Lupin is expected to sustain double-digit revenue growth in FY26, led by strong US market execution, new launches like Glucagon and Liraglutide.

Lupin is expected to sustain double-digit revenue growth in FY26, led by strong US market execution, new launches like Glucagon and Liraglutide. Lupin is expected to sustain double-digit revenue growth in FY26, led by strong US market execution, new launches like Glucagon and Liraglutide.

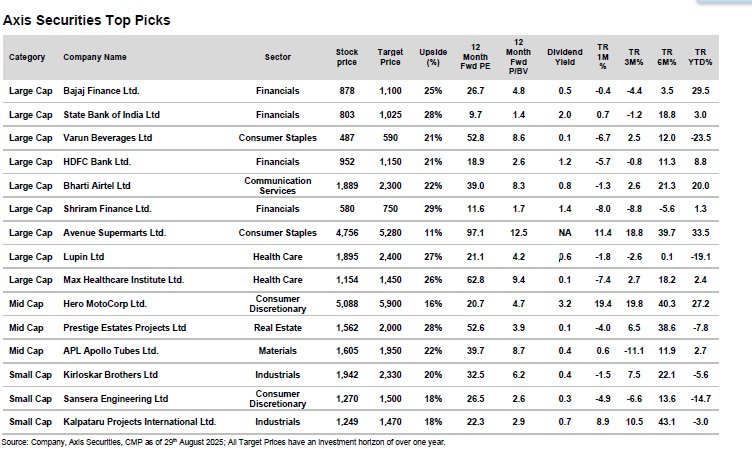

Lupin is expected to sustain double-digit revenue growth in FY26, led by strong US market execution, new launches like Glucagon and Liraglutide.Axis Securities, in its September note, identified 15 stocks, with 11 of them expected to generate returns of over 20 per cent in the next 12 months. Shriram Finance tops the list with an estimated 29 per cent upside, followed by Prestige Estates Projects and State Bank of India at 28 per cent each. Lupin is projected to deliver 27 per cent, Max Healthcare Institute 26 per cent, Bajaj Finance 25 per cent, and APL Apollo Tubes 22 per cent.

On Shriram Finance, Axis Securities said demand buoyancy in the rural markets and healthy growth visibility across most of the segment may help the NBFC deliver a consistent and healthy 15 per cent CAGR AUM growth over the medium term. NIMs should find support from the easing of excess liquidity and the gradual downward repricing of cost of fund.

"Consistent growth delivery while maintaining asset quality alongside NIM improvement on expected lines should drive stock performance. At current levels, we believe the risk-reward is favourable," Axis Securities said as it suggested a target of Rs 750 on the stock.

On Prestige Estates, Axis Securities said the company has set FY26 guidance targeting pre-sales of Rs 27,000 Cr and a robust launch pipeline with Rs 43,000 crore in GDV. The strong Q1 performance, particularly in NCR, establishes a solid base for achieving these targets. Q2 launches are expected to contribute Rs 12,000 crore GDV, and management remains confident of sustaining the sales momentum, the brokerage said as it suggested a target of Rs 2,800 on the stock.

SBI, Axis Securities said, remains well-poised to sustain its growth momentum, supported by its comfortable LDR, providing it with leverage to accelerate credit growth.

"While near-term pressures are expected to be visible on NIMs, benefit from deposit rate cuts, which will reflect in CoF from H2 onwards, should support NIM recovery. Asset quality does not pose challenges, and thus, credit costs should remain benign. Collectively, this should ensure a comfortable 1 per cent RoA delivery over FY26-28E. The recent QIP has strengthened the Tier I capital, adequate to fuel medium-term growth," it said.

Lupin is expected to sustain double-digit revenue growth in FY26, led by strong US market execution, new launches like Glucagon and Liraglutide, and a robust injectable and biosimilar pipeline. While some loss of exclusivity in FY27 may create near-term volatility, the management projected high single-digit to potential double-digit growth, supported by new approvals including Risperdal, Pegfilgrastim, and Ranibizumab.

