Come March and there will be a flurry of new fund offers from asset management companies in the country. Most of them will not be for regular equity-oriented mutual funds but what are called fixed maturity plans or FMPs -- close-ended debt schemes whose money is invested in fixed-income securities for a specific tenure.

"Coupon rates are going up and, hence, FMPs have become attractive. Debt yields have also been going up. On the other hand, fixed deposit rates are not likely to move up until the Reserve Bank of India increases the rates. The only way to benefit from these rising yields is by investing in debt funds. The AA papers can earn up to 100 bps (1 per cent) more than government securities," says Vidya Bala, Head of Mutual Funds Research at FundsIndia.

Axis Mutual Fund, Aditya Birla Sun Life Mutual Fund, Invesco Mutual Fund, Reliance Mutual Fund, SBI Funds, Sundaram Mutual Fund are all offering FMPs with durations ranging from 1,159 days to 1,386 days. If you think the duration is inspired by numerology, you are mistaken. By launching FMPs towards the fag end of the financial year, fund houses help investors claim inflation indexation benefit for four years - 2017/18, 2018/19, 2019/20 and 2020/21. The investments would be held for a little more than three years between March 2018 and April 2020.

Rate Cycle

Returns from debt instruments that FMPs invest in depend on interest rates. While the market is anticipating at least one interest rate hike in the near future, which is the reason why bond yields are rising, experts are of the view that the increase will take some time. "I think the rate hike anticipation is far-fetched. Even if we don't say that the rates have bottomed out, we are seeing a flat cycle with very little upward move," says Lakshmi Iyer Chief Investment Officer (Debt) & Head Products at Kotak Mahindra Asset Management Company. To lock-in higher interest rates, one can consider FMPs and, thereby, avoid volatility between the two rate cycles.

Tax-efficient Structure

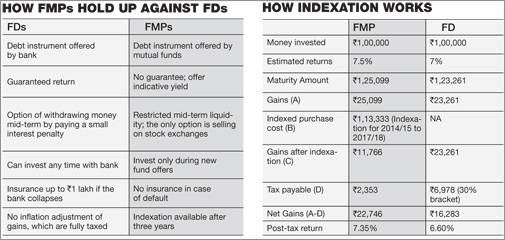

The biggest attraction of FMPs is inflation adjustment -- or indexation as it is called in technical terms -- of gains. Basically, the purchase price is adjusted with inflation, which reduces actual gains and, hence, lowers the tax burden. Returns from FMPs or debt mutual funds held for the long term (more than three years) are eligible for this. The returns from bank fixed deposits, on the other hand, are added to one's income and taxed as per the slab.

So, if you have invested `1 lakh in an FMP for three years and the same amount in a bank fixed deposit, then the math would work out as follows (see How Indexation Works). If you are in the highest tax bracket, you would earn `22,746 from an FMP after tax and `16,283 from a fixed deposit, thanks to the indexation benefit that FMPs are eligible for.

Bala explains. "FMPs are tax-efficient. If you invest `10 lakh each in a three-year FMP and a fixed deposit for the same period, the post-tax yield of fixed deposits for those in the 30 per cent tax bracket would be 5 per cent even if it is giving a 7 per cent return. However, even after paying 20 per cent tax post-indexation, a three-year FMP would give a 6.6 per cent return. The difference of 1.6 per cent is significant."

In essence, however, both FMPs and bank fixed deposits are debt investments that do not have an equity component. FMPs give 75-100 bps higher returns than deposits of equivalent tenures. But while a bank can assure you the amount it will pay at the end of the period, FMPs cannot guarantee any return. All they can provide is an indicative yield based on the current returns on debt instruments it invests in such as certificate of deposits, money market instruments, corporate bonds, commercial papers and bank fixed deposits.

The Risk Factor

FMP fund managers follow a buy-and-hold strategy. Though fund managers lock in their debt investments at the beginning, during the tenure, there is risk of corporate debt default, especially if the investments are not AA- or AAA-rated securities. One should take an informed call as a higher return could mean higher risk. "At present, most FMP portfolios are AAA," says Iyer. The yield on a five-year AAA-rated security is 7.8 per cent; for AA-rated instrument, it is slightly higher.

"FMPs are not a substitute for fixed deposits for those who are very risk averse as nobody is going to guarantee the returns," says Bala. Also, in FMPs, there is no option to take out cash prior to the maturity of the fund. Though FMPs are listed on exchanges, exiting them before maturity may be tough due to lack of liquidity. Or, one would have to sell at a deep discount. So, invest in FMPs only if you can hold till maturity.

For Senior Citizens

Starting financial year 2018/19, those in their silvers would get an additional `50,000 exemption for interest earned from fixed deposits and postal savings. So, instead of FMPs, they can consider other options. "Starting April 1, 2018, up to `50,000 interest earned by senior citizens will be tax exempt. So, we recommend that senior citizens exhaust their postal schemes and bank fixed deposit limits before locking funds in FMPs. The 7.75 per cent RBI bonds, although taxable, are still a good bet for senior citizens. Those looking for regular income can invest in ultra short-term debt funds and consider a systematic withdrawal plan," says Bala.