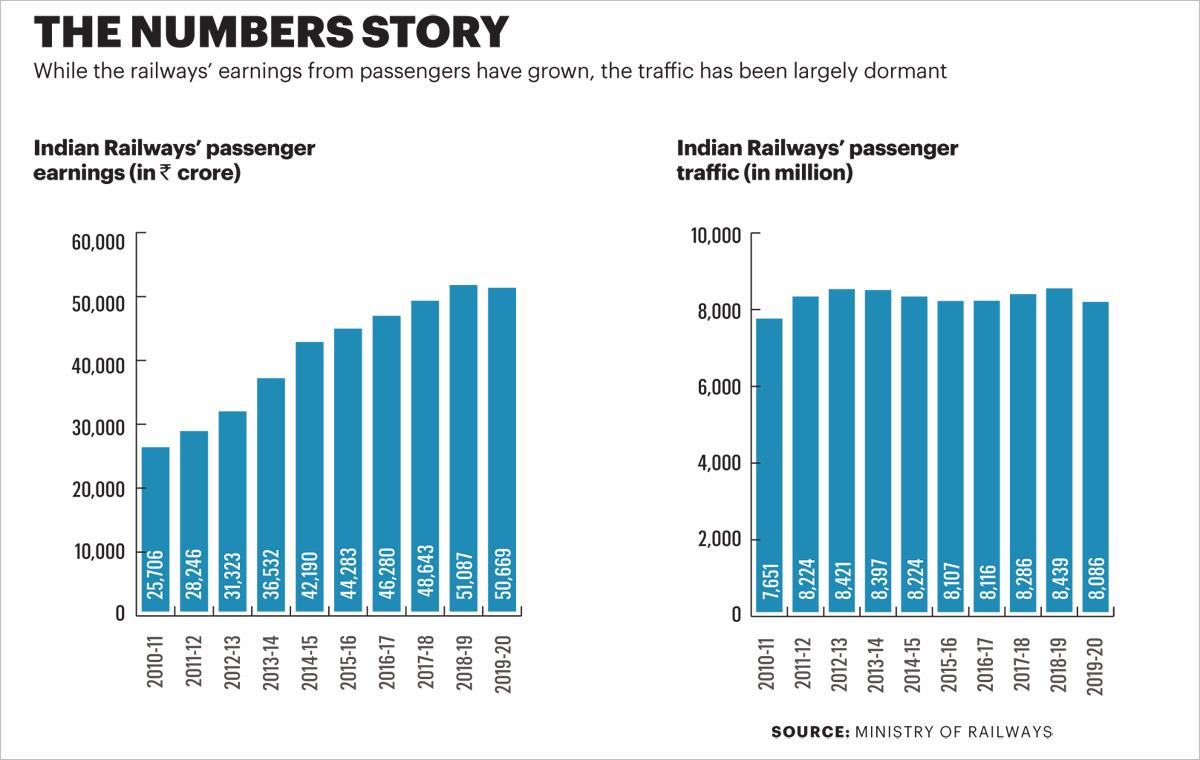

Rail bhawan in New Delhi houses the railway ministry’s apex decision-makers, including the railway minister. Somnolent during the initial months of the lockdown last year, the place was abuzz with activity in June 2020 as the halting of all passenger trains ravaged the Indian Railways’ already dismal finances. Freight volumes, at 241.66 million tonnes, were down 21 per cent in Q1 of FY20-21 compared to Q1 of FY2019-20. (Passenger receipts have been lowered 75 per cent in revised estimates for FY21 to Rs 15,000 crore from the Budget estimate of Rs 61,000 crore.)

To curtail the losses, the ministry decided to take the plunge on private passenger trains—a plan it had set in motion some time back by asking its public sector entity, Rail India Technical and Economic Service Ltd (RITES Ltd), to prepare a feasibility report. Such a public-private partnership (PPP) was a first as the government has always controlled the passenger segment, guided by the philosophy that the private sector would neglect the Railways’ social accountability. Now, though, the possibility of a world-class, on-time travel experience held more promise. As did the government’s potential to earn a pretty penny.

The idea was that the Indian Railways would provide the requisite supporting infrastructure and staff, such as pilots and guards, to the private operators. In return, the operators would pay fixed haulage charges, such as for electricity and track maintenance, as also a portion of revenue. The net present value (NPV) of the revenue share, assuming a 10 per cent cut, would be Rs 10,463 crore, according to RITES’s feasibility report. And the NPV of haulage charge would total Rs 26,346 crore.

