On July 16, public sector behemoth Life Insurance Corporation of India (LIC) decided to acquire 51 per cent stake in debt-ridden government-owned IDBI Bank. It's likely to be a preferential share purchase to recapitalise and strengthen the bank. The expansion of the equity base will see the current majority (85.96 per cent) stakeholder - the Central government - reduce its stake, a possibility hinted at by Arun Jaitley in his capacity as Union finance minister a year ago.

The Opposition parties and bank trade unions accuse the government of arm-twisting LIC to bail out a troubled bank using insurance policy holders' money, but the government and the public sector entities involved are going ahead with their decision. The proposal has the backing of the Insurance Regulatory and Development Authority of India (IRDA) and has received in principle approval of the Reserve Bank of India (RBI). It will soon be vetted by the Securities and Exchange Board of India (SEBI) and the Reserve Bank of India (RBI). LIC, which already owns about 10 per cent stake in IDBI, will remain a financial investor and look to exit once IDBI valuations improve after the turnaround plan succeeds. If everything goes by the script, the government will also see the value of its residual 50 per cent stake improve substantially in the coming days.

The unfurling of the IDBI-LIC deal is the latest display of the Narendra Modi government's public asset management and disinvestment strategy, something that has been influencing the operational, financial and managerial fortunes of dozens of Central Public Sector Enterprises (CPSEs) over the past four years, while allowing the government to meet or exceed its annual disinvestment target. It encompasses the revival of sick companies and maximisation of the value of public assets in multiple ways to achieve larger social objectives.

The IDBI proposal, in isolation, may not give the true picture as the government's attempt to recapitalise and strengthen ailing public sector banks through a Rs 2.11 lakh crore restructuring package since 2017 is yet to resolve the non-performing asset (NPA) problems. But the underlying strategy behind the IDBI-LIC deal seems to have worked well for CPSEs in other sectors. In fact, the clarity with which the government is playing the "investor" and "mentor" role in CPSEs will have a bearing on the restructuring and business plans of several entities, including Air India, one of the biggest loss-making CPSE that failed to attract private bidders in an open stake sale plan attempted recently.

The government's attempt to make maximum use of its public sector enterprises does not end here. The decision to authorise National Highways Authority of India (NHAI) to monetise public-funded National Highway (NH) projects that are operational and generating toll revenues for at least two years, through the Toll Operate Transfer (TOT) model, is one way of meeting fund requirements for future development and operations of highways in the country. Another common practice is to ask CPSEs to take up key social sector initiatives through their CSR activities. "Meeting national priorities means net outgo for PSEs. A significant portion of our CSR contribution was in areas of skill development, sanitation, drinking water, health, rural development, etc.," says U.D. Choubey, Director General of the Standing Conference of Public Enterprises (SCOPE). According to the Department of Public Enterprises, 30 per cent to the total CSR spend in India in the last three years - Rs 9,815 crore - came from CPSEs. Public sector enterprises also played a key role in driving several flagship government schemes and played a vital role in providing LPG connections to over 3.56 crore households, distribution of 29.27 crore LED bulbs, construction of 1.39 lakh toilets and electrification of 16,686 villages - all in the last three years.

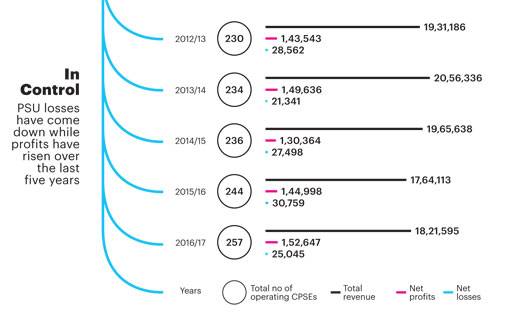

The public asset management plan of Modi government thus assigns a much bigger role for CPSEs in the overall development plan.

Midhani Model

The Modi government kicked off its public asset management plan for 2018/19 on April 4, by diluting 25 per cent stake in Mishra Dhatu Nigam (Midhani), iron and steel products company, for Rs 434.14 crore through an initial public offer (IPO).

The IPO of Midhani, which caters to sectors like defence, space and power, was a low key affair - it got listed at Rs 87 a share, 3 per cent lower than the issue price on Indian stock exchanges. LIC was a saviour here, too. It picked up 8.73 per cent stake and the public issue was oversubscribed 1.23 times.

