Retirement years are meant to be stress free. But managing retirement incomes may not be so. One has to keep in mind various challenges that could crop up in such times of crisis like the one we are witnessing. It presents a dual challenge - preventing one's regular income from falling, and making sure that any health emergency does not erode a significant part of the retirement corpus. There are plenty of investment options available, but since most of them involve a fair amount of equity exposure, most senior citizens prefer to stay away, given the kind of corrections seen recently.

Where are interest rates headed?

The level of interest rate is the biggest factor that determines the return on investment and the amount of regular income that a senior citizen can expect. Barring some exceptions, interest rates have been declining for the last one decade, with the sharpest fall coming in the beginning of the year. "So far in 2020, the RBI made reductions in the policy repo rate twice, reducing it from 5.15 per cent to 4 per cent" says Archit Gupta, Founder and CEO, ClearTax.

"Given the current situation where economic activities have been impacted, consumption is low and revenues are unlikely to pick up in the near future, the RBI will try to keep the interest rate low to support growth. The repo rate may reduce by 0.25 per cent to 0.50 per cent from 4 per cent if the lockdown continues in its current state. Interests on savings account, liquid funds and fixed deposits could also reduce for two to three quarters and are expected to rise thereafter as economic activities start stabilising," says Harshad Chetanwala, Co-Founder, MyWealthGrowth.com. While there may not be a significant fall in interest rates, any revival looks at least three to four quarters away.

What Should Senior Citizens Do?

A wait-and-watch approach could result in a long wait, and one will lose the best-offered rates in the current situation. "In such a situation, anyone with an investible surplus can look at an allocation-based strategy instead of investing in a staggered manner. The maximum allocation should be in the short-to-medium term (1 - 3 years) options. Avoid locking investments in long-duration options currently," says Chetanwala.

Senior citizens therefore should divide their investable surplus into long-term and medium-term investments. While long-term investments will bring stability in regular incomes, medium-term investments can be used to cash in on any opportunity arising due to rising interest rates.

Some banks offer attractive interest rates for senior citizens. Besides, many small saving schemes also offer good returns. "Senior citizens generally look for risk-free returns such as deposits in banks or post offices. Banks generally offer special rates for senior citizens, which are higher than regular deposits. Also, interest rates on savings schemes are unchanged in the second quarter until September 31, 2020. Senior citizens can accordingly base their investment decisions on prevailing interest rates, investment amount and rate of return," says Gupta of ClearTax.

Senior Citizens Savings Scheme

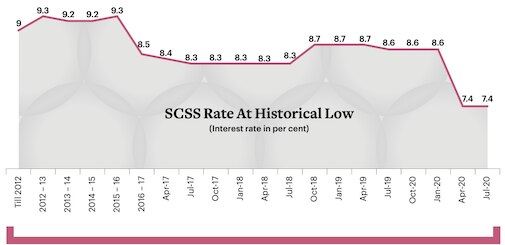

Senior Citizens Savings Scheme (SCSS) is the one of the must have options for senior citizens since it ticks all the right boxes. "Despite the decrease in interest rates, Senior Citizens Savings Schemes are a good investment avenue for risk-averse senior citizens for a number of reasons -the interest is a little higher compared to the rest, you can avail an exemption of up to Rs 50,000 on interest earned from SCSS under section 80TTB of the Income Tax Act, and the interest is payable on quarterly basis that can help in maintaining cash flow," says Rishad Manekia, Founder & Managing Director, Kairos Capital Private Limited, a Mumbai-based financial planning firm.

So, should you invest the entire money at one go or in parts? "This product gives the highest sovereign, safe rates of return. Since most senior citizens get their money in bulk on retirement, if they don't park it here, any other safe avenue is likely to be give low interest. Hence, I recommend them to park their intended amount at one go," says Col Sanjeev Govila (Retd), a Sebi-registered investment adviser (RIA).

The maximum investment limit for this scheme is Rs 15 lakh, which much less than what many people accumulate by the time of retirement. At the current rate of 7.4 per cent, it gives a quarterly income of Rs 27,750 (Rs 9,250 monthly0, which may not be sufficient. The five-year tenure is also not very long, so one should not mind utilising the maximum possible amount of SCSS in his/her retirement portfolio.

