Crisil estimates revenues of traditional players fell about 15% in the second half of FY25 from the first, due to lower trading activity and streamlined brokerage charges.Crisil estimates revenues of traditional players fell about 15% in the second half of FY25 from the first, due to lower trading activity and streamlined brokerage charges.

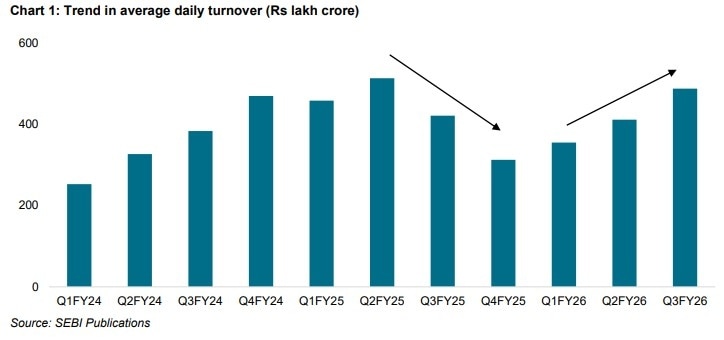

Crisil estimates revenues of traditional players fell about 15% in the second half of FY25 from the first, due to lower trading activity and streamlined brokerage charges.Crisil estimates revenues of traditional players fell about 15% in the second half of FY25 from the first, due to lower trading activity and streamlined brokerage charges.A series of SEBI measures to curb speculative activity, followed by the proposed increase in securities transaction tax (STT) on derivatives in the Union Budget 2026-27, have reduced market activity. Average daily turnover (ADTO) fell about 25% in the second half of the last fiscal, contributing to a 6% year-on-year decline in the broking industry’s revenue in the first half of FY26, according to a recent analysis by Crisil Ratings.

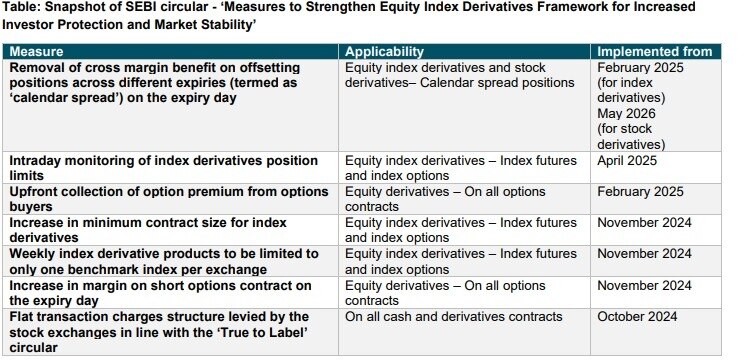

The rating agency noted that the regulatory tightening over the past few quarters has materially altered the operating environment for broking firms. Measures introduced by the Securities and Exchange Board of India (SEBI) — including curbs on weekly expiry products, higher margins on short options, upfront collection of option premiums and limits on index derivatives — were aimed at protecting retail investors and improving market stability. However, these changes have also led to a sustained moderation in trading volumes across cash and derivatives segments.

Against this backdrop, Crisil analysed the performance of 25 broking entities across FY25 and the first half of FY26, categorising them into three groups: traditional brokerages dependent largely on transaction fees, diversified players with significant non-broking income, and firms primarily engaged in proprietary trading. The findings underline a clear divergence in performance based on revenue mix.

Malvika Bhotika, Director, Crisil Ratings, said: “Our analysis of 25 players engaged in the broking business shows that entities with diversified revenue streams have typically navigated market fluctuations adeptly, while entities where transaction broking fees or proprietary trading business constitutes the predominant share of revenues, have faced decline in revenue during such periods.”

Diversified capital market players have emerged as the most resilient. For these firms, nearly two-thirds of revenue is derived from non-broking and non-trading activities such as wealth management, distribution, investment banking and interest income from margin trading facilities (MTF). This diversification helped cushion the impact of lower market volumes, with these players recording the least revenue decline during periods of heightened volatility.

In contrast, traditional brokerages were more exposed to the slowdown. Crisil estimates that revenues of traditional players fell around 15% in the second half of FY25 compared with the first half, driven by reduced trading activity and the streamlining of brokerage charges. While many firms attempted to offset the pressure by revising pricing structures and increasing focus on margin trading, these measures were insufficient to fully counter the decline. As a result, revenues in the first half of FY26 remained below year-ago levels, despite a marginal sequential improvement.