On July 16, the day LIC decided to pick up majority stake in IDBI, its Midhani investment was still an attractive proposition as the company's share closed at Rs 141.6, way above the listing price. The value of the government shares was higher post-IPO.

Rajiv Kumar, Vice Chairman of government think-tank Niti Aayog, says that stake dilution is a win-win strategy for the government as it is just not about disinvestment proceeds but about value creation. "The government is not losing anything. It wants to dilute a bit and once the market capitalisation improves, it retains the same asset value. The government has been thinking about unlocking value in good-performing PSEs. So, if there is a profitable PSE, the government can work towards raising its market cap and after it improves, the government can disinvest. It is all about improving the asset value and in the process get more money," says Kumar.

Track Record

The government collected over `1 lakh crore as disinvestment proceeds in 2017/18 on the back of a series of public asset management interventions. The 36 disinvestment decisions executed last year were a mix of IPOs and follow on IPOs supported by government financial institutions, share buyback by cash-rich companies, strategic sale and disinvestment through exchanged traded funds.

Ever since the first public sector disinvestment plan was rolled out in 1991/92, successive Central governments have rarely managed to achieve the annual targets. The first three occasions when collections exceeded targets, the target was set at Rs 5,000 crore or below. The fourth occasion was in 2003/04, when the government managed to get Rs 15,547 crore against a target of Rs 14,500 crore. With the sale of minority shareholding in CPSEs, including IPCL, GAIL and ONGC. It took almost a decade and a half for the fifth one (in 2017/18) to happen and it was again driven by public sector units and financial institutions.

The public asset management path followed by the Modi government, in short, was not just about disinvestment like its predecessors. There has been a clear plan, with a refined approach and execution, that other governments did not have. Even though the Air India sale came a cropper, the listing of the 11 CPSEs (Midhani was one) approved by the Union Cabinet in April 2017 is in full swing. A Draft Red Herring Prospectus has been filed for RITES Ltd, IRCON International Ltd. and Rail Vikas Nigam Ltd. Due diligence is in progress for IRCTC. Others will follow. In addition, the finance ministry's Department of Investment and Public Asset Management (DIPAM) is readying a draft institutional framework for asset monetisation of CPSEs.

Neeraj Kumar Gupta, former secretary at DIPAM, says that critics have never gone beyond the "disinvestment" prism to look at the government's public resource management plan. "If you are the promoter of a company, what will be your primary objective? Disinvestment? Or maximising the value of the company? When the government formed DIPAM in 2016, this was the philosophy behind it," he said. Gupta said that sectoral departments and ministries controlling CPSEs had sectoral view points, but not necessarily that of an investor. "In May 2016, we came out with a capital restructuring policy on how capital should be serviced. It talks about everything an investor expects from a company from his investment within the framework of national priority and policy. The message to the companies were clear. You should be doing more and more business, because we have asked you to work in that particular sphere for the purpose of nation building. So, you should be making best use of whatever access to resources you have."

While this is the guiding principle for CPSEs, the objective of the investor (read government) is also clear. "Whether the government is the majority investor or not, every investor should have the best return on investment. Which means dividend and if you have surplus cash you should go for buy-back. The 2016 policy laid down all these expectations. Ultimately, doing this also adds value to your market cap. The CPSEs are the only companies which are paying more than 100 per cent of PAT as dividend," says Gupta.

It is clear that the government policy is to encourage companies to enter the market, raise money, expand their business and reduce their dependence on budgetary support. In the process, the government generates some money through stake dilution, reduces the need to provide budgetary support and finds extra resources to fund social sector schemes. The case of Cochin Shipyard, which raised `700 crore for its expansion through public listing, perhaps illustrates this point.

Financial Jugglery?

The multi-pronged strategy of disinvestment has seen a decline in Central government stake in several CPSEs. But what has been the actual decline in the government - direct and indirect - stake in these companies? "Disinvestment is a typical paradoxical story. The logic given is that it will change the culture of the public sector. Around 39 per cent is the total stake dilution that has been carried out so far by the government of India. But if you see it is all to the government entities. Only a little bit has been given in the secondary market. Of this, only Rs 1,000 crore or so has gone into the hands of private equity holders," says SCOPE's Choubey.