Pradhan Mantri Vaya Vandana Yojana (PMVVY)

It is a Central government scheme managed by Life Insurance Corp (LIC) as an immediate annuity product. It gives the option to receive monthly, quarterly, half yearly or yearly payout. At present, it offers the same interest rate as SCSS - 7.4 per cent on monthly payout. The maximum amount one can invest is Rs 15 lakh, which gives a monthly pension of Rs 9,250.

"Unlike SCSS, PMVVY scheme does not provide a tax deduction benefit under Section 80C of the Act and there is no exemption from tax on returns in this scheme. So, senior citizens should think of investing in PMVVY only when they exhaust the investment limit under SCSS. A longer lock-in period of 10 years, compared to five in case of SCSS, is also a deterrent for PMVVY," says Manekia of Kairos Capital.

It is a good product when it comes to interest rate, but being a long-term product of 10 years, one should invest only a part. "If interest rates rise subsequent to investment, as in the current scenario where interest rates are almost at the rock-bottom, there will be a notional loss involved. However, considering the current crisis, it may be quite some time before rates rise again. Hence, staggered investments may actually be less advantageous due to the long intervening periods anticipated before rate hikes," says Col Govila. What it means is that if it takes two to three years for interest rates to rise, one may end up losing a significant amount just by waiting for rates to rise.

While PMVVY is one of the most recommended products, one should go for other immediate annuity options provided by life insurance companies. If one is getting a good annuity rate and looking to invest some part of the corpus for a lifelong stable income, one should consider it. However, it is not for those planning to invest a major part of their retirement corpus.

"It has many disadvantages, which should make it one of the least options for retirees. Low rates of return, typically in the 4-6 per cent range, and full taxability place it much lower in the pecking order. No access to original capital or even facility for premature withdrawal of capital, inability to give positive inflation-adjusted returns, and simple interest payment vis-a-vis compound interests for most other instruments make it a not-so-good option," says Col Govila.

RBI Floating Rate Bonds

RBI Floating Rate Bonds are one of the popular investment options for regular income. Though it does not give any special privilege to senior citizens, it has one of the highest interest rates. "Floating Rate Savings Bonds issued by the RBI is a good investment option for senior citizens considering the fact that it is sovereign guaranteed and returns are 0.35 per cent higher than NSC" says CS Sudheer, Founder & CEO, IndianMoney.com.

Though it gives one of the best rates compared to bank fixed deposits, it lacks liquidity. "There are two concerns - one, there is no liquidity since those who are aged between 60 and 70 will be able to withdraw only after six years, 70-80 after five years, and above 80 after four years. And second, there is no monthly interest payout. It is paid once in three months. The RBI is compensating these two concerns by offering higher returns than NSC," adds Sudheer.

Unlike SCSS and PMVVY, these bonds offer floating rates of interest. So, one can take advantage of interest rate hikes. In the current scenario when interest rates are at record lows, this offers a good option since there will be no notional loss if rates rise.

FDs and Post Office Monthly Income Scheme

Many people who do not want to lock in funds for 10 years in PMVVY or RBI Bonds, or are still left with surplus funds after all investments could consider the Post Office Monthly Income Scheme. It currently offers an interest rate of 6.6 per cent.

Some part of the retirement corpus should be kept in easily accessible funds. Fixed deposits offer the desired flexibility to liquidate at will and at the same time earn a good interest rate. "Senior citizens can invest the special fixed deposit scheme of various banks, which offer interest of 6.5 per cent for senior citizens. The amount and tenure of deposits vary from bank to bank. The interest is higher than the interest offered on regular fixed deposits," says Gupta of ClearTax.

Debt Mutual Funds

When it comes to keeping some part of your liquid investment, which can also earn regular income, one can consider debt mutual funds. "Investing in safe debt mutual funds like Money Market funds, and carefully chosen Banking & PSU debt funds, and Ultra Short-Term funds, and then choosing the Systematic Withdrawal Plan (SWP) option for pension would be more efficient tax-wise, and give more flexibility in regular or bulk withdrawals" says Col Govila.

