The Securities And Exchange Board of India (SEBI) has announced the waiver of entry loads for direct mutual fund (MF) applicants. From January 4, 2008, the regulator has exempted mutual fund investors from the payment of entry fee on applications that are received through the internet, directly submitted to asset management companies (AMC), to collection centres or investor services centres and are not routed through any distributor, agent or broker. This new regulation is applicable to both new fund offers (NFOs) and existing funds.

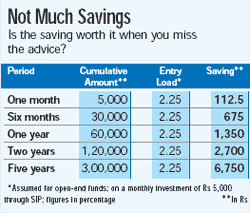

However, mutual funds will not collect any entry load from direct investors. On the face of it, SEBI’s new initiative seems to be in favour of investors, but in reality, it may not benefit the investor community as a whole. A retail investor, on average, invests about Rs 1,000 per month in a mutual fund. On that investment of Rs 1,000, he saves Rs 22.50. However, HNIs and companies who invest huge sums could save a tidy amount. Still, the new rules will not change the scenario too much as HNIs and companies were anyway squeezing distributors.

Says Sameer Kamdar, Country Head, Mata Securities: “The new regulation will slow down the growth in the mutual fund industry. If distributors do not have any incentive in an already lowcommission scenario, they will be more inclined to sell insurance products and promote ULIPs which give them good commission.”

Says Sameer Kamdar, Country Head, Mata Securities: “The new regulation will slow down the growth in the mutual fund industry. If distributors do not have any incentive in an already lowcommission scenario, they will be more inclined to sell insurance products and promote ULIPs which give them good commission.”

Commissions paid by insurance companies go as high as 50 per cent on the first year’s premium. Already, distributors and agents are selling ULIPs as mutual fund products that give investors an additional insurance cover. Experts feel that this can also go against the investor’s interest, as the whole industry will push closeended funds that have amortisation charges as high as 6 per cent.

Whether more investors turn directly to mutual funds remains to be seen. But those investors who go the direct route may have to forgo the expert and informed advice of their planners. For now, the new regulation doesn’t seem to be helping the mutual fund industry at large.

— Mahesh Nayak