Nithin Kamath explained that the structure of STT itself creates an imbalance. STT on futures is levied on the entire contract value, while options are largely taxed on the premium amount.

Nithin Kamath explained that the structure of STT itself creates an imbalance. STT on futures is levied on the entire contract value, while options are largely taxed on the premium amount.  Nithin Kamath explained that the structure of STT itself creates an imbalance. STT on futures is levied on the entire contract value, while options are largely taxed on the premium amount.

Nithin Kamath explained that the structure of STT itself creates an imbalance. STT on futures is levied on the entire contract value, while options are largely taxed on the premium amount. Union Finance Minister Nirmala Sitharaman’s proposal to raise the Securities Transaction Tax (STT) on derivatives in the Union Budget 2026–27 has triggered sharp reactions across the market, with industry voices warning that the move could prove counterproductive if the government’s intent is to curb excessive speculation.

During her Budget speech on Sunday, Sitharaman announced that the STT on futures contracts would be increased to 0.05 per cent from 0.02 per cent, while STT on options premium and exercise of options would be raised to 0.15 per cent. The announcement unsettled stock markets and reignited a long-running debate on how best to regulate India’s booming derivatives segment.

Reacting to the proposal, Nithin Kamath, founder and chief executive of Zerodha, argued that higher STT rates may not meaningfully reduce speculative activity in futures and options (F&O), and could instead distort trading behaviour further in favour of options.

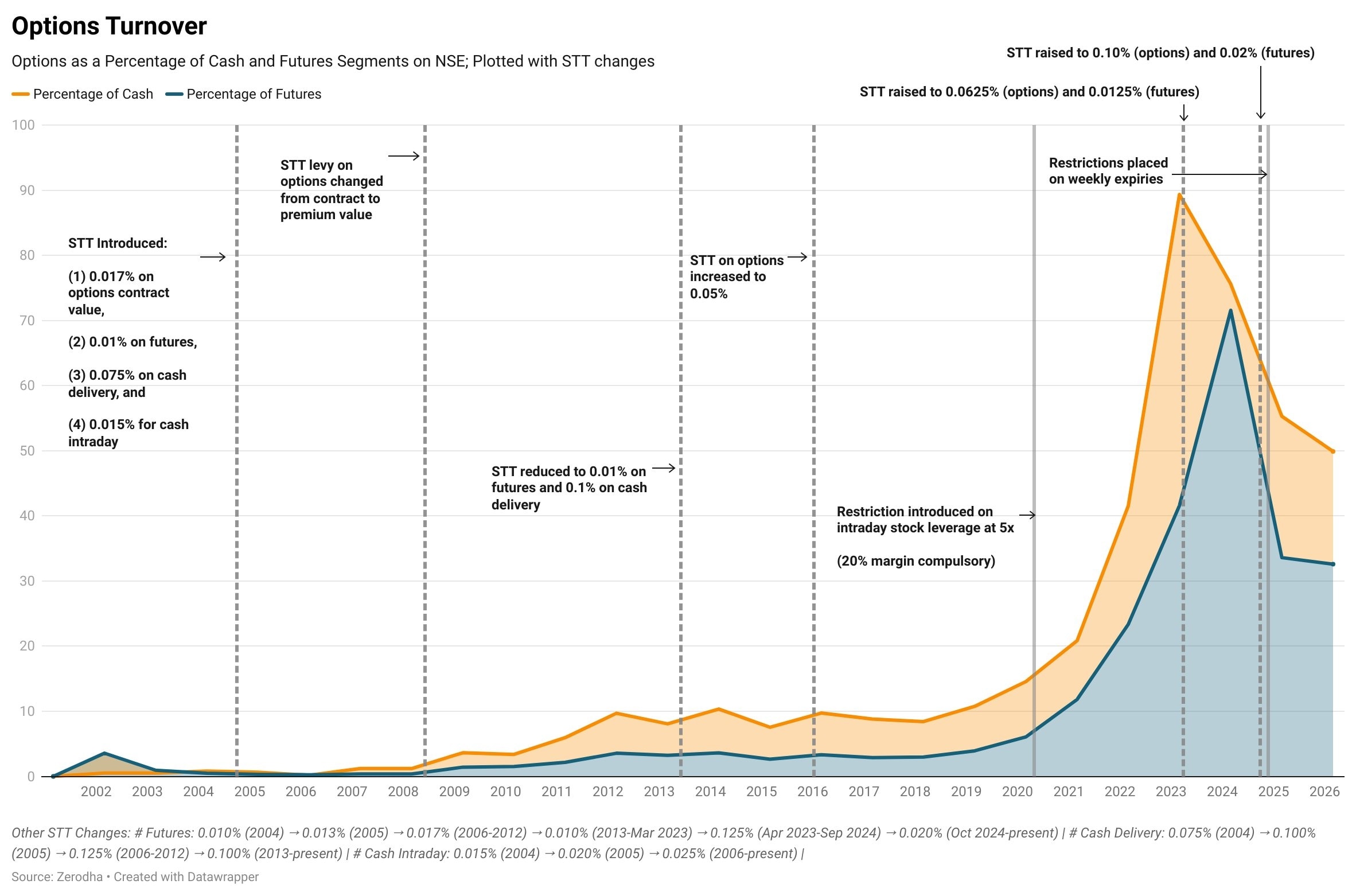

“I don’t know the exact reasoning behind the increase in STT. Having said that, if the goal was to reduce speculative activity in F&O, then I’m not sure this will do anything,” Kamath said. He pointed out that nearly 95 per cent of derivatives trading volumes are already concentrated in options, and the latest STT hike could push that share even higher.

