The backbone of India's financial sector is getting its strength back.

Banks, battling low credit demand and rising bad loans, have been given a few booster shots in the last three months. One, Parliament has finally cleared the Bill that will lead to the setting up of new banks. Two, on January 29, the Reserve Bank of (RBI), lowered the rate at which it lends to banks by 25 basis points (bps). To top it all, the government's efforts over the last few months to boost growth are likely to increase the demand for credit and improve banks' asset quality.

Not surprisingly, banking sector stocks, which had been doing better than the overall market for a while now, have really

surged in the last few months.

The RBI is expected to speed up the process of issuing bank licences after the banking Bill becomes law, says Vaibhav Agrawal, Vice President, Research Banking, Angel Broking.

Another trigger for the stock rally is a proposal in the Bill to increase voting rights from one per cent to 10 per cent in the case of public sector banks and from 10 per cent to 26 per cent in the case of private banks. This has improved investor sentiment, says Saday Sinha, banking analyst, Kotak Securities.

Vinay Khattar, Head of Research, Edelweiss Financial Services, agrees. "This will benefit private sector banks such as Kotak Mahindra Bank, YES Bank and ING Vysya Bank where promoter holding is more than 10 per cent," he says.

New BanksExperts say the entry of new banks is likely to attract foreign funds into the sector. "Apart from bringing tougher competition, new banks will increase the acquisition prospects of the older private banks," says Agrawal. The prospect of acquisition is, in fact, the main reason for the recent rise in shares of these banks.

"In this space, South Indian Bank looks attractive, as it is trading at a reasonable valuation compared with other older private sector banks and has decent fundamentals," he says. "Stocks of other older banks that one can consider for gaining from a possible acquisition are Federal Bank and Karur Vysya Bank," says Agrawal. However, Rajat Rajgarhia, Director, Research, Motilal Oswal Financial Services, feels this will not happen in a hurry. It will be a time-consuming process and taking another 12 to 15 months.

Edelweiss' Khattar says the worst is over on the macroeconomic front, and with the RBI cutting interest rates, economic growth will in all likelihood pick up shortly. After keeping the repo rate unchanged since April 2012, the RBI, in its third quarter review of the monetary policy, slashed it by 25 bps to 7.75 per cent. In the last quarter review in March, it was further reduced to 7.50 per cent. So too, in the third quarter review, the cash reserve ratio, or the percentage of their funds banks have to keep with them, was lowered to four per cent. The last quarter review left it unchanged.

All this suggests the RBI has been shifting focus from controlling inflation to supporting growth. Agrawal says that in the near term, lower commodity prices are also expected to bring down inflation, opening the window for further cuts in the repo rate.

Lower interest rates are good news for banks as they aid credit growth and improve asset quality. "Over the next financial year we could see rate cuts up to 150 bps," says Khattar. As stocks, Angel's Agrawal prefers private sector banks to state owned ones, given their strong capital base, growth prospects and asset quality. Private sector banks are expected to post a strong 22.5 per cent growth in net interest income while public sector banks are expected to lag with 4.5 per cent growth.

Banks in general are expected to improve margins due to better credit offtake and reduction in term deposit rates. Their cost of funds is also likely to drop, considering that short-term borrowing rates have already begun falling. Experts say valuations of public sector banks offered a lot of bottom-fishing opportunities three to four months ago. "After the recent surge in several of these stocks, further upsides would have to be driven by catalysts such as lower pricing of high-cost deposits and higher recoveries," says Agrawal. Another important factor is Tier-I capital, considering the near-term capital raising plans of many of these banks. So, government banks with adequate Tier-I capital can also be a good investment option.

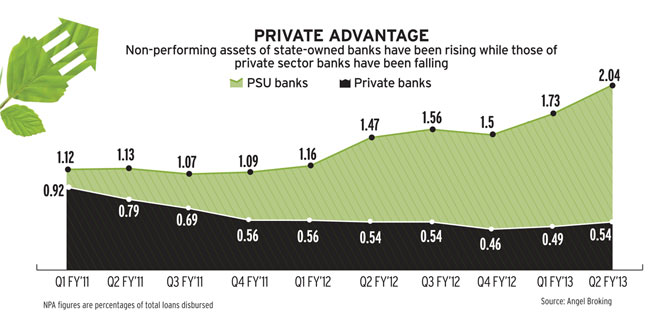

In 2011/12, the asset quality of banks was severely impaired, as seen by the steep increase in non-performing assets (NPAs), particularly of the government owned banks, owing to their significant exposure to troubled sectors such as power, aviation, real estate and telecom (see Private Advantage). According to Dun & Bradstreet, in 2011/12, net bank NPAs grew 55.6 per cent while there was a 58 per cent rise in restructured assets.

Another reason analysts prefer private sector banks is that they have better asset quality because of their lower exposure to small and medium enterprises. Plus, retail business is a big part of their portfolios. "For instance, ICICI Bank's 35 per cent book is retail, which is witnessing good asset quality, while exposure to SMEs is less than five per cent," says Sinha of Kotak.

Agrawal prefers Axis Bank, ICICI Bank and YES Bank because of their capital adequacy and branch expansion plans to gain a higher share of the loan market and increase their low-cost deposits. The loan growth for public sector banks for 2012/13 and 2013/14 is expected to be 14 to 16 per cent, and for large private sector banks in the range of 18 to 24 per cent. At the same time, private sector banks have decent asset quality and have been trading at reasonable valuations. This, despite the fact that any reduction in interest rates will increase the value of public sector banks' huge bond holdings. Bond prices invariably rise when interest rates fall. Sinha of Kotak Securities is cautious on government banks due to their poor asset quality and large restructured assets, which will require provisioning.

Among government banks, Sinha recommends Bank of Baroda and SBI, but only on correction. Although SBI's asset quality has stabilised, net interest margins have fallen from four to 3.5 per cent. "So, even though loan growth has picked up, margins are down, which will impact net interest income," he says.

Of course, nothing is entirely certain. It is possible interest rates may not fall as expected. The RBI has already warned that scope for further easing is limited. Notably, the central bank expects headline inflation to remain around the current levels in 2013 due to the recent increase in diesel prices and rising input costs for industry. However, the government's projections suggest that headline inflation may decline by around one per cent in the period. Further, despite a 175 bps cut in the CRR and the cuts in the repo rate in the last 12 months, banks have cut lending rates by only 25 to 40 bps.

Courtesy: Money Today