Jefferies said Pakistan can be a profitable stock market to trade around IMF bailout cycles.

Jefferies said Pakistan can be a profitable stock market to trade around IMF bailout cycles. Jefferies said Pakistan can be a profitable stock market to trade around IMF bailout cycles.

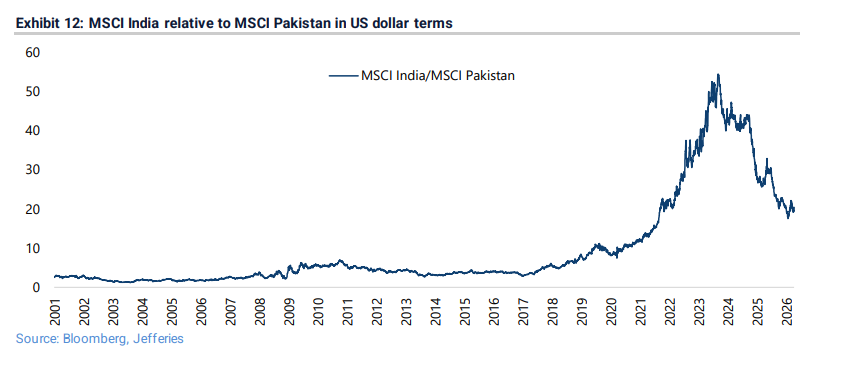

Jefferies said Pakistan can be a profitable stock market to trade around IMF bailout cycles.Christopher Wood of Jefferies in his latest GREED & fear note said Indian stock market has outperformed Pakistan shares by 653 per cent in dollar terms since the start of this century. This is even the MSCI Pakistan index is up 84 per cent in dollar terms since the last IMF programme in September 2024, a period in which it has outperformed the MSCI India by 124 per cent.

Wood's Jefferies is marginally 'Overweight' on India. It said Pakistan can also be a profitable stock market to trade around IMF bailout cycles.

Wood said the two-week Pakistan 'brokered' ceasefire is good news for an energy vulnerable India even though it must be galling, from a New Delhi perspective, "to see Pakistan achieve such a prominent profile on the world stage."

Wood said while Pakistan has been a bit of a macro-economic disaster for most of its existence since its independence in 1947, characterised by a lack of exports, recurring current account crises and numerous IMF programmes, it has genuine geopolitical significance because of its nuclear status and its large military.

"Pakistan is estimated to have a stockpile of about 170 nuclear warheads and approximately 660,000 active personnel in its armed forces. Meanwhile, it can also be a profitable stock market to trade around IMF bailout cycles," it said.

Wood said India will be a beneficiary, from a relative-return standpoint, if AI capex does peak this year given its status as the reverse AI trade and given that foreigners have already sold a lot of stocks, including a net $18.5 billion so far this year.

"Still that does not mean there is no downside risk. That risk is not only renewed conflict in Iran but also a sudden cessation in domestic mutual fund inflows," he said.

India valuations

Wood noted that the three months of 2026 were another quarter of disastrous underperformance for India in the sense that it was the worst performing market in Asia after Indonesia.

Still it is also the case that India has just about stopped under-performing since the onset of the Iran War in both an Asian and global emerging market context. Jefferies said.

"The MSCI India has underperformed both MSCI Emerging Markets and MSCI AC Asia Pacific ex-Japan by only 1.9 per cent in US dollar terms since the beginning of March, after underperforming by 16.2 per cent and 16 per cent respectively in the first two months of 2026,"

Wood said it is further the case that the de-rating in recent months, driven by aggressive foreign selling rather than any particularly negative newsflow, means that India’s traditional overvaluation has reduced significantly.

He said Nifty one-year forward PE now stands at 18.3 times after reaching 17 times at the end of March, which is close to the pre-Covid average of 16.8 times which prevailed between 2015 and 2020.

— the coaching institute acquired by Think & Learn in 2021.") Can Byju Raveendran still shape Byju's insolvency outcome?

Can Byju Raveendran still shape Byju's insolvency outcome? India to launch E85 fuel on World Environment Day

India to launch E85 fuel on World Environment Day Petrol, EV or Flex-Fuel? Here's which car makes most sense for your road trips in 2026

Petrol, EV or Flex-Fuel? Here's which car makes most sense for your road trips in 2026 Tomatoes push up Thali costs in May by 7% -- will onions and potatoes be next?

Tomatoes push up Thali costs in May by 7% -- will onions and potatoes be next? Can flex fuel cut your petrol bill? What the Brazil model shows us

Can flex fuel cut your petrol bill? What the Brazil model shows us Citi Sees Massive Upside In Power Stocks! ₹9.7 Lakh Crore Opportunity Ahead

Citi Sees Massive Upside In Power Stocks! ₹9.7 Lakh Crore Opportunity Ahead Midcap Winners Ahead? Siddhartha Khemka Reveals Top Themes For FY27

Midcap Winners Ahead? Siddhartha Khemka Reveals Top Themes For FY27 Govt's Big Move To Save The Rupee! Will Foreign Money Return To India?

Govt's Big Move To Save The Rupee! Will Foreign Money Return To India? Q4 Earnings Surprise! BFSI, Metals Shine As FY28 Recovery Takes Shape | Siddhartha Khemka

Q4 Earnings Surprise! BFSI, Metals Shine As FY28 Recovery Takes Shape | Siddhartha Khemka Reliance Down 17%: Is This the Best Time to Buy Before Jio Listing?

Reliance Down 17%: Is This the Best Time to Buy Before Jio Listing? 'Is this the biggest stock market scam ever? Move over, Harshad Mehta ...' — asks Sanjay Jha

'Is this the biggest stock market scam ever? Move over, Harshad Mehta ...' — asks Sanjay Jha Thangamayil Jewellery shares zoom 18% to hit record high; here's what investors should know

Thangamayil Jewellery shares zoom 18% to hit record high; here's what investors should know CG Power, Hitachi Energy India, GE Vernova shares rise up to 4% today; here's why

CG Power, Hitachi Energy India, GE Vernova shares rise up to 4% today; here's why  Bharat Forge sets record date for FY26 dividend payment; check details

Bharat Forge sets record date for FY26 dividend payment; check details Did you know? Rajesh Exports was one of the awardees of Rs 18,100 cr PLI scheme in 2022

Did you know? Rajesh Exports was one of the awardees of Rs 18,100 cr PLI scheme in 2022