Financial planning for children is not simple. As you play with your newborn baby, you must also play with numbers to estimate the future cost of higher education, and marriage. Consider this: The MBA course from IIM Ahmedabad costs Rs 22 lakh. The cost could go up to a whopping Rs 70 lakh in the next 20 years. A wedding that costs Rs 10 lakh today could cost Rs 43 lakh after 25 years. The figures factor in a rather moderate annual inflation of 6 per cent.

The burden of planning for your child's future usually emerges while you are jostling with the challenges of improving your professional life and bearing his or her school expenses. You also have to save enough for your retirement. Doing all this appears daunting and indeed is a rigorous exercise but can be done easily if planned well in advance. Here is how you can handle it:

Define Future Goals

The first thing you must do is to jot down goals along with the time period within which you would like to meet those goals. "The possible large expenses that need planning are education and marriage. The simple way is to find out today's cost and compound it for inflation to estimate the fund required in the future," says Abhijit Bhave, CEO, Karvy Private Wealth. You must save separately for both these major goals. Higher education should get more priority since you may have more flexibility with marriage expenses.

While it is easy to guess the year of graduation or post graduation of your child, estimating the savings required is tricky. Most parents face a shortfall when the actual cost hits them. The cost of higher education has been growing rapidly, so you have to revise your estimates keeping inflation in mind. "Institutes that have consistently demonstrated high quality of education on account of their courses, faculty, facilities and partnerships/collaborations with global institutes of repute have greater student attraction power and can command higher fees as compared to other institutes," says Anindya Mallick, Partner, Deloitte India. "Legacy as well as new-age institutes offering a world-class student experience have developed their own brands, and with demand exceeding supply, they can charge significantly higher fees which students are willing to pay," he adds.

Besides higher education, parents should also be aware of offbeat career options - sports, music, fine arts, and others - that the child may take up. While you plan for education, you should also consider ancillary costs of tuition, coaching, gadgets and equipment. This could turn out to be substantial and needed much before the graduation or post graduation.

Estimate Future Cost

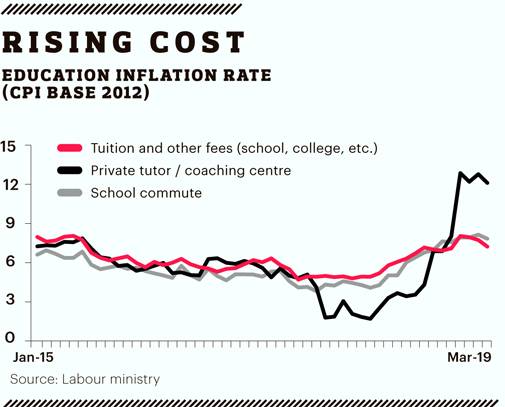

If you start early, your goal may be at least 15-20 years away, so inflation will play a major role in estimating the correct savings target for future (see: Higher Education). "Education inflation is one of the highest. Over the years, we have experienced an increase in the average loan amounts required by customers both for domestic and overseas education. This increase is on account of inflation, and in case of overseas education, both inflation and relative forex movement," says Amit Gainda, CEO, Avanse Financial Services, which specialises in education loans. The average annual inflation of school and college tuition fee between January 2015 and March 2019 was 6.22 per cent. During the same period, private tuition and coaching inflation was 5.8 per cent. It makes sense for you to plan your future expenses keeping these figures in mind.

High Fees At Government-Aided Institutions

While it is assumed that higher education at private institutions will be expensive, most government-aided professional education institutes have also raised their fees significantly of late. In some cases, it is almost on a par with what private institutions charge. The government grant model has been replaced by a loan model in which central education institutions such as IITs, NITs, AIIMS, IISc, IIMs and other colleges under UGC can take loans from the Higher Education Financing Agency (HEFA). Institutions established before 2008 have to bear the 100 per cent repayment burden. Those established between 2008 and 2014 have to bear 75 per cent of the repayment burden while the government of India pays the remaining 25 per cent. Institutions established after 2014/15 will not have to take any burden as the government will make 100 per cent repayment. Old established institutions will have to arrange their own resources if they wish to create any new asset. Due to this, most such institutions have raised fees to be self-sufficient. This means a more expensive higher education is not only a reality in case of private institutions but in government-aided institutions too.

Don't Go Overboard On Elementary Education

While you plan for your child's higher education, you should also be mindful of her elementary education. The cost of elementary education has skyrocketed of late. Many parents now take loans to manage their short-term liquidity due to this higher cost. "With rising school fees, we are seeing a trend where parents are opting for financing school education as well," says Gainda. If it happens occasionally, then there is nothing wrong in taking such loans, but you must review your situation if it becomes a regular practice. If you go beyond limits to fund elementary level studies, you face the risk of falling short of money for higher education. Therefore, it is important to strike a balance between saving for future expenses and current expenses.

Early And Small Steps

If you start saving late for future expenses, it could turn out to be costlier. You may have to double your monthly savings target if you delay by even five years (see: Higher Education). "It is always better to start early, by the time the child turns two-three. The year of graduation/higher studies is fixed at 18-21 years globally - in investment parlance, that's called time horizon. Therefore, starting early leads to a relatively longer time horizon to save and invest. A longer time period has several benefits. One, the benefit of compounding. Two, an ability to invest in relatively higher risk-return asset classes like equities," says Rajesh Cheruvu, Chief Investment Officer at WGC Wealth.

While you cannot take a call on which course your child will choose in the future, you can start by picking a profession of your choice so that it gives you a headstart in estimating the future cost. As they say, shoot for the moon, you'll land among the stars.

