The buzz on the street is not caused by market experts alone talking about signs of revival in the economy. It’s also created by all of us—consumers, investors, employees and employers. So what do these segments have to say about the economic climate in general, and how does it affect them in particular? We take a look at the results of recent studies and surveys, and find that, by and large, optimism is contagious.

Corporates

According to the latest McKinsey global survey on economic conditions, the majority of executives believe that the economy is battered, but resilient. It’s common knowledge that a majority of companies across the world have deployed a slew of measures to ride out the recession, be it reducing operating costs, restructuring or exiting certain markets. But nearly half the respondents, representing all regions, industries, functional specialties and levels of seniority, said that doing so has only been partially effective.

The big exception is the consensus on hiring. Though far fewer companies have hired talent that would not otherwise have been available, the majority of those that did, deem it a very effective move. According to the survey, a significant chunk of many companies’ lower operating costs came from workforce reductions, but a notable 41% of respondents claimed that their companies haven’t had any job cuts since last September. Clearly, pink slip paranoia is on its way out.

More interestingly, the top three fire-fighting responses identified by the respondents include changing the mix of their products to reach new customers, snatching market share from weakened competitors, reconfiguring their organisations to meet future needs and building cash reserves. Regardless of the future that the firms are looking at, introducing new products or services emerged as top priority. This suggests the crisis may be spurring innovation.

Consumers

The optimism is spilling over to buyers too. According to the quarterly Nielsen Consumer Confidence survey, Indians are the second most optimistic citizens in the world (after Indonesians). The survey, which covered 14,029 consumers in Europe, North America and Asia, observed their confidence levels and economic outlook.

After slipping from 114 in September 2008 to 99 in March 2009, India’s consumer confidence index rose to 112 in June. This is the highest gain reported by any country, and the sharp improvement should be seen in light of the perceived improvement in the job market. In March, 41% of Indian respondents had said that job prospects over the next 12 months looked good, while 6% had said that the prospects were excellent. In June, 55% said that the prospects were good and 13% opted for excellent. This means that 68% were bullish on employment in June, up from 47% in March.

When it comes to spending, Indians are more likely to save spare cash after covering essential living expenses, paying loans, spending on clothes, new technology and home improvement, and investing in the stock markets and retirement funds. Conservative consumers are unlikely to blow up the money on holidays or out-of-home entertainment.

Investors

What market experts say has a direct impact on investors. According to the newly established JP Morgan Investor Confidence Index, retail investors are more confident than corporate investors and financial advisers about economic recovery and its impact on the markets. According to the July index, on a scale of 200, retail investor confidence stood at 138.3. The score of advisers is 136 and that of corporate investors, the least confident, 133.5. The aggregate investor confidence index stands at 135.9.

The survey covered 1,711 retail investors with liquid assets in excess of Rs 2 lakh across Delhi, Mumbai, Kolkata, Ahmedabad, Pune, Bengaluru, Hyderabad and Chennai. It also polled independent financial advisers, corporate treasuries, banks and distributors. However, the survey does not reflect the deficient monsoon and the swine flu panic, which could have an effect on the sentiment.

The fallout of quick income programmes

- R. Sree Ram

Fund-starved Indian companies have fallen upon cheap and easy credit and are ready to try any avenue to raise money quickly. Amused market commentators have called these the new QIPs—quick income programmes—an obvious reference to the qualified institutional placement (QIP) route that several companies are taking to raise money in a hurry. Close to 70 companies have passed enabling resolutions to raise around Rs 60,000 crore through various routes like American / European Depository receipts, QIPs or Foreign Currency Convertible Bonds (FCCBs).

Real estate and construction firms head the list of companies that want fast cash. Unitech, Hindustan Construction Company, Indiabulls Real Estate and Sobha Developers have raised Rs 9,762 crore so far this year. The new funds are helping these companies improve liquidity by retiring excess debt and routing more money into productive activities like building capacities.

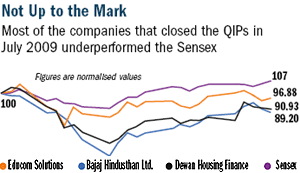

Most of the companies that have obtained shareholder approval to raise funds are planning to go the QIP way, which involves issuance of securities or shares to qualified investors. The biggest beneficiary of a QIP would be the company itself, as it gets to raise the much required money. On the flip side, it results in an expansion of the capital base and the earnings per share will be diluted. If the funds raised do not help the company improve its profits, it can actually result in an erosion of investor wealth. In fact, according to a study conducted by rating agency Crisil, 75% of the QIPs issued till 10 July 2009 have returned negative value as the share prices have fallen below the issue prices. “The significant rise in stock prices before the 2009-10 Union budget made QIP deals unattractive as the inherent fundamentals of most companies that queued up for QIPs have not changed materially,” says Chetan Majithia, head, Crisil Equities.

