For individual taxpayers, whether salaried employees, self-employed professionals, or investors, this evolving approach implies greater continuity and predictability. Rather than headline-grabbing rate changes, Budget 2026 is expected to prioritise stability in personal taxation, reducing uncertainty and minimising surprises on the direct tax front.

“The Union Budget remains a key policy instrument influencing individual tax outflows, disposable income, and household financial decisions, particularly as a growing share of the population is brought within the formal tax net,” said CA (Dr.) Suresh Surana.

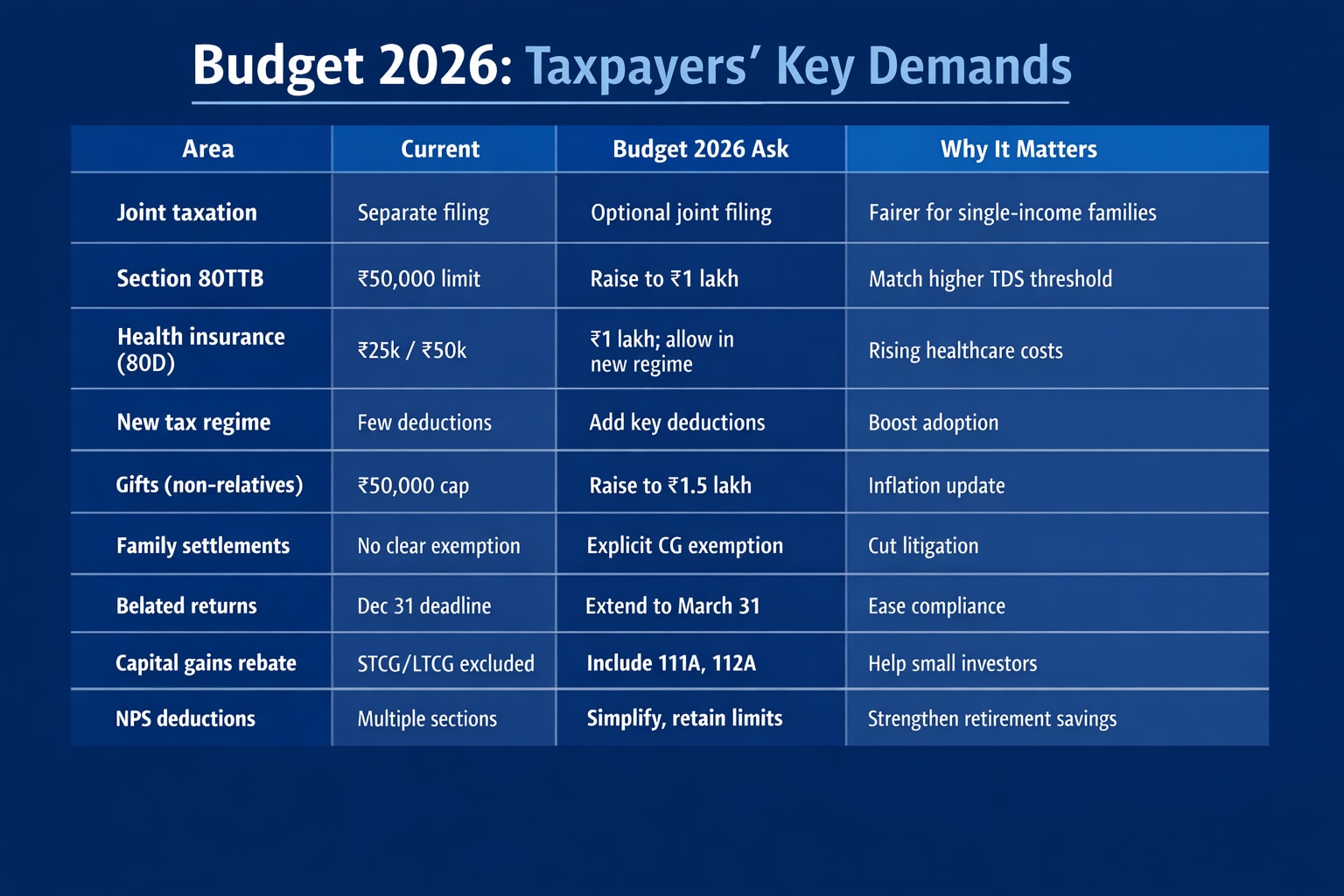

Surana shared a wishlist outlining some of the key expectations on the personal tax front from Budget 2026, as follows:

Joint taxation framework for married couples

Under the existing income-tax framework, India follows an individual-based system of taxation, under which each spouse is assessed separately, irrespective of marital status or the pooling of household resources. While this approach ensures individual tax accountability, it does not fully reflect the economic realities of married households, where income, savings, and expenditure decisions are often made jointly.