Monthly Income Plans (MIPs) from mutual funds are specially designed to meet the needs of senior citizens. They give regular income in form dividend. However, due to changes in the Dividend Distribution Tax (DDT) it is better to go for growth options. "I dont suggest them to go with the dividend option, but instead opt for the growth option and then go for the Systematic Withdrawal Plan so that one can have a steady income and will save a decent amount of tax as well," says Sudheer of IndianMoney.com

"Withdrawal from debt funds can be planned after three years or more holding to take benefit of indexation. This also helps in reducing the tax burden," says Chetanwala.

Health Insurance

A medical emergency can erode a big part of the retirement corpus, which in turn can jeopardise one's retirement planning. A health insurance plan can help one manage this risk at a much lesser cost. An active health plan with adequate cover is the best suited. Opt for one immediately if you do not have inadequate coverage.

There are certain things that one should keep in mind while choosing a health insurance plan. Insurance premiums increase with age options get limited. The insurance regulator, IRDA, has asked health insurers to offer plans till the age of 65.

"Senior citizens must look out for clauses like co-payment, sum-limits and extent of coverage for pre-existing diseases along with waiting period," says Amit Chhabra, Head, Health Insurance, Policybazaar.com.

One also needs to check whether the policy offers a lifelong renewal option or not. "Age plays an important part while investing in health insurance. You should choose a plan that goes well with your age and needs as well. Choose a plan that offers coverage for a longer tenure. Some insurance companies provide health insurance plans for those below 65. Only some companies offer coverage without any limitations," says Naval Goel, CEO & Founder, PolicyX.com.

So, pick a good cover amount as early as possible. "The sum insured is another vital aspect that one should consider while investing in a senior citizen's health insurance policy. With growing age, health risks increase, and hence senior citizens need high health insurance protection," adds Goel.

Make sure that your plan covers all major disease threats based on your personal and family history. "The chosen plan should cover a broad range of illnesses, particularly critical illness as chances of the same are higher with age. One must check all the terms and conditions related to exceptions," says Goel of PolicyX. Add the coverage of pre-existing diseases and applicable waiting period.

Co-payment is the facility in which the policyholder pays a part of the claim amount each time a claim is made. "Co-pay is the fixed amount that the policyholder pays from his pocket for services covered. Normally, all insurance plans come with a co-payment clause depending on the treatment and medication required. Senior citizens should opt for a plan that charges a lesser percentage of a co-pay," says Goel.

Co-payment helps you get a policy at a lower premium. So, it is a good option if one does not have any medical complication or family history, and do not expect any near-term hospitalisation. "Senior citizens without any pre-existing diseases and who are unlikely to get hospitalised in the coming few months must go for plans that come with a co-payment option," says Chhabra.

Earlier, there were hardly any health policy options after the age of 65, but that's not the case anymore. "There are multiple health insurance plans that a person can opt such as Bajaj Allianz Silver health senior citizen health insurance plan, Religare Care Senior, HDFC ERGO Health Optima Senior, Star Health Senior Citizen Red Carpet Plan and much more," says Goel of PolicyX.

Income Tax Leakage

One should make sure that no TDS is deducted if one is eligible. "In the case of bank deposits, SCSS and post office monthly income schemes, there is no TDS on the interest earned from each of them, up to Rs 50,000 per financial year. Senior citizens who have nil tax liability can also file Form 15H with the respective bank or post office to claim income without TDS," says Gupta of ClearTax.

Besides the usual income tax deduction, senior citizens also get an additional deduction. "The interest earned is taxable income of the senior citizen. A tax deduction up to Rs 50,000 is available on the aggregate interest income earned in a financial year from banks and post offices under section 80TTB," adds Gupta.

SCSS is a pure investment option where you can enjoy section 80C deduction. "An investment in SCSS is also eligible for tax deduction under Section 80C in the year of making an investment. The maximum deduction available is Rs 1.5 lakh," says Gupta. For health insurance policy, you get a deduction of up to Rs 50,000 under Section 80D.

@naveenkumar