After a gap of nearly six months, the neat Fixed Maturity Plan (FMP) is slowly making a comeback. This fixed income product became unfashionable after the Securities and Exchange Board of India (SEBI) banned fund houses from stating their indicative yields and portfolios before they were launched. But since August 2009, 11 new offer documents were filed with SEBI, suggesting that investors are now beginning to warm up to these products once again.

Fund houses that have filed offer documents include DWS, Fortis, HDFC, Kotak, Principal PNB and UTI Mutual Funds. Says Arjun Parthasarthy, Head of Fixed Income, IDFC Mutual Fund: “We feel that it’s the right time to launch these products as investor appetite is rising.”

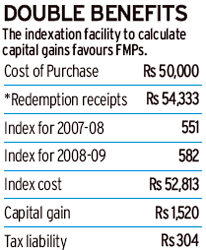

With the interest rates in the economy showing signs of firming up, fund houses have begun launching these funds to capture the higher yields. Another reason for launching these funds now is the indexation benefits that FMPs will get, particularly for schemes maturing in April 2010 or April 2011.

Indexation allows investors to get a better post-tax return. Comparative fixed income instruments like the bank fixed deposits don’t have a similar tax advantage like FMPs. As a result, the post-tax yield for an investor in the highest tax slab is merely 5.4 per cent per year on an 8 per cent bank deposit while a similar yielding 13-month FMP nets about 7.4 per cent post-tax.

Says Suresh Sadagopan, Certified Financial Planner, Ladder7 Financial Advisories: “On pre-tax basis, while FMP returns are similar to other products, its post-tax returns are far higher as compared to other debt products, making them attractive instruments for investors in higher tax brackets.”

On the other hand, the investment portfolios of FMPs are also shifting towards safer and sounder bond instruments. Gone are the days when fund managers used to invest in highyielding debt paper of non-banking financial companies and highlyleveraged debt companies. Besides, post the Lehman Brothers’ bankruptcy, fixed income instruments had come under the scanner for possible defaults and FMP products were looked at with skepticism.

But now fund houses are focussing on AAA (read triple A) or AA+ rated debt instruments that have a lower default risk. Although this reduces the final yield on the FMP product, it reduces the risk of default and thus, a loss of return to the investor. But as fund houses are barred from giving out indicative yields, investors need to comb the fund’s offer documents to assess its debt portfolio.

Also, look at the history of the fund house, how they managed FMPs earlier and whether they aggressively invested in lower rated papers to chase yields. Says Sadagopan: “Investors can look at a fund house’s risk history, and also take into account debt compositions of earlier portfolios to assess FMP risks.”

One must also remember that high-rated paper could also default due to abnormal situations. Hence, investors must do their own due diligence as post-tax yield on FMPs are too good to pass up.