It has been a busy 12 months for Punit Goenka. Sitting in his spacious room in Zee Entertainment Enterprises’ central Mumbai office, the relief on his face is palpable. He has just signed a deal to merge Zee, where Goenka is the MD & CEO, with Sony Pictures Networks India. Though the deal was in the making for over a year—as is normal in M&As—valuation was a contentious issue. With a combined revenue of $1.79 billion, this would be the second largest entertainment network after Star & Disney India, which has revenues of $1.8 billion, a shade more than the new entity. Importantly, the Zee-Sony entity will have 75 channels and a strong presence in entertainment, sports and regional markets, making it a serious player.

The sequence of events that led to the deal is quite apt for two companies that create content from such storylines for a living. The first move was made by Sony in November 2020, but that offer was not acceptable to Goenka. Things started moving about three months later when KPMG reached out to him on behalf of Sony with a better valuation. By August 2021, he was in the thick of it. “I was in London on holiday, but constantly on the phone with my team back here to thrash out the deal,” reveals Goenka. Why was Sony interested? N.P. Singh, MD & CEO of Sony Pictures Networks India, says his company wanted to expand its footprint. “For a while, we had discussed the possibility of doing something with Zee. Once we were clear, I took it to my bosses.”

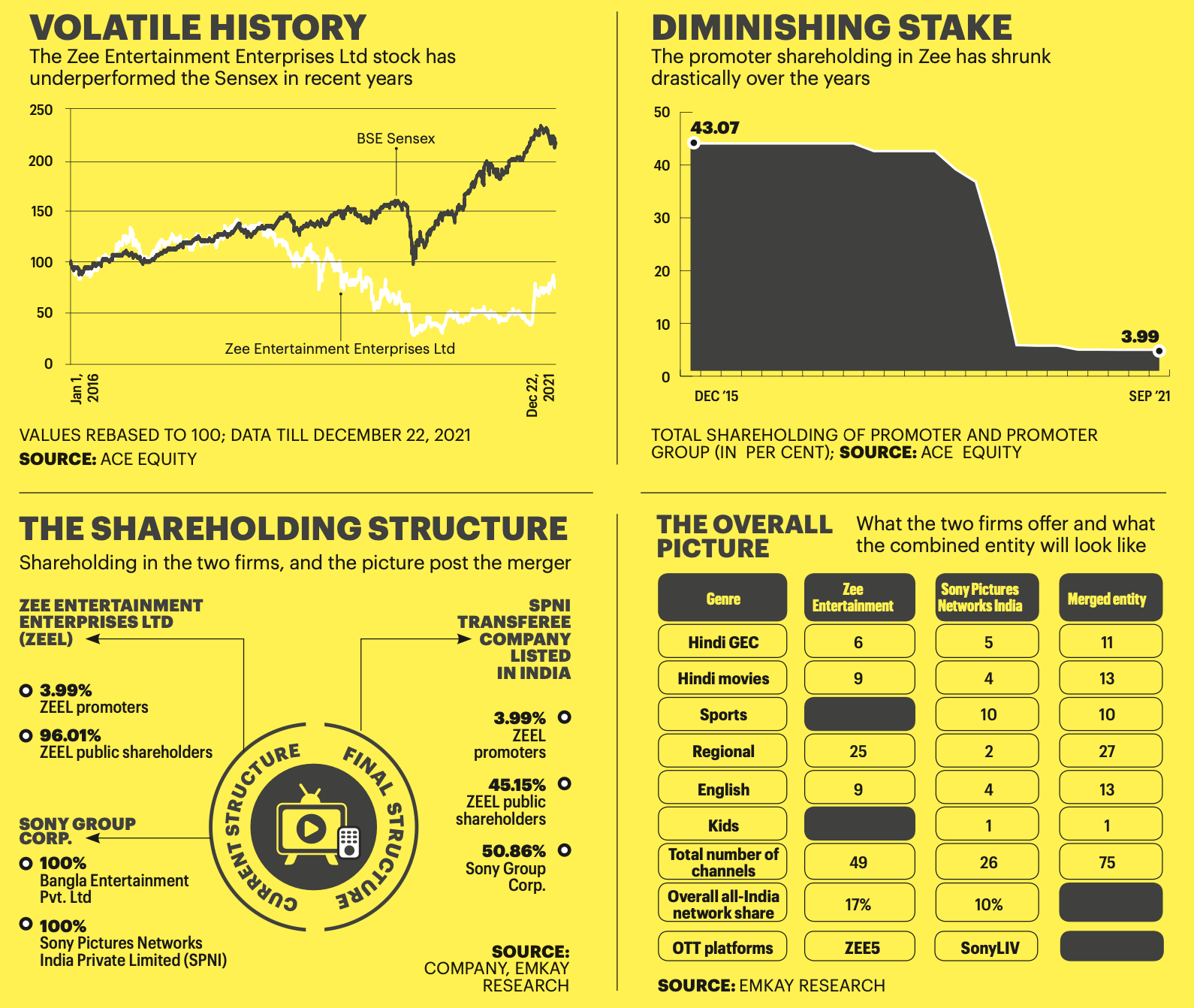

The basic contours were agreed on, and a board meeting was scheduled for October. All hell broke loose when Invesco, the Atlanta-based investment management firm that holds an 18 per cent stake in Zee, accused it of corporate mis-governance. (Invesco did not respond to queries from Business Today.) Goenka and the promoters (Zee was started by his father, Subhash Chandra), with just 4 per cent stake, had limited say. “I told Sony about what was going on and left the decision to them,” he admits.

