ULIPs continue to offer tax benefits, but only within clearly defined limits now.ULIPs continue to offer tax benefits, but only within clearly defined limits now.

ULIPs continue to offer tax benefits, but only within clearly defined limits now.ULIPs continue to offer tax benefits, but only within clearly defined limits now.Unit Unit-linked insurance Plans were long positioned as a versatile investment, blending insurance protection with equity-linked returns and favourable tax treatment. That narrative has shifted in recent years, as tighter tax rules have narrowed exemptions—particularly for higher-premium ULIPs—leaving investors far more exposed to scrutiny if these products are not taxed and reported correctly.

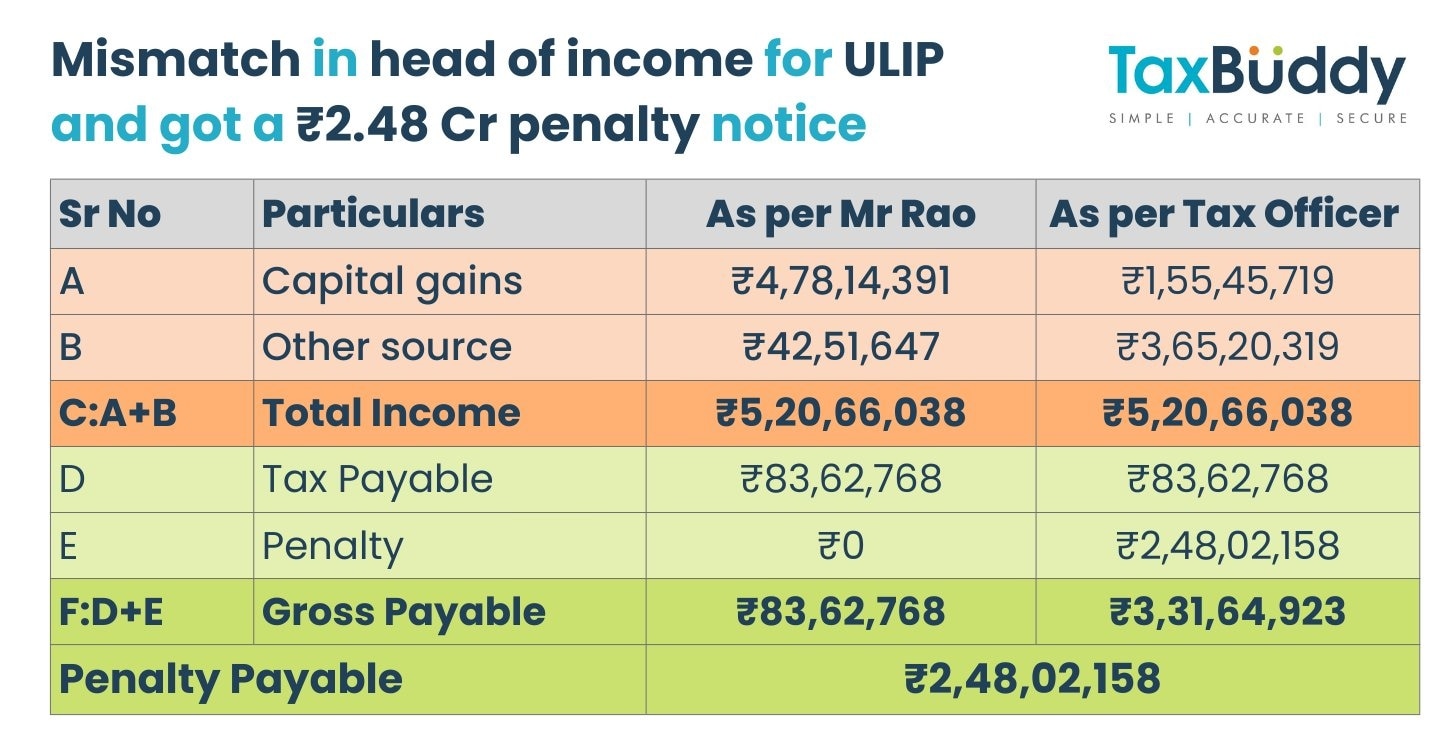

In one such case, an individual identified as Mr Rao surrendered three ULIP policies purchased from Bajaj Allianz Life Insurance about 14 years earlier. The total investment amounted to Rs 75 lakh, while the surrender resulted in net long-term gains of Rs 3.22 crore. In his income tax return, Mr Rao reported this amount under the head “capital gains.” However, the tax department took the view that the gains were taxable under “income from other sources” instead. This difference in classification triggered a tax notice, and the assessing officer eventually imposed a penalty of Rs 2.48 crore, alleging misreporting of income.

Tax advisory platform Tax Buddy highlighted that the Income Tax Appellate Tribunal (ITAT) later ruled that merely classifying income under an incorrect head does not amount to “misreporting,” provided there is full and transparent disclosure. In Mr Rao’s case, the Rs 3.22 crore gain from the surrender of ULIP policies was clearly disclosed in his return for FY20. While the tax officer reclassified the income under a different head, there was no allegation of concealment or understatement of income. Despite this, a steep penalty under Section 270A of the Income-tax Act was imposed—an action the ITAT ultimately found unjustified and set aside. The ruling offers an important precedent for ULIP holders and taxpayers more broadly.

