the anti-China hullabaloo, the decline has been a mere 0.07 per cent. At the same time, India’s imports from the US went down 19.4 per cent to $28.88 billion, while overall imports decreased by more than 17 per cent to $393.6 billion.

“Trade is undertaken by any two countries on the basis of comparative advantage and it is here that China has become a major trading partner. Self-reliance should not mean producing goods at a distorted cost and, hence, imports are essential. Within our trade partners, we need to choose countries which give the best price and quality,” says Madan Sabnavis, Chief Economist, CARE Ratings. “These are private actions. Importers are discerning and have their nose to the ground while choosing partners. The dominance of China is due to the kind of goods which they export to India. Machinery and electronics, where they have an advantage, dominate.”

“China is deeply embedded in the Indian production process with the country’s share in imports of parts and components (P&C) such as blades, engines, electronic instruments, etc, rising from about 5 per cent in 2001 to more than 30 per cent in 2021,” says Nilaya Varma, Co-founder and CEO, Primus Partners. “Reducing dependence on China would be a very long process that would include building partnerships with other like-minded countries, developing domestic industry and products to become self-reliant in critical areas and building export capabilities for Indian products.”

It’s not just that trade is skewed in favour of China. The composition of products India imports from there also benefits China. Machines and electronics account for more than half the import basket in value terms. These are also the two categories that have been targeted by policy actions in the last few years.

In Budget 2019, duties on a range of consumer durables such as air-conditioners, CD, DVD, CRT monitors and TV and plasma display panels were raised. Similarly, in 2020, duties on electrical appliances, including fans, water heaters, ovens, electric vehicles and compressors for refrigerators and air-conditioners were hiked.

After the Galwan clash, restrictions on China, be it on imports or investments, increased further. In April 2020, the commerce ministry’s Department for Promotion of Industry and Internal Trade (DPIIT) amended FDI guidelines to curb investments from China. Aimed at preventing an opportunistic takeover from across the border, any fresh FDI investment from China now requires a specific nod from the government. It puts a spanner in the wheel of companies like Chinese SUV maker Great Wall Motor, whose plans for a foray into India included the purchase of US auto giant General Motors’ Talegaon factory in Maharashtra.

Similarly, the Indian government banned 59 Chinese apps, including the very popular TikTok, in June last year, on grounds of data security. In September and November, another 118 and 43 apps, respectively, were added to the list.

Not surprisingly, electronics and machinery once again received special attention. In end-July last year, the government shifted colour televisions from the free- to the restricted category. This had been done for imported tyres just before the military skirmish in June. In the next few months, the list was expanded to include incense sticks and air-conditioners.

Yet, import of electronics and machines from China grew nearly 6 per cent in FY21. China accounts for over 40 per cent of all electronics and machines that India imports.

“Temporary measures taken post Galwan have helped to an extent. Our imports have come down slightly between 2019/20 and 2020/21, but exports have increased significantly during the period. But since the base for exports is small, the impact on the deficit has not been significant,” says Gopal Krishna Agarwal, National Spokesperson for the BJP. “Though these steps have brought awareness about the impending problems among policymakers and the public, much more needs to be done at the policy level.”

There is a silver lining, though. While the trade deficit is still substantial, it is significantly less than what it used to be — from a high of $63 billion in FY18, it has come down to $44 billion in FY21, the lowest in seven years. “It shows that we are on the right track and policy measures are working. From a time when there was always an increase in the deficit, we have come to a juncture when it is falling rapidly,” says Ashwani Mahajan, Co-convener of the Swadeshi Jagran Manch, an arm of the RSS, one of the staunchest advocates of economic self-reliance. “Our dependence on Chinese goods was so much that the domestic industry was suffering. Efforts to reverse the trend started from 2018 onwards. That was the first time when a finance minister raised tariffs even though protectionism was considered a bad word. Those measures have yielded results.”

The trade deficit has come down more due to increased exports from India than any reduction in imports. India’s exports to China increased over 27 per cent to $21.2 billion, a sharp contrast from its overall export performance, which declined 7 per cent. The increase is almost entirely accounted for by iron and steel, minerals, ore and cotton.

“I am not very happy with higher exports as we are shipping more raw materials — iron ore and minerals to China,” says Mahajan.

