54EC bonds like NHAI and REC offer tax relief, however, experts say paying the capital gains tax and investing elsewhere might yield more.54EC bonds like NHAI and REC offer tax relief, however, experts say paying the capital gains tax and investing elsewhere might yield more.

54EC bonds like NHAI and REC offer tax relief, however, experts say paying the capital gains tax and investing elsewhere might yield more.54EC bonds like NHAI and REC offer tax relief, however, experts say paying the capital gains tax and investing elsewhere might yield more.Selling a property often comes with a sweet profit—but also a bitter tax bill. Long-term capital gains (LTCG) on the sale of land or buildings attract a 12.5% tax (plus cess), and many sellers scramble to invest in 54EC bonds like those issued by NHAI or REC to save on this levy. But is this the smartest move financially?

According to Sujit Bangar, Founder of Tax Buddy, the answer depends on your investment horizon, risk appetite, and financial goals. “Most people blindly rush to 54EC bonds to save tax, but they may be missing out on higher returns elsewhere,” he notes.

Two primary ways to save capital gains tax

Under the Income Tax Act, there are two major routes to tax exemption on LTCG:

Section 54/54F – Reinvest the capital gain into a new residential property.

Section 54EC – Invest in notified bonds such as NHAI or REC within six months of the sale.

The 54EC route is popular because it's relatively low-risk and requires no involvement in the real estate market again. But this “safe” option comes with limitations.

What are 54EC bonds?

54EC bonds are fixed-income instruments issued by government-backed entities such as the National Highways Authority of India (NHAI) and the Rural Electrification Corporation (REC). You can invest up to ₹50 lakh across the year of sale and the next financial year combined. The bonds come with a lock-in period of five years, and they cannot be pledged, sold, or used as loan collateral.

Crucially, the interest income is taxable, and the returns aren’t exactly attractive. Currently, they offer about 5.25% per annum, which falls to just 3.75% post-tax if you’re in the 30% income slab.

Risk vs reward: Should you still go for it?

Let’s break it down with an example.

