When Navin Daniel set out to take a personal loan of Rs 25 lakh about seven weeks ago, the private sector bank where he usually banked his salary seemed eager to take up his business. Soon after Daniel filed the application, his bankers assured him they would release his loan “within a few days”. But about two weeks into the deal, his bankers called up and said they could provide only Rs 8 lakh, which would again take a few days more.

After two more weeks, his bankers brought down the amount to Rs 4 lakh. Three more weeks later, Daniel is still awaiting his personal loan. When Daniel contacted his bank lately, they turned around and refused a loan. Now, the marketing professional is tapping his friends to tide over his shortterm funding requirements. Says Daniel: “If banks have a complete loan department to look into these issues beforehand, then they should have come back a lot earlier than just make blank promises.”

Loan Control |

|---|

| Banks and NBFCs are reluctant to give personal loans even to good-quality customers. |

| If you must borrow, pledging assets is the only option in these times. |

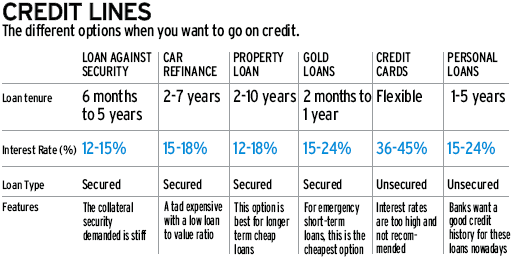

| For short-term needs, loan against gold is the cheapest option - credit card is the most expensive. |

| For long-term needs, consider loan against property or car. Property loans are the cheapest to get. |

With banks seeing high levels of default in personal loans, such rejections are becoming all too common. Banks and non-banking financial companies (NBFCs) have stopped disbursing personal loans, or unsecured loans, to good-quality customers. It’s a sign of the times. The credit squeeze has put lenders in a spot of bother as it’s getting difficult to raise resources in these uncertain times. As a result, they have cut back their lending. Says Apul Nayyar, CEO, Moneyline Credit: “People began to borrow heavily and were getting overleveraged. And to top it, credit began to tighten.” The distress is visible across the lending industry as growth in credit offtake has slipped from 25 per cent last year to around 15 per cent currently.

So, what’s the alternative? If you are looking at borrowing now, you need to pledge some collateral or assets to the bank. Gone are the days of easy credit when borrowers could easily sign up a loan against personal credit history or against salaries. Lenders are increasingly asking for various assets like bank deposits, shares, mutual fund units, government securities like National Savings Certificates, gold and real estate to lend against. Alternatively, credit cards can come to your quick rescue if you need emergency cash, but use this type of borrowing sparingly. That’s because the interest rates on credit cards is a stiff 42 per cent.

Collateral Limit

As a borrower, the decision to take a loan against assets is not one that you should take lightly. Once you pledge an asset, the bank then has a lien on your asset, which means that the bank holds it until you pay off the loan. Says Harsh Roongta, CEO, Apnapaisa.com: “You will need to have an asset in the first place, and then want to pledge it. Therefore, look at the entire options of how quickly you need a loan and for what purpose.”

Short Squeeze |

|---|

| How you can lose when you pledge shares |

| Value of X shares on day of pledging : Rs 1,00,000 |

| Loan against the value of shares : 50% |

| Total loan value you will receive : Rs 50,000 |

| If the market value of shares falls by : 40% |

| The current market value of shares : Rs 60,000 |

| Additional collateral required : Rs 40,000 |

Besides, a loan stays with you for some time and you have to make provisions in your budget to repay these loans. Such actions tend to put your savings plan or retirement investing on the back burner as repaying the loan takes centrestage. That apart, a loan is an expensive affair and it costs more than the returns in, say, a fixed deposit. Take, for example, a fixed deposit that pays you an interest of 10 per cent per annum. When you put up the same as collateral with your bank, you are charged a 3-4 per cent higher interest than your deposit. This way the bank earns it spreads, but it costs you a tidy sum over time. Instead, if you are planning a long-term loan, it sometimes makes better sense to break your fixed deposit at a marginal cost and use the proceeds for your needs.

For many individuals, especially those interested in investing in the stock market, pledging a share for margin funding is no different from taking a loan. Such funding is more common in a booming market as investors pledge shares and re-invest the proceeds in the stock market. But such a move has its own pitfalls. Consider the recent debacle of Great Offshore. Its promoter Vijay Sheth pledged most of his stake in Great Offshore as he borrowed heavily to buy a 15 per cent stake from the Sheths. As the stock market tumbled late last year, Great Offshore’s pledged equity dipped in value, triggering margin calls. Vijay Sheth had to raise a further Rs 240 crore by pledging 5.53 million shares to Bharati Shipyard.

By far the most common threat that such borrowers face is the risk of margin calls getting triggered. If you pledged your shares to the limit and do not have any further collateral in either cash or shares to give your lender, you are most likely to face this situation when your shares tank. Says Nayyar: “As per the margin requirements, borrowers have to put up additional collateral in two to three days in case the asset value of the security falls down.”

Therefore, investors have to be aware of the risk because stock prices are marked to market every trading day. The loan agreements have a depreciation of security clause, which states that borrowers have to make good the loss when the asset price depreciates.

Consider this: a bank typically lends around 50 per cent against a blue chip A group company. If the stock price dips after you have pledged the share, then you have to make good the difference in the bank’s margins (see table: Short Squeeze) within two or three working days. If you don’t comply, the bank may sell a part of your holdings and adjust its margin exposure. If the situation gets worse and the stock price tumbles even further, then the bank may tend to take the hard step and offload your entire holding. It means you will lose your collateral.

Leveraging against shares is a double-edged sword. Investors tend to make money faster if the trend is with you, and lose it equally faster if the trend is against. But more often than not, investors tend to find themselves on the wrong side of the fence. Says Amar Pandit, CEO, My Financial Advisor: “Usually, investors borrow against shares at the peak of the bull market to reinvest in the market, and that’s a sure recipe for disaster.” If the stock prices fall drastically, investors could lose their collateral.

But if investors still have to borrow against shares, then it’s better to keep additional collateral with your banker either in the form of shares or through a lower loan amount. For example, borrow 40 per cent as against the 50 per cent a bank is offering. Still more preferable is to borrow when the chips are down. Says Pandit: “You could borrow to reinvest when the markets were at 8,000. Of course, it could go lower, but you have a margin of safety as the downside potential is that much lower.”

Other Backups

Away from stocks, an asset that moves less drastically is a house as there’s no daily price swing here. House prices move in tandem with the economy and it takes a long time for the property prices to change. Says Roongta: “It takes about three weeks for a loan against a house to get sanctioned as the lender checks the title clearance. This form of loan comes with a low interest rate.” Since this is one of your biggest assets, it’s better to avoid putting up such collateral unless it’s an extreme emergency or you require a slightly flexible and longer repayment period.

For smaller requirements, it’s better to put up gold for your needs. NBFCs and banks are quick to offer a gold loan. Says V.P. Nandakumar, Chairman & CEO, Manappuram Group of Companies: “Gold can be quickly pledged for short-term financing as we lend up to 85 per cent of the scrap value and usually the loan is for two to three months.” Although this form of loan is the quickest, the interest rate is usually higher than a pledge against property. NBFCs are usually quick to provide loans against gold, while banks could take a few days to disburse your loan.

In the end, make sure you have a cushion to tide over any crisis that may occur during your borrowing days. If you need it, always borrow less than the collateral you put up so that you are always one up in tough times. This, coupled with a lower borrowing, will help keep your repayments low, interest costs low and also reduce the risk considerably. That’s a whole lot better than losing your assets.