On September 22, Zee announced its plans to merge with Sony, and the deal was inked three months later. In the merged entity, Sony will hold a 50.86 per cent stake, while the promoters of Zee will hold 3.99 per cent. The remaining 45.15 per cent will be with Zee’s other shareholders. However, this is merely the beginning of what will be a long process: getting approvals at several levels; Zee having to deal with an angry Invesco, its largest shareholder; and the fact that both entities need each other in a challenging scenario, where growth is hard to come by.

A Tale of Two Embattled firms

Both the companies have been on a difficult wicket lately. Zee struggled with hard questions from Invesco, with Zee’s promoters having limited bargaining power (see Diminishing Stake). Plus, with a hefty debt (around Rs 11,000 crore at the group holding company level), there was only so much Zee could do. A deal with Viacom18 was also considered but fell through. “Sony has come in as the white knight in this case,” says Vivek Menon, Managing Partner at NV Capital, a media and entertainment credit fund. To him, Goenka’s experience in broadcasting (he took over as MD & CEO in 2008) is useful, more so given that “he learnt the ropes from his father”.

Not all is well at Sony, too, here in India. Till 2017, the network had the broadcast rights to the Indian Premier League (IPL), the country’s marquee cricket tournament. Between FY15 and FY18, its revenue almost doubled from Rs 3,342 crore to Rs 6,277 crore, while net profit shot up 6x. But in September 2017, Star & Disney India (then Star India) bagged the IPL broadcasting rights, and Sony’s revenue stagnated (Rs 5,640 crore in FY21), while net profit dropped to Rs 564 crore from Rs 976 crore in FY20.

For a broadcasting network, only a handful of channels brings in the revenue. In the case of Sony, according to its annual report for FY21 sourced from the Registrar of Companies (its Indian operations are unlisted), 46 per cent of its revenue comes from advertising (that means Rs 2,563 crore), with subscription’s contribution being 42 per cent (Rs 2,329 crore) and the rest coming primarily from licensing. Here is where one needs to take a closer look at the advertising revenue figures. The company’s flagship channel, Sony Entertainment Television, point out industry trackers, brings in around Rs 1,000 crore each year (Zee’s primary channel, Zee TV, also makes that kind of money), while Sony SAB and Sony Max garner approximately Rs 450 crore and Rs 375 crore, respectively.

Says Karan Taurani, Senior Vice President, Elara Capital: “It has been a difficult phase for the television broadcasting industry. The rapid shift towards digital advertising and overhang of the new tariff order will restrict subscription revenue growth. While the regional pie is growing in double digits, the corresponding number for Hindi general entertainment is in the low- to mid-single digits.” The real rub: Sony has negligible regional presence—one channel each in Bengali and Marathi—and together their revenue is less than Rs 100 crore each year. “The regional story has been disappointing for Sony and that is where they need Zee quite badly. What Zee has done in the south or Bengali or Marathi through organic growth is impressive,” says a rival broadcaster.

In addition, investment bankers point out that the folks at Sony saw merit in going with an entrepreneur-driven culture. “The owners have been hands on at Zee and that is the only way to make money in India’s broadcasting business. The professionals-led approach adopted by Sony and Star always comes with limitations,” says an investment banker on condition of anonymity.

‘WE WANT TO GET THE BUSINESS BACK ON TRACK’

Zee Entertainment Enterprises’ MD & CEO Punit Goenka speaks on some key aspects of the merger. Edited excerpts:

Have you spoken to Invesco about the proposed merger?

The matter is subjudice and we have not discussed it. We want a resolution to the issue. We do not have a problem and it was they who went to court.

Tell us about the non-compete clause with Sony.

The non-compete agreement was a part of the deal. The Zee promoters will get an additional 2 per cent stake in line with this, which will be transferred by Sony. This transfer is in lieu of Zee’s promoters not entering into a conflicting business.

From a clear majority holding in Zee, you hold just 4 per cent today. How will this work?

The emotional tag of being the largest shareholder was over in 2019. We are aware of our status of being a minority shareholder and the objective is to bring stability back to the business. I still think like an entrepreneur regardless of how much I hold.

What about the proposed increase in your shareholding to 20 per cent?

It is not a priority for the moment. The most important thing is to get the business back to its days of glory. With our shareholding of 4 per cent, our board seat remains intact. I will be the MD & CEO of the merged entity reporting to the board. Sony will have a majority of members on the board.