End Of The Consumer Backlash

Did the theatrics of smashing smartphones and television sets reflect on actual sales? It did, but only for a short period. Over the last five years, Chinese smartphone makers such as Xiaomi, Vivo, Oppo, Realme, Poco and One Plus have cornered a giant share of India’s burgeoning smartphone market, which had annual sales of over 150 million units in 2020 (the second-largest globally). They have also replicated this success in the nascent smart TV segment. In the first quarter of calendar year 2020, Chinese-origin smartphone makers commanded an over 80 per cent share in this market. In the third quarter of the year, with the anti-China sentiment at its peak, there was a nine percentage points decline. This also resulted in market leader Xiaomi losing its crown to South Korean electronics giant Samsung — a 24 per cent share as against Xiaomi’s 23 per cent. This was, however, short-lived. In the next quarter, Xiaomi reclaimed its position with 26 per cent market share as against Samsung’s 20 per cent. In the first quarter of this year, too, the numbers were the same. The anti-China buzz has fizzled out in a matter of months.

“Chinese brands accounted for 75 per cent share in the March-ended quarter. Xiaomi led the market, followed by Samsung, Vivo, Realme and OPPO,” says Shilpi Jain, Research Analyst, Counterpoint Research. “The anti-China sentiment largely subsided by the end of the year with Chinese brands holding 75 per cent market share in 2020.”

While it may be seen as a missed opportunity for Samsung, it could be a bigger loss for homegrown brands such as Micromax and Lava that had planned a big-bang comeback by cashing in on the anti-China sentiment. All of that seems to have come to nought.

“It was a godsend but we simply couldn’t capitalise. Partly [because] we weren’t ready and we didn’t have the scale. The global semiconductor shortage also came out of nowhere and really hurt us,” says a senior executive with a homegrown mobile manufacturing firm. “Even if we were prepared with products and marketing, the parts shortage would have sabotaged our plans.”

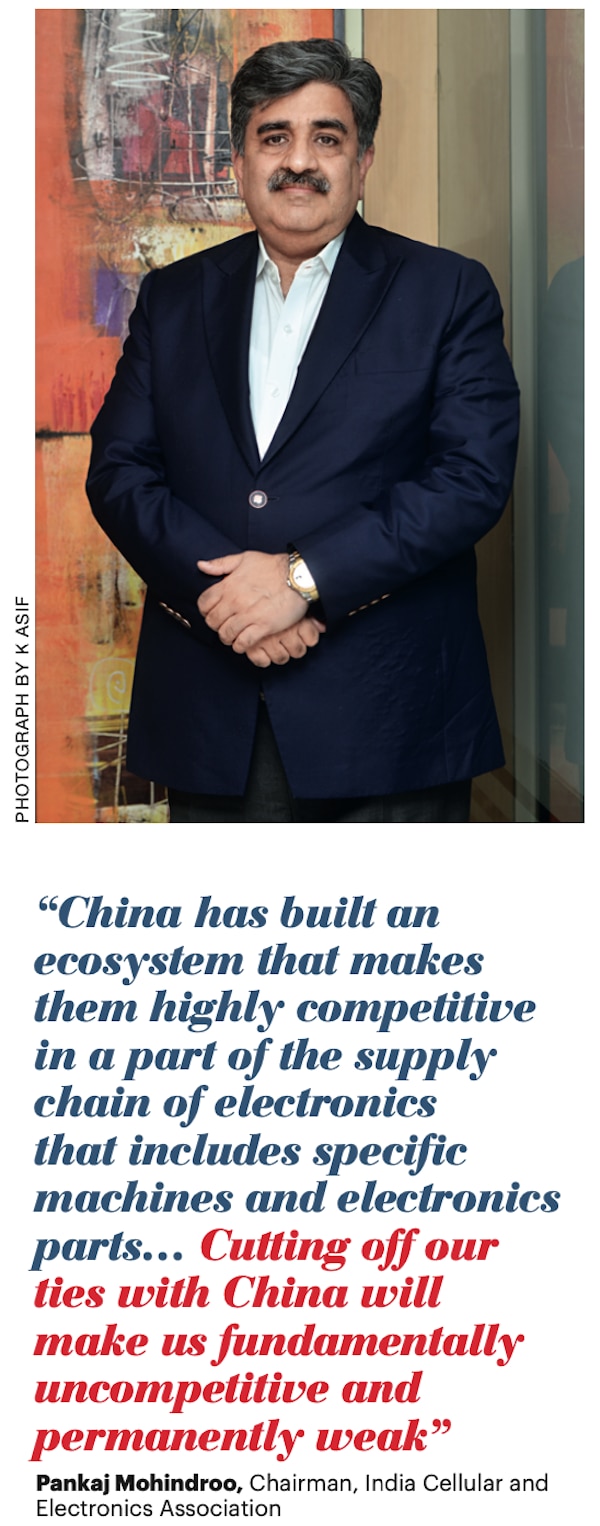

“Rationality always takes over emotions. Until the proposition of Chinese companies is matched, consumers will make a rational choice,” says Pankaj Mohindroo, Chairman, India Cellular and Electronics Association (ICEA). “However, if Indian companies can offer a similar proposition, many consumers will essentially go for non-Chinese products. It is a process. Once we create the ecosystem and domestic companies acquire the skills, the situation will change.”