Several developed and emerging economies permit some form of joint or family-based taxation, recognising the household as an economic unit and providing flexibility to married couples in structuring their tax affairs. In contrast, the absence of an optional joint taxation framework in India may result in inequities, particularly in single-income or uneven-income households, where the higher-earning spouse bears a disproportionately higher tax burden.

The introduction of an optional joint taxation mechanism would recognise household-level economic realities and support families in managing tax liabilities more efficiently, while preserving individual choice within the tax system. Such a framework may allow for aggregation or partial pooling of income for rate or rebate purposes.

Accordingly, it is suggested that an optional joint taxation regime be introduced for married couples, allowing spouses to elect joint filing of tax returns while retaining the existing system of separate taxation as the default.

TDS thresholds for seniors

Section 80TTB provides senior citizens with a higher deduction of up to Rs 50,000 in respect of interest income from deposits. The government has extended additional relief to senior citizens by enhancing the threshold for non-deduction of tax at source on interest income under Section 194A (corresponding to Section 393(1), Table S. No. 5(ii) of the ITA, 2025) to Rs 1,00,000, following amendments introduced by the Finance Act, 2025.

However, the deduction limit under Section 80TTB has not been aligned with this policy approach, leading to a continued tax incidence and compliance burden for senior citizens.

In view of the enhanced threshold for non-deduction of tax at source, it would be appropriate to align the deduction limit under Section 80TTB by enhancing it to Rs 1,00,000 to provide meaningful relief to senior citizens.

Threshold limit for Section 80D

Section 80D (corresponding to Section 126 in the ITA, 2025) of the Income-tax Act provides a deduction for premiums paid by an individual in respect of medical insurance or contributions to the Central Government Health Scheme or any other notified scheme for self, spouse, dependent children, or parents. Further, under the current law, senior citizens above the age of 60 years who are not covered by health insurance are allowed a deduction of up to ₹50,000 towards actual medical expenditure.

As the scope of such expenditure is currently restricted only to senior citizens, it is recommended that this benefit be expanded to other individuals as well. Further, the quantum of deduction under this section should be revised upwards to ₹1,00,000, considering inflationary pressures and rising healthcare costs. It is also expected that the benefit under Section 80D be allowed under the new tax regime.

Threshold limit for gifts

Under Section 56(2)(x) (corresponding to Section 92(2)(m) of the ITA, 2025), if any person receives property without consideration, or for consideration that is less than the fair market value by an amount exceeding ₹50,000, the difference is taxable as ‘Income from Other Sources’.

The existing threshold of ₹50,000 was last revised in Budget 2006 (earlier covered under Section 56(2)(vi)). Considering inflation and the increased cost of living, it is suggested that this threshold be enhanced to ₹1,50,000.

Family settlement

Under the provisions of the Income-tax Act, capital gains tax is attracted on transactions involving the transfer of a capital asset. Section 47 (corresponding to Section 70 of the ITA, 2025) exempts certain transactions from being regarded as transfers and, therefore, from capital gains tax.

Capital assets are often received by specified individuals as part of family settlements. While Section 56(2)(x) provides that transfers of assets between specified relatives are not treated as income, and judicial precedents have consistently held that family settlements do not attract capital gains tax, Section 47 does not explicitly provide such an exemption.

To reduce litigation and provide clarity, it is recommended that Section 47 explicitly include family settlements among relatives so as to exempt them from the ambit of ‘transfer’ for capital gains purposes.

Belated tax return

The existing due date for filing a belated return is December 31 of the relevant assessment year. For instance, the belated return for FY 2025–26 can be filed by December 31, 2026. Filing a belated return attracts a late fee of ₹5,000, restricted to ₹1,000 where the total income does not exceed ₹5 lakh.

Extending this due date would provide taxpayers with additional time to fulfil their filing obligations, potentially improving compliance as individuals are more likely to file returns when given adequate time to collate information. A more lenient timeline encourages voluntary compliance rather than a punitive approach.

However, while extending the due date has advantages, a balance must be maintained between taxpayer convenience and administrative efficiency. Accordingly, it is suggested that the due date for filing belated returns be extended to the end of the relevant assessment year, i.e., March 31.

Rebate benefit

Certain categories of capital gains are taxed at special rates, including short-term capital gains on equity shares and equity-oriented mutual funds under Section 111A (corresponding to Section 196 of the ITA, 2025) and long-term capital gains under Section 112A (corresponding to Section 198 of the ITA, 2025).

Currently, the rebate under Section 87A is restricted to income taxed at normal slab rates and does not extend to income chargeable at these special rates. As a result, taxpayers whose income largely comprises equity-linked capital gains may not fully benefit from the rebate, even if their total income remains within the effective “no-tax” threshold.