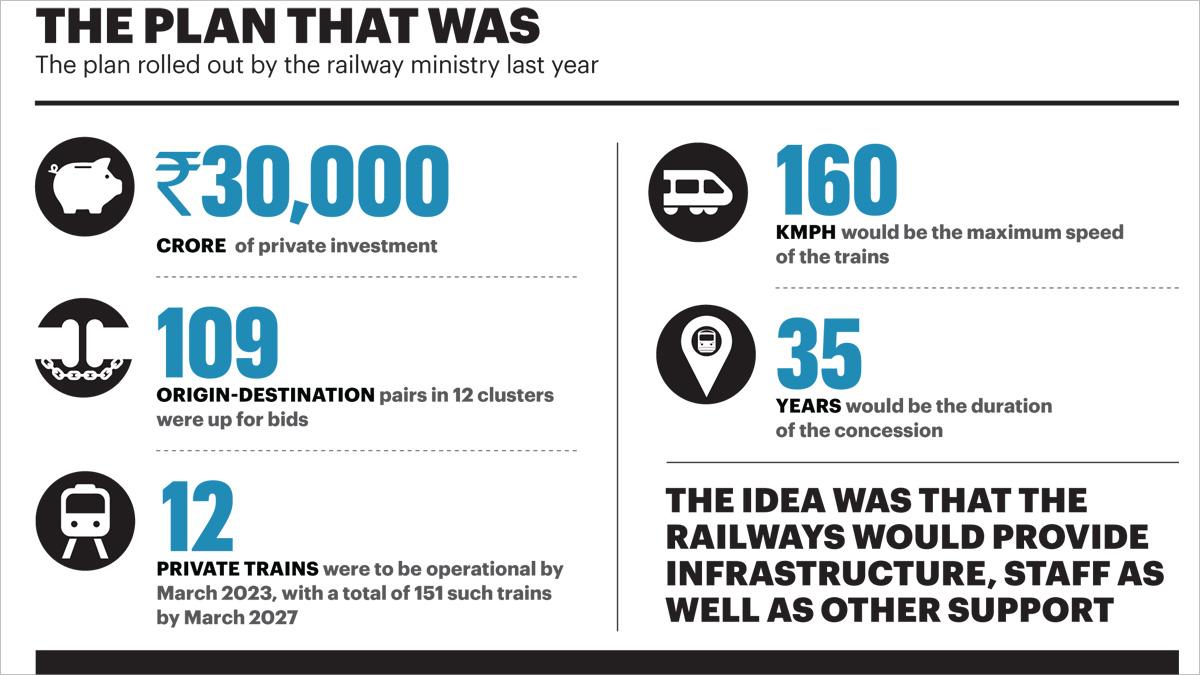

The railway ministry kicked off the Rs 30,000 crore-bidding process in July last year. Its request for qualification (RFQ) put 109 origin-destination route pairs up for grabs across 12 clusters including Delhi, Mumbai, Chandigarh, Prayagraj, Patna, Howrah, Secunderabad, Jaipur and Bengaluru. Each cluster has several routes that would be operated by the winning bidder.

At least 12 private passenger trains would have been operational by 2023, per the plan, and by 2027, 151 trains with modern rakes would crisscross the 60,000-km-plus railway network. Railways would have an additional revenue stream, the private sector would get a new business, and passengers would experience world-class travel.

The earnings from these 12 clusters wouldn’t help the Railways’ financials much but it would help build a model for private participation. Scaling this up with new routes would have ensured a healthier revenue stream for the Railways, which has been subsidising the losses in its passenger operations from gains in its freight service.

Losses from passenger and coaching services rose from Rs 31,727.44 crore in FY14 to Rs 46,024.74 crore in FY18, of which Rs 101.41 crore was left uncovered, according to the Comptroller and Auditor General (CAG) of India’s report last October. In that same period, the profit from freight services increased nearly 41 per cent to Rs 45,923.33 crore from Rs 32,641.69 crore.