"Ebitda margins are expected to remain healthy at 24–25 per cent in FY26, with further expansion in FY27, driven by premium product mix and continued cost optimisation." Axis Securities said.

The brokerage values Max Healthcare at 35 times estimated EV/ Ebitda for H1FY28. The company management reiterated guidance of 3–7 per cent ARPOB growth in mature hospitals, led by higher case complexity and clinical mix, alongside sustained 80 per cent occupancy levels.

"Developing hospitals are expected to ramp up gradually, driving incremental occupancy and revenue growth. Focus remains on scaling oncology and international patient business while maintaining strong return ratios," the brokerage said.

Bajaj Finance is set to witness improved margins, supported by faster transmission of the rate cuts in CoF and an optimal borrowing mix, Axis Securities said. While the majority of the segment continues to deliver healthy growth, emerging stress in the MSME segment could weigh on near-term growth for the company, it said.

"With the growth drivers intact, we believe APL Apollo tubes is well positioned to capture India’s infrastructure growth. We project Ebitda CAGR of 38 per cent over FY25-27E. The stock is trading at a 12-month forward P/E of 35x. We maintain our Buy rating on the stock with a target of Rs 1,950," Axis Securities said.

'Join Abraham Accords or stay out of Iran deal': Trump's message to Saudi Arabia, Pakistan and others

'Join Abraham Accords or stay out of Iran deal': Trump's message to Saudi Arabia, Pakistan and others  India overtakes US in electric car penetration for the first time

India overtakes US in electric car penetration for the first time 'India cannot afford fear-mongering': FM Sitharaman says economy is robust. Here's the proof

'India cannot afford fear-mongering': FM Sitharaman says economy is robust. Here's the proof Fuel, fertiliser, forex: FM Sitharaman calls for focus on the 3Fs amid global pressures

Fuel, fertiliser, forex: FM Sitharaman calls for focus on the 3Fs amid global pressures") Has your SIP given FIIs an exit? Capitalmind CEO disagrees with the logic. Here's why

Has your SIP given FIIs an exit? Capitalmind CEO disagrees with the logic. Here's why Who Will Lead Karnataka? Siddaramaiah & DKS Head To Delhi Amid Power Buzz

Who Will Lead Karnataka? Siddaramaiah & DKS Head To Delhi Amid Power Buzz "OMCs Are Not Profiteering With Fuel Price Hike, Past Profits Are Being Wiped Out In Just A Quarter"

"OMCs Are Not Profiteering With Fuel Price Hike, Past Profits Are Being Wiped Out In Just A Quarter" Why Centre Wants Delhi Gymkhana’s Prime Land | Elite Club Faces Eviction Battle

Why Centre Wants Delhi Gymkhana’s Prime Land | Elite Club Faces Eviction Battle New U.S. Green Card Rules To Hit Lakhs Of Indians Waiting In America Hard

New U.S. Green Card Rules To Hit Lakhs Of Indians Waiting In America Hard Big Day For Tata Group | Will N Chandrasekaran Get Another Term?

Big Day For Tata Group | Will N Chandrasekaran Get Another Term? SpaceX IPO: How can you subscribe to world's biggest IPO ever? Here's what rules say

SpaceX IPO: How can you subscribe to world's biggest IPO ever? Here's what rules say Sensex, Nifty outlook: What could shape market trade tomorrow?

Sensex, Nifty outlook: What could shape market trade tomorrow? This smallcap staged a massive 300% comeback in Q4 profits. Here's how the magic happened

This smallcap staged a massive 300% comeback in Q4 profits. Here's how the magic happened Trent shares fall 31% from 52-week high, price target and outlook

Trent shares fall 31% from 52-week high, price target and outlook KPIT Tech, L&T Technology: Brokerage shares top 2 IT stock picks; check target, outlook

KPIT Tech, L&T Technology: Brokerage shares top 2 IT stock picks; check target, outlook