In the wake of difficulties faced by numerous borrowers during coronavirus-related lockdown, the union government has decided to offer relief to retail and MSME borrowers who had active loan accounts during the period March 1, 2020 to August 31, 2020. All eligible borrowers will receive an amount of relief, which will be the difference between simple interest and compound interest during the six-month period from March to August 2020, in their respective account by November 5, 2020.

Pushed by the Supreme Court, this may appear to be a good relief for the borrowers. "This will help in alleviating some of the financial burden faced by individual and MSME borrowers hit hard by the pandemic and consequent lockdown. We hope this will bring some cheer on the faces of the borrowers during this festival time and hopefully also help lenders recover some of their dues," says Mayur Modi, Co-founder and Co-CEO, Moneyboxx Finance Ltd.

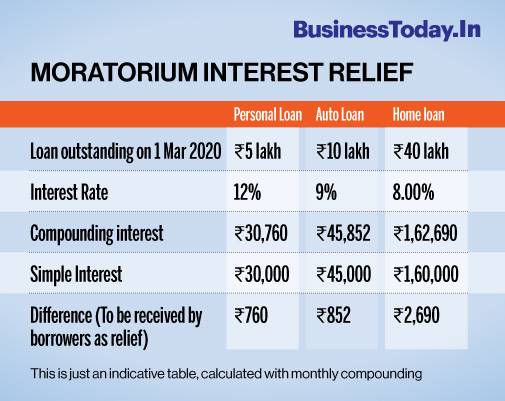

However, when you dig a little deeper the picture does not look rosy for borrowers. Going by the basic method of computation, the benefit for retail borrowers appears to be marginal. For example, if you have a home loan which had an outstanding of Rs 40 lakh, the difference between the compound interest and simple interest at 8 per cent for the concerned six-month period comes out to be only Rs 2,690. It means that while the borrowers will bear the burden of Rs 1.6 lakh interest payment during the period, the relief they will get through government under this scheme is only Rs 2,690.

When it comes to other small-ticket loans like auto loan, personal loan and consumer durables loan, the actual benefit that the borrowers get will be much lower.

Which loans are eligible

This relief is limited to only specific types of loans, including MSME loans, education loans, housing loans, consumer durables loans, credit card dues, automobile loans, personal loans to professionals and consumption loans.

More clarity will be needed on personal loans as only one type of such loan - for professionals - has been mentioned in government notification. However, the notification also covers consumption loan which has not been elaborated whether all personal loans will fall under this category or not.

Moreover, not only term loans but other credit facilities like overdraft, cash credit and revolving credit of a credit card are also eligible for this benefit and.

Conditions for relief eligibility

To be eligible for this relief the loan account should not have been a non-performing asset (NPA) on February 29, 2020, which means it should have been categorised as standard regular asset by lender on this date. In other words there should not be any default on repayment by the borrower till February end this year.

"So for any borrower who has maintained their account in standard state and has been making timely payments pre-COVID is eligible for this credit. For the customers who opted into moratorium, they will be just required to pay the simple interest in their outstanding and any compounded interest will be waived by the financial institution," says Anil Pinapala, CEO, Vivifi Finace India.

The aggregate loan outstanding amount including all lending facilities through all lending institutions should not be more than Rs 2 crore on February 29, 2020. While the majority of retail borrowers will not be impacted by this limit, many MSME borrowers will lose their eligibility when total outstanding with all lending institutions will be considered.

Interest rate calculation may vary

When it comes to term loans, the interest rate prevailing on February 29, 2020, will be taken for calculating the difference between simple and compound interest. This will remain same even in cases where the interest rate changed during the following 6 months period. This will increase the benefit for floating rate loans like home loan which witnessed reduction of interest rate but will get the reimbursement at higher rate.

For the overdraft or cash credit facility the simple interest would be calculated on daily balance for the concerned six-month period at the interest rate prevailing on February 29 this year. However, the compound interest will be calculated at monthly interval for the same period.

The methodology for charging credit card dues is totally different as for credit card dues the interest rate which will be used is Weighted Average Lending rate (WALR) charged by the lender on EMI facilities and not on revolving credit. It means that the interest rate used will be much lower because the rate charged on EMI conversion are much lower than the ones charged on revolving credit.

Not related to moratorium exercise

All types of borrowers, whether availed the loan moratorium for full six months or only for few months or did not avail the moratorium will be eligible for this interest relief. This relief will apply even to those borrowers who closed their loan accounts in the middle of this period by completing the repayment. If the loan was closed during this period then the amount will be calculated only till its last day of closing.

"This measure is being implemented in a fashion that it is uniformly applicable to all borrowers and doesn't put the good paying customers at any disadvantage and this particular aspect has to be highly appreciated," says Pinapala of Vivifi Finace India.

ALSO READ: Finance Ministry issues guidelines for implementation of interest waiver on loan

RBI continues to bring more gold back to India. Here's why

RBI continues to bring more gold back to India. Here's why KPIT to acquire Israeli auto cybersecurity firm Cymotive for up to $120 million

KPIT to acquire Israeli auto cybersecurity firm Cymotive for up to $120 million BT Exclusive: From JEE tutor to defence-tech founder - how olee.space delivered one of India's first start-up built laser weapons

BT Exclusive: From JEE tutor to defence-tech founder - how olee.space delivered one of India's first start-up built laser weapons Suvendu Adhikari's close aide shot dead from close range in West Bengal's Madhyamgram

Suvendu Adhikari's close aide shot dead from close range in West Bengal's Madhyamgram FD investors, don’t miss this! These banks now offer over 8% returns

FD investors, don’t miss this! These banks now offer over 8% returns Isha Ambani Brings India To Met Gala 2026 With Gold Saree & Rare Nizam Jewel

Isha Ambani Brings India To Met Gala 2026 With Gold Saree & Rare Nizam Jewel Tamil Nadu Assembly Twist: Vijay in Focus As Alliance Talks With Congress & AIADMK Grow

Tamil Nadu Assembly Twist: Vijay in Focus As Alliance Talks With Congress & AIADMK Grow Smriti Irani’s Strong Response To Rahul Gandhi And Mamata Banerjee On Election Controversy

Smriti Irani’s Strong Response To Rahul Gandhi And Mamata Banerjee On Election Controversy Twin Blasts In Punjab: Terror Plot Or Political War Ahead Of Elections?

Twin Blasts In Punjab: Terror Plot Or Political War Ahead Of Elections? Nothing’s Watch 3 Pro: Budget Smartwatch With AI Coach & Dual GPS

Nothing’s Watch 3 Pro: Budget Smartwatch With AI Coach & Dual GPS Bajaj Auto Q4 profit jumps 34%; announces up to Rs 5,633 crore buyback, Rs 150 dividend

Bajaj Auto Q4 profit jumps 34%; announces up to Rs 5,633 crore buyback, Rs 150 dividend Sensex, Nifty outlook for tomorrow: What's next after today's sharp upmove?

Sensex, Nifty outlook for tomorrow: What's next after today's sharp upmove? Jupiter Wagons, Titagarh Rail Systems shares jump 15–32% in a month: Outlook, strategy | Daily Calls on BTTV

Jupiter Wagons, Titagarh Rail Systems shares jump 15–32% in a month: Outlook, strategy | Daily Calls on BTTV 3750% dividend stock alert! Bumper amount in Q4 results; record date fixed

3750% dividend stock alert! Bumper amount in Q4 results; record date fixed BT Closing Bell | Sensex, Nifty end higher amid US-Iran peace hopes; top gainers & losers

BT Closing Bell | Sensex, Nifty end higher amid US-Iran peace hopes; top gainers & losers