The case and the ruling

In a significant order, the Hyderabad Bench of the Income Tax Appellate Tribunal clarified that reporting income under an incorrect head does not automatically amount to misreporting when the income itself is fully and truthfully disclosed. The case involved a non-resident individual whose return for Assessment Year 2020–21 was selected for scrutiny. The taxpayer had declared income under both capital gains and income from other sources, including ₹3.22 crore arising from the surrender of units of the Bajaj Equity Plus Fund, which was reported as capital gains.

During assessment, the assessing officer accepted the quantum of income but held that the surrender proceeds were taxable under “income from other sources” rather than capital gains. Although there was no dispute regarding the amount disclosed, the officer initiated penalty proceedings under Section 270A, treating the issue as misreporting of income. The penalty was subsequently confirmed by the Commissioner (Appeals).

On further appeal, the ITAT overturned the penalty. The Tribunal observed that the taxpayer had made full disclosure of the income in both the return and the accompanying computation statement. It noted that the disagreement was confined to the correct head of taxation and did not involve any suppression of facts, false entries, or misleading claims. Importantly, the Tribunal pointed out that Section 270A(9) clearly defines what constitutes misreporting, and a bona fide difference of opinion on classification does not fall within those parameters. Accordingly, the penalty was held to be unsustainable and was deleted.

The tax breakup

The case also highlights how a simple mismatch in the head of income can escalate into a massive penalty notice, even when there is no impact on total income or tax payable. Mr Rao reported Rs 4.78 crore as capital gains and Rs 42.5 lakh as income from other sources. The tax officer reclassified a substantial portion of the capital gains under “income from other sources.” Crucially, total income of Rs 5.20 crore and tax payable of Rs 83.6 lakh remained unchanged in both calculations. Despite this, the reclassification alone led to a Rs 2.48 crore penalty for alleged misreporting—later struck down by the ITAT due to full disclosure and absence of concealment.

ULIPs and taxes

ULIPs continue to offer tax benefits, but only within clearly defined limits. Under Section 80C of the Income Tax Act, 1961, premiums paid for ULIPs are eligible for deduction up to Rs 1.5 lakh per year, provided the annual premium does not exceed 10% of the sum assured and the policy is held for a minimum of five years. These benefits, however, are subject to strict conditions and exclusions.

A major shift came with Budget 2021, which made maturity proceeds from ULIPs taxable if the annual premium exceeds Rs 2.5 lakh across all policies issued on or after February 1, 2021. Such ULIPs are now taxed in a manner similar to mutual funds, including taxation on fund switches. Only death benefits continue to remain fully tax-exempt, irrespective of the premium size.

") 'Never seen so many tankers': India's Russian crude imports may hit record high in June

'Never seen so many tankers': India's Russian crude imports may hit record high in June Delhi EV policy approved: Road tax exempted for cars up to ₹30 lakh; ₹50,000 subsidies for EV buyers

Delhi EV policy approved: Road tax exempted for cars up to ₹30 lakh; ₹50,000 subsidies for EV buyers 9 shares may enter AMFI largecap list: BSE, Vodafone Idea, Groww, BHEL among probables

9 shares may enter AMFI largecap list: BSE, Vodafone Idea, Groww, BHEL among probables Qatar Emir’s $500 million superyacht Al Lusail returns after luxury refit worth $35 million

Qatar Emir’s $500 million superyacht Al Lusail returns after luxury refit worth $35 million GIFT Nifty logs record open interest, contracts on June 25

GIFT Nifty logs record open interest, contracts on June 25 Delhi Unveils ₹15,000 Crore EV Policy: What It Means For Auto Companies And Consumers

Delhi Unveils ₹15,000 Crore EV Policy: What It Means For Auto Companies And Consumers Gold, Silver Or Crude? Where Should Investors Bet Now? | Vandana Bharti

Gold, Silver Or Crude? Where Should Investors Bet Now? | Vandana Bharti How India Strategically Managed LPG & Crude Oil Supplies During West Asia War | K. Surana Explains

How India Strategically Managed LPG & Crude Oil Supplies During West Asia War | K. Surana Explains Delhi’s Green Revolution: CM Rekha Gupta Unveils Massive ₹15,000 Crore EV Policy To Combat Pollution

Delhi’s Green Revolution: CM Rekha Gupta Unveils Massive ₹15,000 Crore EV Policy To Combat Pollution Why Crude Oil Prices Could Stay Under Pressure As China's Demand Weakens And Supply Improves

Why Crude Oil Prices Could Stay Under Pressure As China's Demand Weakens And Supply Improves Why Jio BlackRock feels hybrid long-short is the perfect fund to launch now as it enters the SIF space

Why Jio BlackRock feels hybrid long-short is the perfect fund to launch now as it enters the SIF space Where should investors put their money? PL Wealth CEO has some tips

Where should investors put their money? PL Wealth CEO has some tips  Axis Bank CFO Puneet Sharma steps down; stock likely in focus on Tuesday

Axis Bank CFO Puneet Sharma steps down; stock likely in focus on Tuesday Apollo Hospitals, Medanta, Healthcare Global, Max Healthcare, Artemis Medicare: Check target prices, outlook

Apollo Hospitals, Medanta, Healthcare Global, Max Healthcare, Artemis Medicare: Check target prices, outlook Polycab: Amid record FII buying, shares at all-time high but brokerages expect more upside

Polycab: Amid record FII buying, shares at all-time high but brokerages expect more upside