Kamath explained that the structure of STT itself creates an imbalance. STT on futures is levied on the entire contract value, while options are largely taxed on the premium amount. As a result, any increase in STT disproportionately raises costs for futures trading, making them progressively less viable compared to options.

“Options are far more speculative than futures, but the impact of this STT hike falls mostly on futures,” Kamath said, adding that repeated increases in transaction taxes risk pushing traders toward products with higher leverage and risk.

He also flagged the uncertainty created by frequent and incremental STT changes. “The other problem with steady STT hikes is that at some point you start seeing a material impact on trading volumes because transaction costs make trading unviable. You’re already kind of seeing that with futures,” he said.

Case for alternative reforms

If the government’s objective is to rein in speculative excesses, Kamath suggested that product suitability norms -- defining who can trade complex derivatives—would be a more effective policy lever than repeatedly raising transaction taxes.

“I know it’s an unpopular opinion, but this will remove a lot of uncertainty among brokers and traders. It’s a much better approach than a death by a thousand STT hikes,” he said.

In earlier comments, Kamath has also argued that encouraging activity in cash equities and futures, rather than trying to suppress options trading, could lead to a healthier market structure. He said that lowering STT on cash and futures and increasing intraday leverage could naturally shift volumes away from excessively speculative options trades.

What the Budget proposed

Under the Union Budget 2026, Sitharaman announced a clear tightening of the STT regime for derivatives. “I propose to raise the STT on futures to 0.05 per cent from the present 0.02 per cent. STT on options premium and exercise of options are both proposed to be raised to 0.15 per cent,” she said in her speech.

As per the Finance Act, the revised STT rates will come into effect from April 1, 2026. Other STT rates remain unchanged.

The government has defended the move as necessary to cool down speculative excesses. In a post shared by the Income Tax Department, it noted that India’s total F&O trading volumes are now more than 500 times the country’s GDP. While India’s GDP is estimated at around Rs 300 lakh crore, the value of derivatives transactions has crossed Rs 1.5 lakh lakh crore, underscoring the scale of speculative activity.

Whether higher STT alone can temper this surge, however, remains a point of contention among market participants.

Centre to launch new series WPI, producer price indices on June 15

Centre to launch new series WPI, producer price indices on June 15 Oyo parent Prism gets Sebi nod for ₹6,650-cr IPO; eyes $7-8 bn valuation

Oyo parent Prism gets Sebi nod for ₹6,650-cr IPO; eyes $7-8 bn valuation Mother Dairy expects 5% growth in FY27; eyes expansion beyond Delhi-NCR

Mother Dairy expects 5% growth in FY27; eyes expansion beyond Delhi-NCR, Wipro and Tech Mahindra have seen renewed buying interest.") IT stocks stage a comeback: Five factors supporting the strong upmove

IT stocks stage a comeback: Five factors supporting the strong upmove ‘This is an incredible time to be a…’: Nvidia CEO Jensen Huang said on ‘SaaSpocalypse’

‘This is an incredible time to be a…’: Nvidia CEO Jensen Huang said on ‘SaaSpocalypse’ From Global Uncertainty To India's Opportunity: The Big Economic Outlook

From Global Uncertainty To India's Opportunity: The Big Economic Outlook Godrej Industries Is Entering The Wealth Management Space As It Looks To Scale Up Financial Services

Godrej Industries Is Entering The Wealth Management Space As It Looks To Scale Up Financial Services SIP Vs SWP: The Two-Step Mutual Fund Strategy That Could Help Become A Millionaire & Retire Early?

SIP Vs SWP: The Two-Step Mutual Fund Strategy That Could Help Become A Millionaire & Retire Early? Daily Calls LIVE: Ask Your STOCK MARKET TODAY QUERIES | Market Update LIVE | Share Market News Today

Daily Calls LIVE: Ask Your STOCK MARKET TODAY QUERIES | Market Update LIVE | Share Market News Today Retired At 39! How Sanjay Kathuria Turned A ₹2,000 SIP Into Complete Financial Freedom

Retired At 39! How Sanjay Kathuria Turned A ₹2,000 SIP Into Complete Financial Freedom Tata Tech, Bharti Airtel, PFC, BLS International shares: Should you enter at current levels?Oyo parent Prism gets Sebi nod for ₹6,650-cr IPO; eyes $7-8 bn valuation

Tata Tech, Bharti Airtel, PFC, BLS International shares: Should you enter at current levels?Oyo parent Prism gets Sebi nod for ₹6,650-cr IPO; eyes $7-8 bn valuation Rs 75/share dividend by Tata Group stock – Record date next week IT stocks stage a comeback: Five factors supporting the strong upmove

Rs 75/share dividend by Tata Group stock – Record date next week IT stocks stage a comeback: Five factors supporting the strong upmove CMR Green Technologies IPO: GMP zooms 130% in a week; should you subscribe?

CMR Green Technologies IPO: GMP zooms 130% in a week; should you subscribe?