As your child will grow, you will start getting clarity and accordingly you can modify your target based on the new developments.

Save Big For Overseas Degree

The trend of Indian students going for higher education overseas has been rising. If you have any such plan, you should be prepared for much higher expenses. For example, an MBA at IIM-Ahmedabad at present costs about Rs 22 lakh, but an MBA from Harvard Business School costs Rs 80 lakh. "If one looks at the private institutions in India which offer education that's comparable with global standards, the cost will be somewhat lower than what the foreign institutions charge. The cost difference in these cases from the student's perspective is largely on account of the living expenses, which will be significantly higher abroad. If one compares the cost of a foreign institution (without scholarship) vis-a-vis a reputed public sector institution (which are generally subsidised), there will be significant differences in the course fee itself," says Mallick.

Start much earlier if you plan to send your child for higher studies abroad as the cost there could be many times higher than what you would need to pay in India. The best way to realise your dream is to start early, set your savings target and invest in equities. Parents with more than one child should go for separate investments for both children.

Protection Top Priority

Parents are often emotional when choosing a product for child-related goals, which makes them vulnerable to exploitation. Many of them end up buying products that don't gel with their investment requirements. Therefore, be cautious and not emotional when selecting an investment product for your child's future.

Protection should be your first priority. For that, take a holistic view and depend mainly on term insurance. "Term insurance is a must for every earning individual as it offers financial protection to their loved ones. The decision on the quantum of the cover is key as it has to take into account the prevailing family expenses, future needs like children's education, health care, mortgage commitments and other family life needs with necessary adjustments through reasonable assumption of inflation. This helps the insured ensure his family meets its aspirations even in the unfortunate event of his untimely demise, while securing the future at a nominal premium," says Cheruvu.

Model Investment Portfolio

If you start early, you should have a long horizon of 10-15 years and, therefore, equity should be a major part of your investment due to its higher growth potential. "Equity investing is a long-term solution for wealth creation, which means parents must look at an investment horizon of at least five years. So, if there are any short-term education goals, direct equities are not the right avenue. Parents looking to save for longer-term goals like secondary schooling, private tuitions or higher education, can consider direct stock market investing," says Rahul Jain, Head, Personal Wealth Advisory, Edelweiss. If you invest 70-75 per cent of your savings in equities, you may keep the rest of the investment for your child in a debt product.

Most financial experts advise buying a combination of term plan and a systemic investment plan (SIP) in an equity mutual fund. A term plan takes care of protection, while SIPs in equity mutual funds are the best way for long-term investing. "Saving money via mutual funds is one of the most convenient ways to build wealth for your child's education. Mutual funds are particularly useful for saving money towards goals of varying frequencies," says Jain.

Many insurance companies offer unit-linked investment plans (ULIPs) as an option to invest in equities for your child's future; the insurance works as a goal protection feature. Should you go for such ULIPs?

"A ULIP covers both needs under the same policy and provides tax-free returns on maturity, whereas in the case of equity mutual funds, there is long-term capital gains (LTCG) tax on profits of more than Rs 1 lakh. On the other hand, ULIPs have a lock-in period of five years. Both the options are suitable depending upon specific individual needs and situations," says Bhave of Karvy Private Wealth.

New-age ULIPs have become cost-efficient, so they could be considered for long-term investment. However, you should avoid buying endowment plans of insurance companies for this purpose because they invest predominantly in debt products and offer a return just around the inflation rate.

For the debt part of your portfolio, you may go for products that offer higher tax efficient return.

Sukanya Samriddhi Yojana (SSY) is a good debt product for a girl child. If you have a daughter, you can start investing in SSY till she turns 10. However, you should be aware that it is a long-term product which matures when your daughter turns 21. It lacks liquidity, so commit only an amount that you are sure about not needing in the near future.

You can also invest in public provident fund (PPF), which offers relatively higher post-tax returns among debt products. You will have to stay invested for a minimum period of 15 years. The maximum annual investment for both the products is Rs 1.5 lakh, while the minimum annual investment is Rs 500 in PPF and Rs 1,000 in SSY. If you have a short-term horizon, then you could go for bank fixed deposits or debt mutual funds.

Keep Education Loan As The Last Option

Taking an education loans has become easier and this is one of the reasons it has becoming a popular option for funding higher education. However, you should take this loan only to the extent that your child can handle. An education loan is a facilitator but comes with a long repayment burden. "Loan should be the last resort for parents. It will impact the wealth building process of the child as there will be an interest-paying term once the child starts working," says Jain.

If the choice is between your retirement kitty and your child's higher education, then do go for an education loan. Jeopardising your retirement savings to fund your child's education is inadvisable as it is possible that your child's income after education is big enough for her to pay off the loan early.

"Dynamics seen with regards to foreclosure of the loan vary with respect to the level of the programme (post-graduate/undergraduate), country of study, etc. While our sanction tenure is nearly 10 years, for post graduate students, our end-to-end loan tenure is nearly five-six years. On an average, a student forecloses her loan after nearly three-four years after completion of studies," says Gainda. Else, you can share some of the repayment burden to ensure the loan in taken care of as early as possible.

When your child has been selected for a course in a reputed institution with an excellent placement track record, taking an education loan may be worthwhile. Given the good reputation of the institution and the course, there will not be any dearth of funding options. You can take an education loan even from a private lender. If the right course at the right institution is chosen, repaying the education loan may not be a difficult task.

@naveenkumar80