The CAG report said earnings from freight operations in FY18 subsidised the losses on all passenger services, except the AC three-tier and chair-car classes. The report also said operational losses in AC first-class more than trebled from Rs 47.39 crore in FY14 to Rs 164.95 crore in 2017-18, while the losses in AC two-tier jumped from Rs 497.28 crore to Rs 604 crore. However, upper-class rail travel had grown at a CAGR of about 7.5 per cent between FY11 and FY19, the railway ministry found. And that formed the crux of the Railways’ plan to monetise its passenger operations and exploit an additional revenue source by roping in private players.

That plan, however, seems to be a far cry for now. When the bids were opened this July, after a year-long bidding process, they were worth a mere Rs 7,200 crore against the planned Rs 30,000 crore. The plan for private passenger trains had come to a standstill, even before it left the station.

Several private players expressed interest in operating passenger trains. The RFQ generated 120 applications from 16 firms in October last year. These included IRB Infrastructure Developers Ltd, GMR Highways Ltd, PNC Infratech Ltd, Megha Engineering & Infrastructures Ltd (MEIL), Gateway Rail Freight Ltd, Gateway Distriparks Ltd, Indian Railway Catering and Tourism Corporation (IRCTC) Ltd, Omaxe Ltd, and Cube Highways and Infrastructure Pte Ltd. Among the applications, 102 were eligible to place bids.

But a majority of them have since vanished.

The Rs 7,200 crore worth of bids came from two parties—Hyderabad-based MEIL and IRCTC, which the government recently listed on the bourses. They had submitted bids for 29 origin-destination pairs, well short of the 109 pairs on offer. According to railway ministry sources, MEIL is a non-serious bid, with a mere 1 per cent revenue-share offer. IRCTC, meanwhile, has offered to share nearly 10 per cent of the revenue it earns. The ministry has held several rounds of talks with both the bidders since this July but is yet to take a final call.

A railway ministry source, however, has indicated that the entire bidding process is likely to be scrapped in favour of a new one. “The current tenders for private train operations will be discharged and fresh bids, with changes in the provision for private participation, will be rolled out soon. The ministry has started work on fresh bids based on the learnings from the recent process,” the source said. An email seeking comment from the railway ministry remained unanswered.

But Suneet Sharma, Chairman of the Railway Board, is confident. “We are sure that with the interest shown so far by the local and global investors and by the industry, we will be able to achieve the targets we have set. We have also formulated certain mechanisms by which we will monetise our assets, be it trains, the dedicated freight corridor, or railway stations. We have got a structured way of going about these because these are different areas of work and require different approaches,” he told Business Today. The fact of the matter is that bidders seem to have lost interest midway during the process. But what turned them away?

There are several reasons for the lack of interest, say experts. The chief concerns include bid provisions such as revenue sharing that heavily favour the ministry, no administrative control over the staff deputed by the Indian Railways, and penalties for not meeting key performance metrics such as punctuality, cleanliness and maintenance. But the biggest sticking point was the railway ministry being both the regulator and a competitor.

“I do not think anyone is surprised by the outcome,” says Manish Agarwal, an independent infrastructure expert. “The concerns that everyone wanted to be addressed were essentially to do with Railways as a regulator and as a competitor. A financial regulator may not be needed but an independent technical regulator is imperative for common operating rules.” He believes the rail ministry was too focused on protecting the downside while trying to maximise the upside.

That view is echoed by Ashish Gupta, Deputy Managing Director at freight car manufacturer Texmaco Rail and Engineering Ltd. “The biggest confidence booster for the industry would be an independent regulator. Look at the telecom sector. It flourished because there was an independent regulator. Also, policies need to be made more investor-friendly,” says Gupta.

Jatin Aneja, partner at law firm Shardul Amarchand Mangaldas & Co, says competing with the Railways for tariffs was another major concern. “Unless there is a huge difference in the user experience, including the time taken, passengers may not want to pay a higher fare,” he says. Agarwal drives home the point with an example. “If the Rajdhani fare is a benchmark, a major concern is what happens to the private trains if Rajdhani’s fares drop or do not increase.” The government, he adds, has the luxury of operating with losses, but not private players.

The prospect of revenue sharing on top of predetermined haulage charges was also a concern. “The commercial structure was set up in such a manner that there is a haulage charge irrespective of passenger footfall and revenue share over and above that haulage charge,” says Agarwal. Further, Aneja questions why private operators should bear the penalties in case of delays when they are dependent on the Railways for staff.

