Two big insurance initial public offers, or IPOs, hit the markets recently. Both left investors puzzled, as while Price to Earnings multiples and Profit After Tax are good indicators of a companys financial position, things are not so simple when it comes to a life insurance company in India. There are two reasons for this. One, before these two, there were no listed insurers in India, and so relative valuation was not possible. Two, the valuation of a life insurance business is not based on just the present value of the company but also on the future value of its business. Both quantitative and qualitative factors come into play while analysing a life insurer, right from persistency ratio (total business a company is able to retain in a year) to distribution network.

The good news is that ICICI Prudential Life and SBI Life have got listed, setting a precedence for valuation of life insurers such as HDFC Life. More insurers are expected to line up for public offerings over the next couple of years.

Before looking at the companies numbers, it is important to understand that the life insurance business has different metrics than what people generally use for companies in manufacturing and services. It is a unique business because of its long payback period. In the initial years, insurers put in a lot of capital on expansion and covering underwriting risks. There are losses in initial years as strain on new policies wipes out profits from old policies. It is only when expenses shrink and the company stabilises that it achieves break even. Generally, it takes a life insurance company 8-10 years to break even. In India, a handful of insurers have started reporting profits, and that too only recently. The industry was opened to private players in 2000. Anuj Mathur, Chief Executive Officer of Canara HSBC OBC Life, says, "If you have accumulated losses, you have to wipe off those losses. In our case, we have been having a discrete profit for five years but still have accumulated losses. It will take time to wipe off losses in the first three-four years. You are in a position to pay dividend once the accumulated losses are wiped off." Lets take a look at the parameters one should consider before investing in life insurance companies.

Embedded Value (EV)

Embedded value is equivalent of book value in other sectors. It is defined as net asset value or networth plus the present value of potential future profits. In simple words, it calculates the present value of future profits from "existing policies", assuming the company stops writing business today. It reflects assets today and value of policies today.

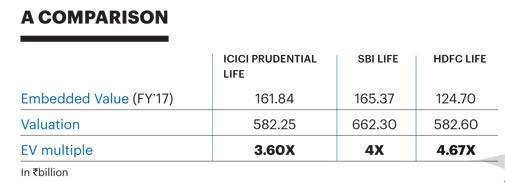

Future profits are determined on the basis of various parameters ranging from persistency, mortality and morbidity rates. External factors such as stock markets and interest rates also play a role in determining the value of the future business. The embedded value of ICICI Life is `16,184 crore (2016/17). SBI Life was valued at `16,537 crore as of March 31, 2017. HDFC Life, to be listed, has an EV of `12,470 crore.

Value of New Business (VNB)

VNB is defined as the present value of all future profits measured in the year in which the business is written based on long-term assumptions. It is calculated based on various factors, including product mix, product margin and persistency ratio.

a) Product mix

In India, 98 per cent premium goes into savings and investment products. Only 2 per cent goes into protection plans. The truth is that there is a lot of value creation in protection plans. Insurers are being assigned high valuation in hope that the companies will get a lot more exposure to protection plans in future considering that insurance penetration in the country is low. However, belying this notion, insurance penetration went down from 4 per cent of GDP in 201x/1y to 2.7 per cent of GDP in 201x/1y.

b) Product Margin

While valuing an insurance company, the mix of traditional and unit-linked plans, or Ulips, is also looked at. Ulip margins are lower because return on yield is fixed. In traditional plans, there is no restriction, making them more profitable. One also needs to look at what kind of business the insurer is writing. If the company is writing regular premium business, there is a multiple to that, because the customer has been locked in for 20-30 years. If it is primarily into single premium policies, then the multiples are low.

c) Persistency Ratio

Persistency ratio shows the percentage of policyholders paying renewal premiums at the end of a period. According to the Insurance Regulator and Development Authority of India, renewal premium accounted for 62.16 per cent (65.46 per cent in 2014/15) premium received in 2015/16. "If persistency is poor, it means your book is not healthy," says Mathur.

VNB Margin

VNB margin is the ratio of VNB for the period to annual premium equivalent (APE) for the period. It is similar to profit margin for any other business. Annual premium equivalent is the sum of the annual value of all regular premium contracts written in that year and 10 per cent of the total amount of single premium contracts written during the year. ICICI Prudential Life VNB margins were 10 per cent with VNB at `666 crore and APE at `6,625 crore for 2016/17. Similarly, for SBI Life, VNB was `1,036 crore and VNB margin as a percentage of APE was 15.4 per cent for 2016/17. HDFC Life has a VNB of `920 crore and VNB margin of 22 per cent.

EV Multiple

This is calculated by dividing the embedded value with market capital. The two life insurers that have been listed have EV multiples in the range of 3.5X-4X.

Prashant Tripathy, Senior Director & CFO, Max Life Insurance, says, "In developed markets, where insurance penetration is high, the multiple is usually in the range of 1-1.5X. In Asia, the range is 1.5-2.5X. For companies based in China, it is 1-2X." The reasons for these differences are potential and the stage of development of the insurance market. However, in case of India, the current valuations of strong insurance players are in the range of 3-4X, predominantly because the market is nascent and insurance penetration is significantly lower compared to developed markets".

R.M. Vishakha, Managing Director and Chief Executive Officer, IndiaFirst Life Insurance Company, agrees. "The multiples are a factor of the insurance markets potential and ability to realise that potential. Under current circumstances, the multiples seem to be a fair reflection of future growth potential."

Key Points

Insurers abroad calculate the value based on existing embedded value. But in India, a major portion of the value is coming from future business.

Shashwat Sharma, partner and head of insurance, KPMG India, says, "In India the listed life insurance companies have approximately 25 per cent of the overall valuation from embedded value, while in mature markets almost all of comes from this. This means capitalising on future potential and the ability of the insurer to expand into the higher margin protection businesses shall be the key to sustaining valuations."

Vishakha says, "Since unlocking of these profits will happen in the future, there is a belief that EV should be considered. This could be true at the current stage of business that the companies are at. Discounted cash flow can be used but it will need the market to be more mature to have a reasonable prediction of cash flows."

Remember that the valuation of a life insurance company is based on both existing and future value (where assumptions play a key role).