Proprietary trading firms bore the sharpest impact. With SEBI’s decision to limit weekly expiry products reducing arbitrage opportunities, revenues of proprietary players dropped about 25% in the second half of FY25 over the first half. Although some stability in market volumes led to a modest recovery in the first half of FY26, Crisil cautioned that the proposed STT hike could further strain this segment. Proprietary traders, including high-frequency traders and arbitrageurs, account for nearly 60% of market volumes, making them particularly sensitive to transaction cost increases.

Prashant Mane, Associate Director, Crisil Ratings, said: “With the regulatory measure of reducing weekly expiry products resulting in fewer arbitrage opportunities, proprietary players saw revenue drop by ~25% during the second half of fiscal 2025 over the first half, with a slight improvement in the first half of fiscal 2026 owing to some stability in market volume. Going ahead, the proposed hike in STT could have a higher impact on proprietary traders, including high-frequency traders and arbitrageurs, who account for ~60% of the market volume.”

The report also flags broader implications for market liquidity. Higher transaction costs and regulatory constraints could discourage trading activity, potentially affecting price discovery and participation, especially in derivatives. While rising interest income from margin trading has provided some cushion to brokers, Crisil emphasised that expanding revenue from other non-cyclical sources is becoming increasingly critical.

Most broking firms have already initiated steps towards diversification, as reflected in a gradual shift in revenue mix over the past year. However, Crisil noted that the pace and effectiveness of these efforts will be key to determining how well firms can withstand further regulatory changes or external shocks. As policy tightening reshapes India’s capital markets, diversification is no longer optional but central to the sustainability of the broking business model.

Centre to launch new series WPI, producer price indices on June 15

Centre to launch new series WPI, producer price indices on June 15 Oyo parent Prism gets Sebi nod for ₹6,650-cr IPO; eyes $7-8 bn valuation

Oyo parent Prism gets Sebi nod for ₹6,650-cr IPO; eyes $7-8 bn valuation Mother Dairy expects 5% growth in FY27; eyes expansion beyond Delhi-NCR

Mother Dairy expects 5% growth in FY27; eyes expansion beyond Delhi-NCR, Wipro and Tech Mahindra have seen renewed buying interest.") IT stocks stage a comeback: Five factors supporting the strong upmove

IT stocks stage a comeback: Five factors supporting the strong upmove ‘This is an incredible time to be a…’: Nvidia CEO Jensen Huang said on ‘SaaSpocalypse’

‘This is an incredible time to be a…’: Nvidia CEO Jensen Huang said on ‘SaaSpocalypse’ From Global Uncertainty To India's Opportunity: The Big Economic Outlook

From Global Uncertainty To India's Opportunity: The Big Economic Outlook Godrej Industries Is Entering The Wealth Management Space As It Looks To Scale Up Financial Services

Godrej Industries Is Entering The Wealth Management Space As It Looks To Scale Up Financial Services SIP Vs SWP: The Two-Step Mutual Fund Strategy That Could Help Become A Millionaire & Retire Early?

SIP Vs SWP: The Two-Step Mutual Fund Strategy That Could Help Become A Millionaire & Retire Early? Daily Calls LIVE: Ask Your STOCK MARKET TODAY QUERIES | Market Update LIVE | Share Market News Today

Daily Calls LIVE: Ask Your STOCK MARKET TODAY QUERIES | Market Update LIVE | Share Market News Today Retired At 39! How Sanjay Kathuria Turned A ₹2,000 SIP Into Complete Financial Freedom

Retired At 39! How Sanjay Kathuria Turned A ₹2,000 SIP Into Complete Financial Freedom Tata Tech, Bharti Airtel, PFC, BLS International shares: Should you enter at current levels?Oyo parent Prism gets Sebi nod for ₹6,650-cr IPO; eyes $7-8 bn valuation

Tata Tech, Bharti Airtel, PFC, BLS International shares: Should you enter at current levels?Oyo parent Prism gets Sebi nod for ₹6,650-cr IPO; eyes $7-8 bn valuation Rs 75/share dividend by Tata Group stock – Record date next week IT stocks stage a comeback: Five factors supporting the strong upmove

Rs 75/share dividend by Tata Group stock – Record date next week IT stocks stage a comeback: Five factors supporting the strong upmove CMR Green Technologies IPO: GMP zooms 130% in a week; should you subscribe?

CMR Green Technologies IPO: GMP zooms 130% in a week; should you subscribe?