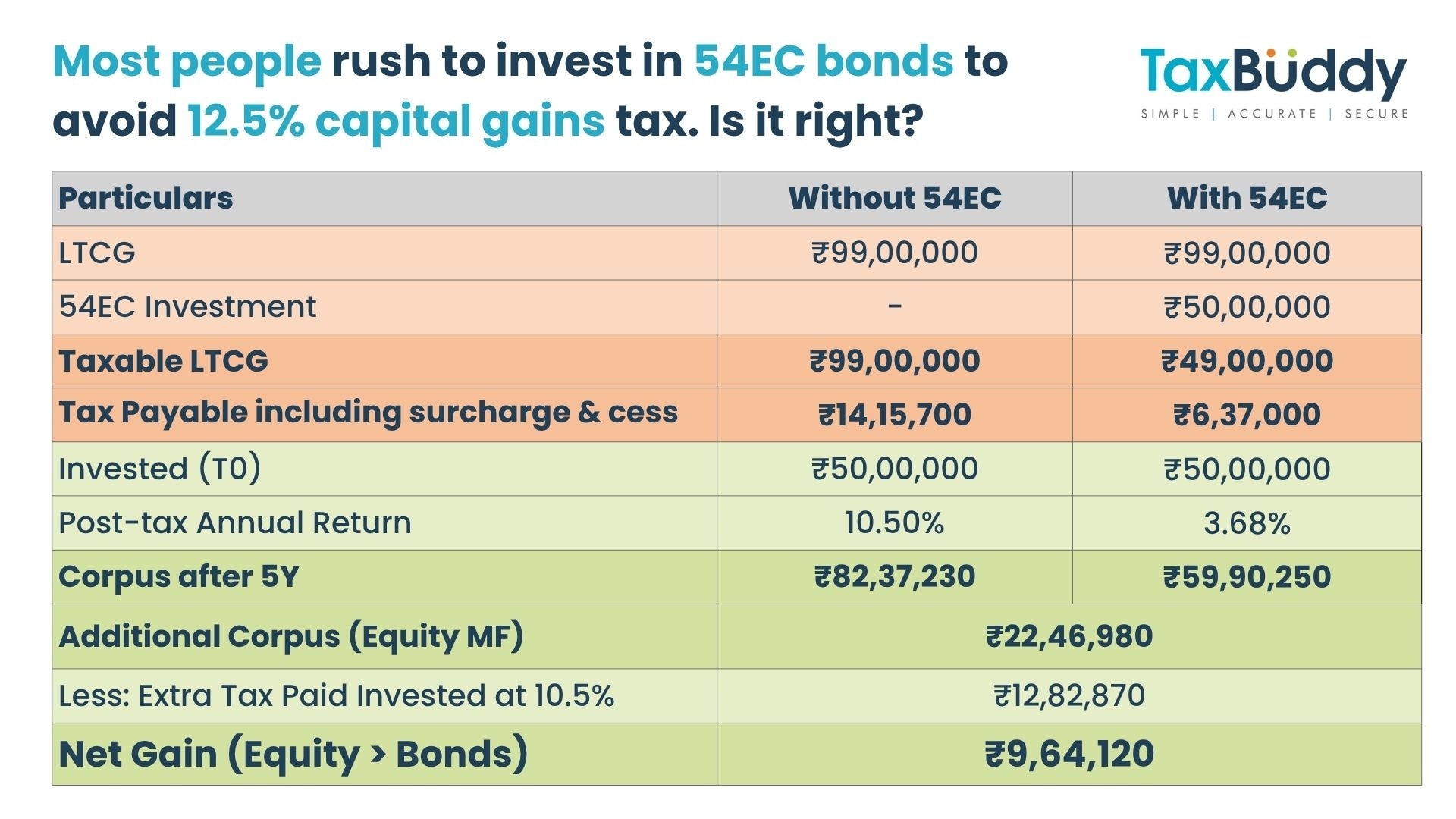

Say Ms. A sells a property and earns Rs 50 lakh in capital gains. If she doesn’t reinvest, she pays Rs 6.5 lakh in LTCG tax. To save this, she invests the Rs 50 lakh in 54EC bonds.

Over 5 years, she earns roughly Rs 13.1 lakh in interest (taxable), and she’s saved Rs 6.5 lakh in tax. But her capital remains locked and earns modest returns.

Now, if she paid the Rs 6.5 lakh tax upfront and invested the remaining Rs 43.5 lakh in an equity mutual fund (assuming a 12% CAGR), she could end up with Rs 76.7 lakh in 5 years, even after factoring in tax on mutual fund gains. That’s a Rs 9.6 lakh difference in her favour—without the five-year lock-in.

So, what’s better?

If your only goal is tax savings, and you don’t want any market-linked risk, 54EC bonds are a safe bet, Bangar added.

But if you’re comfortable with short-term volatility and can think long term, paying the tax and investing elsewhere, like in equity mutual funds, a balanced hybrid fund, or even arbitrage funds, could deliver significantly better returns.

“Let your financial goals—not just the urge to save tax—guide your decision,” Bangar advised.

In essence, 54EC bonds reduce tax, but possibly at a cost. Think before you lock in ₹50 lakh for five years when smarter alternatives might work harder for you.

, Wipro and Tech Mahindra have seen renewed buying interest.") IT stocks stage a comeback: Five factors supporting the strong upmove

IT stocks stage a comeback: Five factors supporting the strong upmove ‘This is an incredible time to be a…’: Nvidia CEO Jensen Huang said on ‘SaaSpocalypse’

‘This is an incredible time to be a…’: Nvidia CEO Jensen Huang said on ‘SaaSpocalypse’ 'Over 1 lakh attempts': CBSE claims cyberattacks by 'malicious actors' on revaluation portal

'Over 1 lakh attempts': CBSE claims cyberattacks by 'malicious actors' on revaluation portal Apollo Micro, Persistent Systems: These stocks set for more upside? Here what expert say

Apollo Micro, Persistent Systems: These stocks set for more upside? Here what expert say Annamalai-BJP breakup complete? Former 'Singham' has THIS plan for Tamil Nadu

Annamalai-BJP breakup complete? Former 'Singham' has THIS plan for Tamil Nadu Godrej Industries Is Entering The Wealth Management Space As It Looks To Scale Up Financial Services

Godrej Industries Is Entering The Wealth Management Space As It Looks To Scale Up Financial Services SIP Vs SWP: The Two-Step Mutual Fund Strategy That Could Help Become A Millionaire & Retire Early?

SIP Vs SWP: The Two-Step Mutual Fund Strategy That Could Help Become A Millionaire & Retire Early? Daily Calls LIVE: Ask Your STOCK MARKET TODAY QUERIES | Market Update LIVE | Share Market News Today

Daily Calls LIVE: Ask Your STOCK MARKET TODAY QUERIES | Market Update LIVE | Share Market News Today Retired At 39! How Sanjay Kathuria Turned A ₹2,000 SIP Into Complete Financial Freedom

Retired At 39! How Sanjay Kathuria Turned A ₹2,000 SIP Into Complete Financial Freedom What’s Hot: Stocks, Gold & Big Money Moves | Daily Market Show | Business Today TV

What’s Hot: Stocks, Gold & Big Money Moves | Daily Market Show | Business Today TV Rs 75/share dividend by Tata Group stock – Record date next week IT stocks stage a comeback: Five factors supporting the strong upmove

Rs 75/share dividend by Tata Group stock – Record date next week IT stocks stage a comeback: Five factors supporting the strong upmove CMR Green Technologies IPO: GMP zooms 130% in a week; should you subscribe?

CMR Green Technologies IPO: GMP zooms 130% in a week; should you subscribe? Hindalco Industries, APL Apollo Tubes shares: Axis Direct's top metal bets; check target prices, outlook

Hindalco Industries, APL Apollo Tubes shares: Axis Direct's top metal bets; check target prices, outlook L&T, BEML, Belrise, CG Power shares: Short-term target prices

L&T, BEML, Belrise, CG Power shares: Short-term target prices