The Tryst For Self-reliance

Is it game over, though? Not really.

The desire to become a self-sufficient economy is neither new nor original. It isn’t misplaced either as most countries in the world are aspiring for minimal import dependence. To do that, however, the domestic industry needs to overcome fundamental roadblocks such as high cost of capital and land, poor infrastructure, snail-paced bureaucracy and lack of adequate government support. All of this makes India Inc. uncompetitive in the global arena.

It is with this in mind that the government launched the ambitious Production Linked Incentive (PLI) Scheme, which offers a host of incentives across a gamut of sectors to make India capable of competing in the global market. The potential impact on trade ties with China is significant. It is also intentional.

“That policies will immediately change the overall trade dynamics in a globally integrated supply chain is too much to expect. In the aftermath of the Covid-19 pandemic, the Indian government took a series of measures to boost self-reliance in critical areas through the Aatmanirbhar Bharat initiative. This included raising tariffs on certain items to promote domestic industry and introduction of the PLI Scheme to boost domestic manufacturing,” says Varma of Primus Partners.

“While the government has introduced many such schemes to pursue the path of self-reliance, there is always a lag between implementation and results. Hence, it would be too soon to deem the government’s efforts as failure. Further, the pandemic has acted as an impediment to the quick rollout of such measures,” he adds.

The corpus for the various PLI schemes covering electronics and automobiles, textiles and pharmaceuticals, food and steel, is massive — nearly Rs 2 lakh crore. The first such scheme for manufacturing mobile phones and components has received an enthusiastic response with more than a dozen proposals.

“In the post-Covid economic scenario, globally there is a perception of manufacturing being shifted outside China as a risk diversification strategy. India, being a democracy, having independent judiciary and media, brings more comfort to global players as an alternative,” says Agarwal of BJP. “This is an added opportunity for attracting foreign greenfield projects to India. Initiatives such as PLI, the new Logistics- and Industrial Policy are helping in this direction. Efforts of some states like Uttar Pradesh are also bringing positive results.”

Much more needs to be done on land banks and land reforms, water, air, road and railway connectivity, setting up of district commercial courts and urgent notification of four Labour Codes.

If India can get right its localisation strategy, in electronics alone, the potential is significant. In printed circuit board assemblies (PCBAs) — the green colour board inside electronic gadgets that mechanically supports and electrically connects the components — ICEA believes that the current market size of $16 billion (FY20) will grow to $87 billion by 2025/26, representing a $71-billion opportunity in the domestic market. Thanks to the PLI Scheme for mobiles and smartphones, ICEA expects that 90-99 per cent of PCBAs will be locally assembled in future. Smartphones account for over 80 per cent of the PCBA market.

Similarly, in flat-panel displays, a surge in demand for consumer durables such as smartphones is likely to more than treble India’s market from $5.4 billion in 2020 to nearly $19 billion by 2025. Globally, the market for flat-panel displays was valued at $100 billion in 2020. It is projected to grow to over $125 billion by 2024. Mobile phone and TV product segments account for more than 65 per cent of industry revenues, while notebooks, monitors, tablets, automotive and other applications account for the rest. This offers an export opportunity for India of up to $11 billion per year by 2025. With a corollary benefit of reduction in imports, an estimated 2,00,000 jobs could be generated in the sector.

“Keeping politics in mind, India should ideally reduce the dependence because in case of a serious discord between the two countries, there should be a fallback option,” says Sabnavis of CARE Ratings.

This will, however, bear fruit in the medium to long term, and in the interim, India cannot wish away China — a country that has established itself as the factory to the world — just like that. More importantly, in-house manufacturing is capital-intensive and consistency in policy would be the key to scaling up. India needs to stay the course.

“China is a significant global factory. We need to use globally competitive inputs from China to be competitive in the world. However, we must also have a clear strategy to occupy a part of the global value chain. It would not only reduce our trade deficit with China but also create strategic interdependence,” says Mohindroo of ICEA. “This strategy would ensure that China cannot twist our arms with a similar dependence on the Indian supply chain to be globally competitive.”

For India to shrug off China’s oversized shadow, it will not be a T20 game but a hard grind. We are still not the best when it comes to Test matches.

@sumantbanerji