Cricket Holds the Key

Goenka is clear that a cricket strategy is needed today. “If you want to be in a position of leadership in digital, you need sports, and within that cricket is a must,” he says. Making a demarcation in the audience profile, he emphasises that early adopters of digital are the youth. “The female audience and the older generation will take the linear [television broadcasting] path. If we want to get the youngsters, sports is the way to do it.”

To his mind, nothing changes when it comes to Zee being a content company. “That is irrespective of the platform and we have to own it. This is where OTT becomes critical,” he maintains. Of the three large television screens in his room, two play a live feed while the other is reserved for OTT viewing.

In the first quarter of FY22, a webinar was organised for analysts and a few investors. It gave the participants a chance to get up and close with Goenka on how he viewed the business. In this session, he spoke openly on how the broadcasting story for Zee was in place. “But we need to crack the OTT game. My organisation has people working in silos and to integrate them is the only way to bring down costs,” he told the gathering at the time. According to one participant, Goenka opened up on options such as charging for micro content, which could be, for instance, a musical show. Here, the consumer pays only for specific content instead of getting locked into a plan.

“The impression a lot of us got was that a new digital platform was in the works. The non-compete fee (where Sony is paying Zee’s promoters Rs 1,100 crore, with that amount to be used by Zee to retain its original 3.99 per cent stake in the merged entity; see ‘We Want to Get the Business Back on Track’) in all likelihood is being paid for this,” says the person quoted above. He explains that Zee understands distribution in broadcasting but not in OTT. “Netflix and Amazon are the best here. With the merger, Sony will want to build on Zee’s digital platform and that is why they need Goenka.”

In just about a month from now, the bidding for the five-year (2023-27) broadcasting rights for the IPL will get under way, for which Star & Disney India had forked out Rs 16,348 crore for 2018-22. That amount was twice as much as what Sony had paid for 2008-17. Even the most conservative bet on the street suggests that it will easily get past Rs 30,000 crore this time. Goenka says Zee will bid independently since the merger is still in the works. “We will be prudent about our bid,” he says. Recently, Zee returned to sports broadcasting by acquiring the global media rights for the upcoming UAE T20 league for a 10-year period (the amount paid out was about $100-120 million). Sony’s Singh says, “We will certainly evaluate the IPL. After all, we were the first to take a bet on the tournament.”

It is expected that Star & Disney India, too, will be there, although all eyes are on Mukesh Ambani’s Jio, which, with its large telecom base, is expected to be very aggressive. His broadcasting network, Viacom18, has no cricket now and needs it badly. Elara’s Taurani thinks Zee may not be that aggressive. “Being a listed company, it cannot afford a situation where a big-ticket investment fails to deliver value to shareholders. A higher acquisition cost will negatively impact profitability. This may enable Disney or Jio to aggressively bid for the IPL,” he says. With an assured audience cutting across age groups, there is a lot a broadcaster can gain through the IPL. Much as the rights for the ICC (including the World Cup across formats) and BCCI (for all cricket played in India) too come up later, nothing is quite as important as the IPL.

The Final Marriage

The Zee-Sony merger is a complex affair. Goenka expects it to be completed around August 2022. There are many layers to this and a big one is Invesco, whose appeals against Zee are pending in the National Company Law Tribunal (NCLT) and Bombay High Court. Avanti T. Chandele, Partner, Mind Legal, says: “Under the Companies Act, 2013, a scheme of arrangement is to be approved by 75 per cent votes cast in its favour.” She thinks Invesco may request for a stay on the merger process. “Under Section 230 of the Companies Act, shareholders with at least a 10 per cent stake may object to the merger and that could be an area of concern. However, to stall the merger, Invesco would need at least one-fourth of the shareholding, which they may not be able to muster,” she says.

According to Chandele, Zee and Sony will have to file a detailed notice with the Competition Commission of India since the merger has the potential to create market dominance. “The approval from the Ministry of Information and Broadcasting will also be required apart from the stock exchanges and SEBI.” Further, NCLT may take 6-12 months to adjudicate upon the merger.

So, where does that leave Invesco and its case? Shriram Subramanian, Founder & Managing Director at InGovern, a proxy advisory firm, says in the absence of an alternate plan, “it would be imprudent of Invesco to vote against the merger, which will result in a new direction for the company as a media leader and subsidiary of an MNC”. He is clear that, as the largest shareholder, Invesco would do itself and other investors more damage than good if the merger does not go through. “Information that was made available in the past couple of months point to the fact that they were comfortable with similar deal structures. The legal cases only benefit the lawyers and are a distraction for management and investors.”

Every large M&A deal is ironic in more ways than one. In September 2016, Zee sold its sports network business (the Ten Sports portfolio) to Sony for $385 million at a handsome return—this was originally bought from Dubai’s Taj Group for $107 million. “Internally, we kept joking that it would come back to us. Today, it has,” says Goenka. Indeed it has, but there is a lot of work to do for both the entities in a scenario that is vastly different from the past. Zee and Sony will be only too aware of that.

The future, then, will be full of hope and trepidation in equal measure.

@krishnagopalan