If the funds are raised by the issuance of convertible debentures, it can have long-term implications. This is because these are issued with a pre-determined conversion price, one at which the investor has the option to convert the debentures into equity shares in the future. However, the company could be in trouble if the price is lower than the set price at the time of conversion. Investors would not convert the debentures into equity at low prices and opt for cash instead.

Take Wockhardt. In 2004, the firm had issued FCCBs, which could be converted at a price of Rs 486 per share in October 2009. The current market price of a Wockhardt share is around Rs 150, so the firm has had to sell noncore businesses and restructure its debt to stay afloat. As the debt piled up to Rs 3,400 crore, the company posted a net loss of Rs 189 crore in April-June quarter. Investors ended up being the biggest losers as the share price of Wockhardt crashed from Rs 430 in January 2008 to Rs 80 in April this year. This is the biggest drawback of most corporate quick-cash schemes—the small investor ends up taking the beating.

Clunkers for cash may not be a steal

- Rakesh Rai

A Chennai-based builder seems to have taken inspiration from US President Obama’s ‘Cash for Clunkers’ plan. He is offering an exchange scheme: old homes for new. Unlike Obama’s scheme, in this offer, the clunkers (old houses) may turn out to be more expensive and of better value than the equivalent of cash (new homes).

So what’s this all about? L&T Arun Excello Realty, a joint venture between an L&T subsidiary and a Chennai-based real estate group, has offered an apartment exchange scheme exclusively to senior citizens, for whom the ground and first floors of an integrated township have been reserved. The project, Estancia, is coming up 18 km from the Chennai airport on the Madurai route, while most senior citizens who eventually trade their ‘old’ homes for new ones will most likely be staying within city limits, often in upmarket residential localities.

To make sure that potential buyers get their money’s worth, the builder has engaged realty consultant Jones Lang LaSalle Meghraj (JLLM) to ‘guide’ elderly customers through the nitty-gritty of the transaction, including evaluating the worth of their old apartments. Detailing the concept, P. Suresh, managing director, L&T Arun Excello Realty, says, “Senior citizens often feel out of place in the din of city life. They would have put up with hardships for decades for the sake of their children’s education. In retired life, instead of living alone, feeling insecure and coping with daily challenges in managing the household, we invite them to our gated community that provides a secure environment. They will not be neglected or left alone, but will form part of a community, including children. We are even offering to organise the housekeeping.” What he doesn’t say is that the elderly residents will be paying for these services like any other resident in the society.

On the positive side, though, the project will have elderly-friendly features like anti-skid flooring, ramps, stretcher lifts and grab bars in toilets. Thirty apartments have been reserved for senior citizens in the first three residential towers, which are expected to be ready for occupation by the year-end. The prices start from Rs 75 lakh per apartment.

So, why is this offer open only to senior citizens? Though the builders do not rule out the possibility of extending the exchange offer to other customers, Suresh says, “Since senior citizens are not eligible for home loans to buy their dream house, they often have to liquidate other assets. Hence, we came up with the idea of buying their old flats.” What will the builders do with the old apartments? “We will refurbish and sell them. If people want to sell their flats directly to end-customers, JLLM will guide them through the process. If people own independent plots or houses, we have a joint venture development plan,” he adds.

It sounds philanthropic but does the seller of an old home really benefit? That depends on where the ‘old’ house is situated. If the house has land value, one always has the option of exploring the open market for better prices or signing a joint redevelopment deal with a builder if the size of the plot is big enough. In any case, you should do your homework well in terms of research and get a clear sense of the price of your house in the open market.

Better Blu-ray quality for less?

- Brinda Vasudevan

The media format war seems to have been won, with Toshiba announcing plans to enter into an alliance with a Blu-ray player soon. A little history is in order to understand why this matters. Early this century, companies were looking for the next big optical storage medium to replace the DVD. There were two major camps—Blu-ray and HDDVD. For long, Sony was seen as the biggest (and possibly only) player in the Blu-ray camp as it was responsible for much of the development. However, the format is really the result of an association of several heavyweights, including Sony, Dell, JVC, Hitachi, HP, Panasonic, TDK, LG and Thomson.

The HD-DVD camp, meanwhile, seemed to have little room for other players, as it was dominated by Microsoft, Intel and Toshiba. But Blu-ray had its strategy in place and managed to get film producers/distributors to adopt it. And when Sony’s Play-Station 3 came out with Blu-ray, it seemed to be the killer stroke.