The biggest of all such deals was the ONGC takeover of HPCL last year. The deal was done a day before the Union Budget for 2018/19 was presented, thereby moving Rs 36,915 crore into the government kitty as disinvestment proceeds. Choubey calls it great financial managment. "HPCL remains HPCL, ONGC remains ONGC and the government has got Rs 36,000 crore. It is a unique financial proposition. Government is not losing, it is gaining. Companies are not losing, it is status quo," he says.

Was it just money moving from one government hand to another or did it have its own business rationale? "Don't think these are government companies. Global top five oil companies are vertically integrated because there are margins at every stage. In India also, the two biggest private sector players always had the dream of vertical integration. They are doing it in the best possible manner. Look at the merger from this point of view," says former DIPAM secretary Gupta. He also points out that the deal was perfectly aligned with the government policy on mergers and acquisitions announced in 2016 itself. Vivek Jain, Associate Director, India Ratings and Research, is also of the opinion that ONGC-HPCL can make business sense beyond the immediate gain to the government in terms of disinvestment proceeds. "The logical thinking has been to merge the petrochemicals and refining in one part and keep the exploration and production (E&P) in the other part," Jain says. According to him, HPCL will thus be stronger in terms of refining even as ONGC will be able to leverage the strength of the combined balance sheet while bidding for higher assets.

So, even if the government stake moves to another CPSE, there is a limit to the revenue that can be generated. The total valuation of CPSEs is around Rs 12 lakh crore. And that is the maximum the government can divest. Disinvestment then can't be a long-term solution to manage public assets. It can also have an impact on the contribution of CPSEs to the public exchequer by way of dividend payment, interest on government loans and payment of taxes and duties. There is also an increasing effort to put PSE stake in public hands, with the retail investor and employees. Between 2006-14, some Rs 900 crore worth of PSE shares went to the public - the figure was Rs 100 crore till 2006. This trend should gather strength.

Former DIPAM Secretary Gupta says that the government strategy will be to strengthen and expand the role PSEs play. "To that extent, there will be more leveraging of public assets, public investment in infrastructure, more extra budgetary role," he says. The 50 PSEs listed on the stock exchanges command almost 14 per cent of the total market capitalisation. If this is an indication of the confidence investors have in public sector assets, there is a lot of money to be made from future PSE listings.

The Future

Ashwini Mahajan, National Co-convenor of Swadeshi Jagaran Manch (SJM), an affiliate organisation of ruling Bharatiya Janata Party's ideological mentor Rashtriya Swayamsevak Sangh, says that the government is on the right path as it involves more public sector entities in managing or strengthening the assets of other CPSEs.

"We have been saying for long that there is no relationship between the efficiency (of a company) and its ownership. The public sector could be efficient, private sector could be inefficient. It could be the other way, too. Even if the private sector is efficient from its management point of view, it may not be efficient from the societal view," says Mahajan. He cites the example of Air India. "Most of its debts are on account of mishandling. That happened because the political class was in a hurry to get things done. Instead of selling Air India, you should try to utilise the assets it has. Its value should be discovered. Even if you want to sell it, you can then explore the IPO option," he adds.

Anant Geete, Union Minister for Heavy Industries and Public Enterprises, echoes the same feeling when he says that even the loss-making CPSEs are not considered for abrupt disinvestment. "We are looking at various options to make sick PSUs that we wish to disinvest more attractive to potential suitors. Infusing fresh funds into them from the government coffers is being deliberated upon. Further, we are not selling the surplus land available with sick PSUs in the country, but we are yet to take a decision on whether we want to utilise this land for low-cost housing under Pradhan Mantri Awas Yojana," he says.

On April 9, Prime Minister Modi set five challenges before India's CPSEs in the presence of the heads of all public sector enterprises at Vigyan Bhawan in New Delhi. He wanted PSEs to come up with a development road map in 100 days with a 2022 deadline. The challenges were the following: How will Indian PSUs maximise their geo-strategic reach, minimise the country's import bill, integrate innovation and research, optimally utilise their CSR funds, and, finally, what new development model will Indian PSUs give the country? The Department of Public Enterprises, given the task of preparing the road map in 100 days, is working overtime.

The government's public asset management plan seems to be clear. The PSEs should be profitable and it should be vehicles of social benefit, too.

@joecmathew