After banning algorithmic (algo) trading in micro- and mini-contracts in commodities with effect from January 1, the commodities market regulator, the Forward Markets Commission (FMC), has issued guidelines for regulation

of algorithmic trading in the commodity futures market.

Algorithmic trading refers to trade orders generated using automated execution logic through a computer application.

According to the guidelines, which will be effective from April 1, stock exchanges will have to ensure that immediate or cancel orders are not placed through the algo trade route.

To promote fair use of

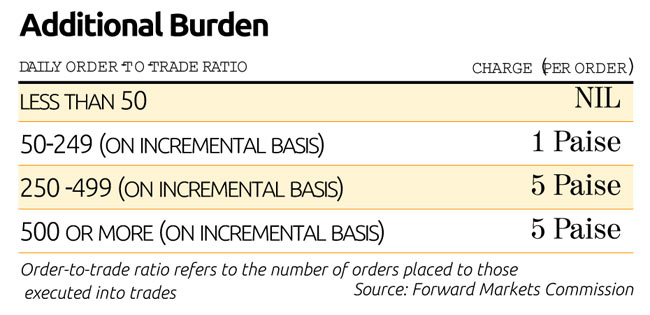

the trading platform , there will be some economic disincentives for algorithmic trades based on the order-to-trade ratio. Only a portion of orders placed through trading terminals are executed due to non-fulfilment of certain conditions or cancellation by clients. Based on the daily order-totrade ratio of the client, an additional charge ranging from 1-5 paise will be levied on all algorithmic orders.

From the next financial year, commodity exchanges will be able to process 20 orders per second from a user, irrespective of the order size. In case the order-totrade ratio of a member reaches 500 during a trading day, the member will not be allowed to place any order for the first 15 minutes on the next trading day.

The FMC has asked commodities exchanges to submit a monthly report on algorithmic trading, including its percentage in total trade and the number of members of using algorithmic trading. Members already using algorithmic trading will need their exchange's approval by March 31.