So what does this mean to us as consumers? More players means more competition, and more competition inevitably means lower prices. So, a Blu-ray movie disk, which now costs upwards of Rs 1,200, could become as affordable as a regular DVD. The best news for consumers is the rumour that Microsoft might join the Blu-ray bandwagon. If that happens (a slim possibility right now), Blu-ray writers, which now cost around Rs 30,000, might be had for a fraction of the price.

Regulator Watch

A look at the recent rulings which can affect you.

MARKETS

BANKING

INSURANCE

TELECOM

Banks may push ASBA now

- Rakesh Rai

It was a good idea launched at the wrong time. What’s not to like about an arrangement where an investor’s funds will leave his bank account only on allocation of shares in public issues? But when the Securities and Exchange Board of India (Sebi) introduced the Application Supported by Blocked Amount (ASBA) facility last year, most retail investors were avoiding D-street.

With market activity picking up gradually, more and more investors are now availing of the facility. Around 1.5 lakh retail investors applied via this facility in the recent NHPC IPO. This surge in interest comes soon after Sebi’s clarification that companies will have to pay a commission to banks, along with the broker, for facilitating this process. “One of the reasons for the poor response is the lack of incentive for banks to do the assigned task of accepting ASBAs,” according to Sebi’s circular. Applicants just need to submit the ASBA form, physically or electronically, at their banks. The banks then block the due amount till the allotment or till the application is rejected.

A new dawn or a zero sum game?

- Babar Zaidi

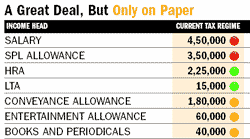

It proposes to tax all allowances and perks, remove tax incentives, even levy a tax on your retiral benefits. Yet, the new tax code proposed by the government is likely to help taxpayers. This is because it has simplified the tax rules to a great extent and made them comprehensible for the common man.

Though the rules governing the proposals are yet to be framed, it is clear that under the new code most allowances would become taxable. For some of these perks, such as conveyance, books and periodicals, entertainment, etc, employers were already paying the fringe benefit tax (FBT) and passing on the liability to the employee. But the FBT rate was lower at 7-18% of the value of the perk. Now, the full value of the perk would be included in the gross taxable income of the individual.

Even though several exemptions would be removed, the new tax code will not push up the tax outgo of the average assessee. In fact, the raising of the slabs neutralises the impact of the tax on perks (see table).

Of course, the bigger benefit is the simplification of the tax rules, which means even the average taxpayer can understand the statute without help from a chartered accountant. The new regime would make it easier to compute your tax liability. No more looking at the calendar for LTA exemption. No more confusion between short- and long-term capital gains when you sell your equity holdings and mutual funds. Everything will be included and taxed at the same rate. Maybe this is the Saral II that Finance Minister Pranab Mukherjee referred to in his budget speech.

The only sour note is the proposal to shift retiral benefits such as the Provident Fund and the Public Provident Fund from exempt-exempt-exempt to exempt-exempt-tax (EET). This could be harsh on retirees and should ideally be accompanied with a hike in the basic exemption limit for senior citizens to at least Rs 5 lakh. In this case, a monthly income of Rs 40,000 would not attract any tax.

Also, some of the changes will upset the applecarts of many taxpayers. Till now, life insurance policies were considered a tax-free haven. Under the new regime, if the premium exceeds 5% of the sum assured, any income from the policy will be taxed. This pretty much covers the entire range of Ulips, moneyback plans and endowment policies. Only pure insurance policies (or term plans) are eligible for tax exemption, but these don’t have an investment component.

This change would be a big blow to investors in Ulips as the tax exemption was a major reason for their investment. “The government has not just moved the goal posts, it has changed the very rules of the game,” says Vikas Vasal, executive director, KPMG. This could take the sheen out of Ulips and make them look like high-cost mutual funds. Is there a silver lining? Sure. Investors will stop looking at insurance as an investment and treat it as the risk cover that it is.

In some ways, the new tax code is guided by the Vijay Kelkar Committee on Direct Taxes. In 2003, the panel had suggested abolishing all tax exemptions, taxing income from insurance policies, removing the distinction between short- and long-term capital gains and shifting to EET. However, pressure from political lobbies had forced the government to water down the proposals. Let’s hope that this time around, the new code meets no road-blocks.

Revamping the ATM machines

Very soon you will be able to pay your income tax at an ATM. While Corporation Bank takes the lead in introducing this initiative for its 4 million debit card holders, other banks may follow suit. Here’s a step-by-step guide:

Incidentally, Braille and voice-aided ATMs will also soon be in place. Responding to the RBI’s directive that one-third of bank offsite ATMs should be suited for differently-abled people, ATM manufacturers NCR Corporation and Diebold Systems, recently unveiled voice-aided machines with a Braille keyboard. Currently, only 2% of the 40,000 ATMs in India are voice-aided.