When it comes to buying health insurance, people like Ravi Malhotra are spoilt for choice. It isn’t the multitude of health plans that has the 42-yearold wondering what he should do, but it’s the mix of the right health plans with a minimum overlap of illnesses covered and maximum benefits that Malhotra is keen on signing for himself.

“In reality, everything boils down to your requirements and there are several ways of assessing this,” says Rahul Aggarwal, CEO, Optima Insurance Brokers. “The lower one’s income, the greater the need for a health cover, as the rich can pay for themselves,” he adds.

There are some ground rules you need to remember. It is never too late to go for health insurance and that the first policy should be the basic one offered by all general insurers. This is the typical mediclaim policy that reimburses the cost of hospitalisation and day-care surgeries. This policy needs to be renewed every year, covers all ailments needing hospitalisation and is very useful in emergencies.Health in your hands 5 points you must keep in mind when buying health insurance.

|

The premium in a diabetes plan is prohibitive, but this is more affordable in a cancer care plan. These plans are essentially oriented towards managing the insured disease.

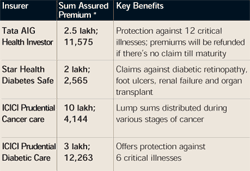

Star Health has a general insurance policy that covers the cost of hospitalisation for diabetics up to a maximum of Rs 5 lakh. Specifically, it covers diabetic retinopathy, diabetic nephropathy (chronic renal failure), diabetic foot ulcer requiring micro-vascular surgical correction. The best thing about this policy is that it covers the cost of organ transplant (both for donor and receiver) subject to the sum assured and allows a second transplant if the first is a failure. People can enter into this policy even at age 65 and can get renewals till age 70.

LIC’s Health Plus is an interesting ULIP scheme. While a portion of the sum assured is used for covering immediate risk, the rest is invested in equities. In case any listed critical illness is diagnosed, a lump sum benefit is offered. Surgery patients are provided with a daily hospitalisation cash benefit. A person can claim up to three times the sum assured in the policy’s lifetime as lump sum benefit, as well as coopt for cover with family members. In a year, one can make several claims. For other medical exigencies, including illnesses not covered under the policy, the insured can utilise the invested corpus.

|

| Click here to enlarge |

The policy, however, lapses when one makes the first claim. On death, survivors get the sum assured. Besides, there is a 5 per cent increase in critical illness benefit every year subject to a maximum of 50 per cent (like the no-claim benefit offered by general health insurers). Health Investor also offers a limited premium paying term.

What is the best way to plan for a comprehensive health cover? Over and above the basic mediclaim policy, individuals could opt for policies that have flexible payment terms. If there’s uncertainty of income, a limited premium plan is another option, but this should not come with loss of benefits. Essentially, individuals must evaluate their premium outgo against the healthcare benefits. A diabetic can check out his options under the Star Health policy, while a person with a family history of cancer can opt for a specific policy offered by ICICI Prudential; but do check out the cancers excluded from cover. “A healthy young person with no serious bad habits can opt for a policy that has limited critical illnesses covered rather than the full gamut,” says Aggarwal.

One should also check out the amount of cover. Apollo DKV Insurance Company, in its in-patient hospitalisation cover, provides coverage of up to Rs 10 lakh against the maximum cover of Rs 5 lakh offered by other insurers. But it is better to opt for two policies from different insurers—those that complement each other. But if you find premiums expensive, a standard plan with a few critical top-ups should always be your first choice.