Among city gas distributors, IGL and MGL are likely to report marginal sequential declines, while Gujarat Gas could see a sharper 11 per cent drop in Q2 Ebitda.

Among city gas distributors, IGL and MGL are likely to report marginal sequential declines, while Gujarat Gas could see a sharper 11 per cent drop in Q2 Ebitda. Among city gas distributors, IGL and MGL are likely to report marginal sequential declines, while Gujarat Gas could see a sharper 11 per cent drop in Q2 Ebitda.

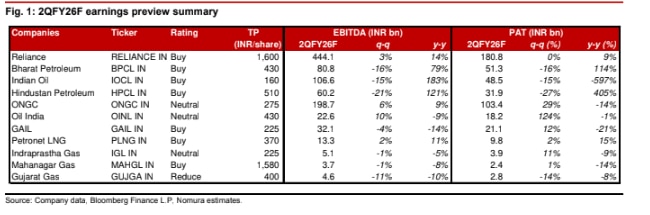

Among city gas distributors, IGL and MGL are likely to report marginal sequential declines, while Gujarat Gas could see a sharper 11 per cent drop in Q2 Ebitda.Nomura expects a mixed earnings season for India’s oil and gas sector in Q2FY26, with oil marketing companies (OMCs) likely facing a sharp sequential decline in profitability due to weaker marketing margins, while upstream producers may benefit from firmer crude realisations and currency gains. Gas utilities are expected to post muted results amid higher input costs and rupee depreciation. Reliance Industries (RIL), meanwhile, is seen delivering stable performance, supported by its telecom and oil-to-chemicals (O2C) businesses, even as softer trends in retail and upstream may offset some gains.

Nomura maintained its 'Buy' on RIL, HPCL, BPCL, IOCL, GAIL, Petronet LNG, and MGL; 'Neutral' on ONGC, OIL India, and IGL; and 'Reduce' on Gujarat Gas.

RIL

Nomura estimated RIL’s consolidated Ebitda at Rs 44,400 crore for Q2FY26, up 3 per cent quarter-on-quarter, as sustained strength in Jio and O2C is offset by muted retail and upstream performance. O2C Ebitda is pegged at Rs 15,020 crore, up 4 per cent QoQ, driven by higher refining margins and throughput, with GRMs estimated at $10.1 per barrel against $10 in Q1FY26. Upstream Ebitda is expected to remain flat at Rs 5,000 crore, as lower volumes are offset by favorable currency movements.

Jio’s Ebitda is estimated at Rs 17,230 crore, up 3 per cent QoQ, aided by 6 lakh net subscriber additions to 50.4 crore and higher ARPU of Rs 212 against Rs 209 in Q1. Retail growth is expected to remain soft, with revenues at Rs 84,600 crore (up 11 per cent YoY) and Ebitda at Rs 6,400 crore (up 13 per cent YoY), pushing margins to 7.6 per cent.

HPCL, BPCL, IOC

Nomura projected a steep sequential decline in OMC earnings, as lower marketing margins more than offset stronger refining performance. Ebitda is expected to fall 21 per cent QoQ for HPCL to Rs 6,020 crore, 16 per cent for BPCL to Rs 8,080 crore, and 15 per cent for IOCL to Rs 10,660 crore. Refining margins, however, are seen improving — HPCL at $7.3 per barrel against $3.1, BPCL at $5.6 (against $4.1), and IOCL at $6.2 (against $2.2), aided by inventory gains.

ONGC, OIL, GAIL

Upstream producers are expected to post steady growth on higher oil and gas realizations and a weaker rupee. Nomura estimated ONGC’s Ebitda at Rs 19,900 crore, up 6 per cent QoQ, with crude realisations rising 2 per cent to $67.3 per barrel. Oil India's Ebitda is seen up 10 per cent QoQ to Rs 2,300 crore, supported by higher volumes and realizations of $67.4/bbl.

GAIL, PLNG, IGL, MGL, Gujarat Gas

Nomura sees mixed trends across the gas utilities space. GAIL’s Q2 Ebitda is estimated at Rs 3210 crore (down 4 per cent QoQ), as lower profitability in LPG, liquid hydrocarbons, and petchem segments offsets stable transmission and marketing. Petronet LNG (PLNG) is expected to post a 2 per cent sequential Ebitda rise to Rs 1,330 crore, supported by higher Dahej terminal utilization at 94 per cent.

Among city gas distributors, IGL and MGL are likely to report marginal sequential declines, while Gujarat Gas (GGL) could see a sharper 11 per cent drop in Ebitda due to price cuts and higher input costs.

— the coaching institute acquired by Think & Learn in 2021.") Can Byju Raveendran still shape Byju's insolvency outcome?

Can Byju Raveendran still shape Byju's insolvency outcome? India to launch E85 fuel on World Environment Day

India to launch E85 fuel on World Environment Day Petrol, EV or Flex-Fuel? Here's which car makes most sense for your road trips in 2026

Petrol, EV or Flex-Fuel? Here's which car makes most sense for your road trips in 2026 Tomatoes push up Thali costs in May by 7% -- will onions and potatoes be next?

Tomatoes push up Thali costs in May by 7% -- will onions and potatoes be next? Can flex fuel cut your petrol bill? What the Brazil model shows us

Can flex fuel cut your petrol bill? What the Brazil model shows us Citi Sees Massive Upside In Power Stocks! ₹9.7 Lakh Crore Opportunity Ahead

Citi Sees Massive Upside In Power Stocks! ₹9.7 Lakh Crore Opportunity Ahead Midcap Winners Ahead? Siddhartha Khemka Reveals Top Themes For FY27

Midcap Winners Ahead? Siddhartha Khemka Reveals Top Themes For FY27 Govt's Big Move To Save The Rupee! Will Foreign Money Return To India?

Govt's Big Move To Save The Rupee! Will Foreign Money Return To India? Q4 Earnings Surprise! BFSI, Metals Shine As FY28 Recovery Takes Shape | Siddhartha Khemka

Q4 Earnings Surprise! BFSI, Metals Shine As FY28 Recovery Takes Shape | Siddhartha Khemka Reliance Down 17%: Is This the Best Time to Buy Before Jio Listing?

Reliance Down 17%: Is This the Best Time to Buy Before Jio Listing? 'Is this the biggest stock market scam ever? Move over, Harshad Mehta ...' — asks Sanjay Jha

'Is this the biggest stock market scam ever? Move over, Harshad Mehta ...' — asks Sanjay Jha Thangamayil Jewellery shares zoom 18% to hit record high; here's what investors should know

Thangamayil Jewellery shares zoom 18% to hit record high; here's what investors should know CG Power, Hitachi Energy India, GE Vernova shares rise up to 4% today; here's why

CG Power, Hitachi Energy India, GE Vernova shares rise up to 4% today; here's why  Bharat Forge sets record date for FY26 dividend payment; check details

Bharat Forge sets record date for FY26 dividend payment; check details Did you know? Rajesh Exports was one of the awardees of Rs 18,100 cr PLI scheme in 2022

Did you know? Rajesh Exports was one of the awardees of Rs 18,100 cr PLI scheme in 2022