Another massive hurdle in the Railways’ privatisation plan is the strained line capacity in the sections that will run the private trains. The capacity is over 100 per cent and tops 150 per cent in some cases, according to the RITES feasibility report. The capacity will only increase further if infrastructural improvements are expedited as the number of freight and passenger trains is rising each year, the report adds.

Railway officials say the completion of the dedicated western and eastern freight corridors will ease some of the capacity and make passenger operations more feasible. But the two sections completed so far account for only 650 km of the 3,381 km-long corridor that has been in the works for more than 15 years. And, given the multiple extensions, meeting the latest deadline of June 2022 seems a tall order.

By all counts, the Railways’ private train journey seems to have stopped in its tracks. But there are lessons from an unexpected source.

In an ironic twist of fate, while India is keen to rope in private partners to run passenger trains, its erstwhile colonial ruler is doing the opposite. The UK’s Prime Minister, Boris Johnson, recently announced plans to bring the railways back under government control after nearly three decades under the stewardship of private entities, largely on a franchise model.

The UK plans to dismantle the franchise system and set up a state-owned body—the Great British Railways— that will operate trains, regulate fares and manage infrastructure. Why? The short answer is a crumbling railway infrastructure as years of private ownership compromised on investments to upgrade the network. The longer answer needs a detour into the past.

After Margaret Thatcher became the PM in 1979, she announced a slew of initiatives, including the privatisation of state-owned companies, to revitalise the economy. Several institutions went private, including British Petroleum, British Airways and Rolls-Royce. But the railway network was untouched due to political considerations of the Conservative party under Thatcher. When Thatcher lost control in 1991, her successor moved swiftly to right that wrong, at least according to them.

The European Union, at the time, had made a clear distinction between providing transport services and operating the infrastructure. The EU deemed it “necessary for those activities to be separately managed and have separate accounts” for the “development and efficient operation of the railway system.” Beginning in 1994, the trains of British Rail went to three rolling stock companies, while the freight operations were hived off to six newly formed private companies and the franchise model was adopted for railway passenger services. However, the private operators made highly competitive bids and ultimately ended up running into losses and defaulting on their dues to the government, which hurt the exchequer.

Moreover, these private entities focused solely on making money and neglected to upgrade the railway infrastructure. This is what Johnson seeks to correct by re-nationalising British Rail.

There are, however, two key distinctions in India’s privatisation model. Firstly, India is not selling its rail routes and assets lock stock and barrel as the UK did. Secondly, it is not transferring the title and the rights of the assets. Rather, it has a concession model for a fixed period over which the private entity can earn a return on its investment while sharing revenue with the government. At the end of this period, the rights are transferred back to the government. The similarity between the Indian and UK situations is that their domestic railways are in dire straits. That is what each country seeks to address, albeit in opposite ways.

Given the recent bidding experience, experts are divided over the government’s next course of action. While all of them see the immense potential in the privatisation plan, their views on the path ahead range from cautious to optimistic.

Agarwal, who is among the cautious ones, says this is yet another missed opportunity for the Indian Railways, which has a chequered history as far as PPP is concerned. “This team could have demonstrated that the Railways could have competed with air travel or taken on super luxury buses. Success on this front would have disciplined the operations. It would have helped everybody. Today there is no timetable, which impacts businesses in India and Railways’ revenue.” He adds that the key learning for the Railways should be “altering the risk-sharing model” for projects of this magnitude.

Kushal Kumar Singh, partner at Deloitte India, agrees with this. He believes that the bidders did not fully understand the concession agreements for the private operators. Singh says the railway ministry has two options now. “For the clusters in which the Railways did not get any bids, it must re-engage with the private players and reissue the RFP. The second option could be to hold wider stakeholder consultations and see if the model needs tweaking.”

Texmaco’s Gupta, meanwhile, is so bullish that he has started aligning the company’s investments with the government plans. “While the government has a lot of good intentions on the private train operators, these are early days and teething problems cannot be ruled out. We have plans to get into manufacturing locomotives for the private train operators, so we are looking at getting into an alliance with global partners. We are geared up to tackle demand from the private players and are in the process of selecting a design team,” he says.

Of course, much more than Texmaco’s future is riding on the government’s next steps. However, it is clear that the responsibility for an optimal risk-and-revenue-sharing model for private passenger trains rests on the shoulders of both the Indian Railways and the private bidders. Only that will ensure that the privatisation bandwagon transforms from a handcar into a bullet train.

@eco_no_money