While the Finance Act, 2025, raised the effective tax-free threshold to ₹12 lakh, the exclusion of Sections 111A and 112A from rebate eligibility dilutes the intended relief for small and retail investors.

Accordingly, it is suggested that the rebate under Section 87A be extended to include tax payable on income chargeable under Sections 111A and 112A, at least up to the specified income threshold.

The Economic Survey highlights a steady shift in India’s tax mix, with direct taxes now contributing nearly 59% of total tax revenues, up from about 52% before the pandemic.

The Economic Survey highlights a steady shift in India’s tax mix, with direct taxes now contributing nearly 59% of total tax revenues, up from about 52% before the pandemic. 'Every great airline is built over decades': Tata Sons Chairman says Air India's turnaround is a 5-10 yr mission

'Every great airline is built over decades': Tata Sons Chairman says Air India's turnaround is a 5-10 yr mission  Tata Motors flags ‘severe disruption’ at Sanand plant in Gujarat due to floods

Tata Motors flags ‘severe disruption’ at Sanand plant in Gujarat due to floods for garnering deposits in 2017 and 2021.") HDFC Bank penalises top officials, including CEO and CFO, in MSRDC case. Here’s why

HDFC Bank penalises top officials, including CEO and CFO, in MSRDC case. Here’s why Only 26 of every 100 young Indian graduates have salaried jobs; just 4 enjoy basic employment benefits: Report

Only 26 of every 100 young Indian graduates have salaried jobs; just 4 enjoy basic employment benefits: Report Where are the jobs: Youth unemployment remains high; fewer jobs for those with higher education in India

Where are the jobs: Youth unemployment remains high; fewer jobs for those with higher education in India DCB Bank Management | Q1 Earnings, Loan Growth, Margins & Asset Quality Explained

DCB Bank Management | Q1 Earnings, Loan Growth, Margins & Asset Quality Explained Infosys Fined In France: 70-Hour Work-week Debate Returns After €175,000 Labour Penalty

Infosys Fined In France: 70-Hour Work-week Debate Returns After €175,000 Labour Penalty I.T. Sector Outlook: Is the Worst Over for Indian I.T. Stocks After Long Underperformance?

I.T. Sector Outlook: Is the Worst Over for Indian I.T. Stocks After Long Underperformance? France And Spain Wildfires Threaten Cap Ferret Mansions And Bordeaux Wine Country

France And Spain Wildfires Threaten Cap Ferret Mansions And Bordeaux Wine Country Maruti Suzuki Eyes 25-30% SUV Growth, Says CNG Demand Has Overtaken Diesel

Maruti Suzuki Eyes 25-30% SUV Growth, Says CNG Demand Has Overtaken Diesel Tata Power Q1 profit rises 11% to Rs 1,176 crore; revenue up 6%, capex tops Rs 5,300 crore

Tata Power Q1 profit rises 11% to Rs 1,176 crore; revenue up 6%, capex tops Rs 5,300 crore HDFC Bank concludes internal review into MSRDC deposit arrangements; CEO, CFO among 3 fined Rs 1 lakh

HDFC Bank concludes internal review into MSRDC deposit arrangements; CEO, CFO among 3 fined Rs 1 lakh How Narayana Murthy's era, Vishal Sikka's stint and Salil Parekh's tenure differed; big task awaits next Infosys CEO

How Narayana Murthy's era, Vishal Sikka's stint and Salil Parekh's tenure differed; big task awaits next Infosys CEO BEL Q1 results: Net profit rises 9%, revenue at Rs 5,533 crore

BEL Q1 results: Net profit rises 9%, revenue at Rs 5,533 crore  Sensex, Nifty snap five-session losing run; investors add Rs 5.1 lakh crore in wealth

Sensex, Nifty snap five-session losing run; investors add Rs 5.1 lakh crore in wealth India's Vande Bharat sleeper gets a luxury upgrade: First look inside the redesigned first AC coach

India's Vande Bharat sleeper gets a luxury upgrade: First look inside the redesigned first AC coach Brazil aced the ethanol journey. Here's why it shows consumer trust matters most

Brazil aced the ethanol journey. Here's why it shows consumer trust matters most Beyond Strait of Hormuz & Red Sea: This Asian waterway is the world's most critical trade chokepoint

Beyond Strait of Hormuz & Red Sea: This Asian waterway is the world's most critical trade chokepoint AI could become the next financial shock: IMF tells central banks to prepare before crisis hits

AI could become the next financial shock: IMF tells central banks to prepare before crisis hits Women now own ₹18 lakh crore in mutual funds. What's driving India's investing boom?

Women now own ₹18 lakh crore in mutual funds. What's driving India's investing boom?