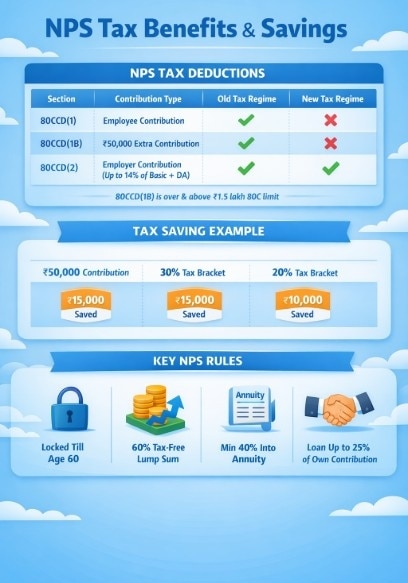

Tax benefits under NPS are available in three parts — Section 80CCD(1), Section 80CCD(1B), and Section 80CCD(2).Tax benefits under NPS are available in three parts — Section 80CCD(1), Section 80CCD(1B), and Section 80CCD(2).

Tax benefits under NPS are available in three parts — Section 80CCD(1), Section 80CCD(1B), and Section 80CCD(2).Tax benefits under NPS are available in three parts — Section 80CCD(1), Section 80CCD(1B), and Section 80CCD(2).The National Pension System (NPS) is gaining attention ahead of the March 31 tax deadline, as changes in rules and lesser-known deductions allow investors to claim additional tax benefits beyond the standard ₹1.5 lakh limit under Section 80C. Financial experts say the scheme now offers both tax savings and long-term retirement planning advantages, especially for salaried individuals.

Recent reforms have made NPS more flexible. Subscribers can now withdraw up to 80% of their corpus as a lump sum at retirement, compared to the earlier 60%, while at least 20% must still be used to buy an annuity. In addition, NPS accounts can now be used as collateral for loans of up to 25% of personal contributions, reducing the need for premature withdrawals. These features have increased the appeal of the scheme among private-sector employees and self-employed individuals looking for disciplined retirement savings.

Extra ₹50,000 deduction

Contribution to the NPS remains one of the few tax-saving options available under both the old and the new tax regimes, though the benefits are higher in the old regime.

Capital markets banker and investment expert Aditya Garg said many investors are unaware that NPS provides a separate tax deduction of ₹50,000 that is not part of the ₹1.5 lakh limit under Section 80C.

“NPS offers tax benefits under both the old and new tax regimes, though the structure differs. NPS gives you ₹50,000 in extra tax deduction, not inside your ₹1.5 lakh 80C limit, but on top of it,” he said.

Tax benefits under NPS are available in three parts — Section 80CCD(1), Section 80CCD(1B), and Section 80CCD(2). Most taxpayers use only the first one, which falls within the ₹1.5 lakh limit, but the real advantage lies in the additional deductions.

Under Section 80CCD(1B), investors can claim an extra ₹50,000 deduction by contributing to their NPS Tier-I account after exhausting the ₹1.5 lakh limit. For those in the 30% tax bracket, this can mean savings of about ₹15,000 per year, while those in the 20% bracket can save around ₹10,000.

However, this extra ₹50,000 deduction is available only under the old tax regime.

Deduction that works in both regimes

Experts say the most powerful and least used NPS benefit is under Section 80CCD(2), which applies to the employer’s contribution to NPS.

Under this provision, an employer can contribute up to 14% of basic salary plus dearness allowance, and the entire amount is deductible from taxable income. This benefit is available under both the old and the new tax regime and does not count toward the ₹1.5 lakh limit under Section 80C.

Tax planners say employees can ask their HR or payroll department to route part of their cost-to-company (CTC) as employer NPS contribution, which can significantly reduce tax without increasing the employer’s cost.

NPS as retirement support

Under the old system, deductions are allowed for employee contribution up to ₹1.5 lakh, an additional ₹50,000 under a separate limit, and employer contribution of up to 14% of salary. In the new tax regime, only the employer’s contribution to NPS qualifies for deduction, which reduces the overall tax advantage.

Apart from tax benefits, NPS is considered a disciplined long-term retirement tool as the investment remains locked until retirement, helping investors build a stable pension corpus. The scheme offers diversified exposure across equities and government securities and now allows a longer investment horizon, though liquidity remains limited compared with mutual funds.

Lock-in remains the biggest drawback

Despite the tax benefits, experts caution that NPS is not a liquid investment. Tier-I accounts remain locked until the age of 60, with partial withdrawals allowed only under specific conditions.

At maturity, 60% of the corpus can be withdrawn tax-free, while the remaining 40% must be used to buy an annuity, which is taxed as income.

With the financial year nearing its end, investors who want to claim the additional ₹50,000 deduction must contribute to their NPS Tier-I account before March 31, making the coming weeks crucial for tax planning.

Nothing is better than biofuels for immediate carbon reduction: Hero MotoCorp CEO

Nothing is better than biofuels for immediate carbon reduction: Hero MotoCorp CEO Is AI sustainable? Why the debate goes beyond data centres and energy use

Is AI sustainable? Why the debate goes beyond data centres and energy use AI gold rush: How tech boom created a record $20.1 trillion billionaire class

AI gold rush: How tech boom created a record $20.1 trillion billionaire class Monsoon races ahead after Kerala delay: Enters Maharashtra, when will it reach Delhi?

Monsoon races ahead after Kerala delay: Enters Maharashtra, when will it reach Delhi? ‘Global debt has crossed $330 trillion, world moving beyond the dollar’: Kremlin adviser Anton Kobyakov

‘Global debt has crossed $330 trillion, world moving beyond the dollar’: Kremlin adviser Anton Kobyakov #BTSustainabilityAwards LIVE: Grand Award Ceremony & Special Edition Magazine Launch!

#BTSustainabilityAwards LIVE: Grand Award Ceremony & Special Edition Magazine Launch! #BTSustainabilityAwards LIVE: Environment Minister Bhupender Yadav On India's Green Future

#BTSustainabilityAwards LIVE: Environment Minister Bhupender Yadav On India's Green Future #BTSustainabilityAwards LIVE: The Eco Drive - Will Flex-Fuel & EVs Redefine India's Mobility?

#BTSustainabilityAwards LIVE: The Eco Drive - Will Flex-Fuel & EVs Redefine India's Mobility? #BTSustainabilityAwards LIVE: The Organic Shift - How Conscious Consumers Reshape The FMCG Market

#BTSustainabilityAwards LIVE: The Organic Shift - How Conscious Consumers Reshape The FMCG Market #BTSustainabilityAwards LIVE: ESG Over Profits? Redefining Business For Long -Term Value

#BTSustainabilityAwards LIVE: ESG Over Profits? Redefining Business For Long -Term Value Sensex, Nifty outlook for Monday, June 8: GIFT Nifty down 356 pts – What to expect from stock market?

Sensex, Nifty outlook for Monday, June 8: GIFT Nifty down 356 pts – What to expect from stock market? Titan shares up 20% in a year; still a ‘Buy’? - Check share price target

Titan shares up 20% in a year; still a ‘Buy’? - Check share price target Subscribed 127 times, all about CMR Green Technologies IPO latest gmp, allotment status check online, listing date

Subscribed 127 times, all about CMR Green Technologies IPO latest gmp, allotment status check online, listing date US stock market news: Why Nasdaq, S&P 500 witnessed its worst day of year - Factors behind fall

US stock market news: Why Nasdaq, S&P 500 witnessed its worst day of year - Factors behind fall CMR Green Tech IPO attracts over Rs 56,200 crore bids, subscribed 127 times; check GMP, listing timeline

CMR Green Tech IPO attracts over Rs 56,200 crore bids, subscribed 127 times; check GMP, listing timeline