With pan-India 5G rollout already complete, capex for both Bharti Airtel and Jio moderated in FY25, and FY26 guidance is likely to trend lower.

With pan-India 5G rollout already complete, capex for both Bharti Airtel and Jio moderated in FY25, and FY26 guidance is likely to trend lower.  With pan-India 5G rollout already complete, capex for both Bharti Airtel and Jio moderated in FY25, and FY26 guidance is likely to trend lower.

With pan-India 5G rollout already complete, capex for both Bharti Airtel and Jio moderated in FY25, and FY26 guidance is likely to trend lower. JM Financial in telecom sector note said the upcoming mega Jio Platforms IPO (initial public offer), targeted for the first half of 2026, has strengthened the case for a firmer tariff environment and sustained average revenue per user (ARPU) uptrend across the telecom sector. The brokerage expects FY25-28 ARPU to grow at about 12 per cent compounded annually, supported by the industry’s consolidated structure, the government’s preference for a 3+1 player market, and Jio’s own need to justify its heavy 5G capital spend ahead of the listing. This ARPU trajectory, it noted, should underpin 14-18 per cent Ebitda CAGR for telcom operators (telcos) over FY25-28.

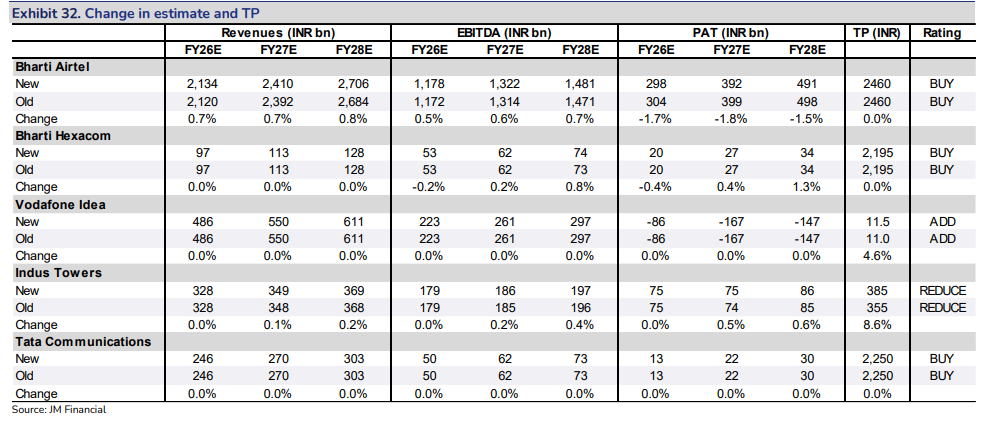

JM Financial has a target of Rs 2,460 for Bharti Airtel, Rs 2,195 for Bharti Hexacom, Rs 11 for Vodafone Idea (VIL), Rs 355 for Indus Towers and Rs 2,250 for Tata Communications.

With pan-India 5G rollout already complete, capex for both Bharti Airtel and Jio moderated in FY25, and FY26 guidance is likely to trend lower. JM Financial estimated Bharti’s India business free cash flow (FCF) to rise to about Rs 37,300 crore, Rs 41,600 crore and Rs 49,100 crore in FY26, FY27 and FY28, respectively, while Jio’s FCF may increase to roughly Rs 24,500 crore, Rs 33,700 crore and Rs 41,400 crore over the same period.

The brokerage reiterated a BUY rating on Bharti Airtel and Bharti Hexacom and maintained a positive stance on Jio. At its equity valuation of about $140 billion and enterprise value of $153 billion for Jio, the implied FY28 EV/Ebitda for Jio’s telecom business is around 12.4 times, similar to its implied multiple for Bharti’s India business, based on its EV estimate of around $150 billion.

According to the brokerage, the projected 12 per cent ARPU CAGR is likely to be driven by two key levers: a 6-7 per cent CAGR contribution from tariff hikes and a 5-6 per cent CAGR boost from ongoing premiumisation initiatives. These include migration of subscribers to 4G/5G, stronger post-paid additions, rising data consumption, regular plan restructuring that nudges users toward higher-priced packs, and gradual monetisation of 5G use-cases. International roaming and the removal of low-value plans are expected to support this trend.

The broking firm highlighted that ARPU in India, at roughly $2.4 per month, remains among the lowest globally versus the $8-10 global average. Its calculations suggest the industry requires ARPU to rise to Rs 270-300 by FY28 to earn pre-tax RoCE of 12-15 per cent, against sub-10 per cent currently, to justify recurring investments in spectrum and 5G rollouts.

JM Financial added that long-term ARPU growth would also be aided by a structural repair of the tariff architecture. As 5G penetration and data usage mature—penetration is already at about 45 per cent and monthly consumption has climbed to nearly 32GB—the industry may move away from the current one-size-fits-all tariff model towards a “pay-as-you-use” structure. This shift, it said, would allow telcos to charge heavier users more and reduce data allowances on lower-end plans, even if the scope for broad-based tariff hikes moderates over time. Airtel and Vodafone Idea have consistently argued for such a tariff overhaul.

The brokerage noted that visibility for a tariff hike of around 15 per cent over the next few months has improved, partly because of Jio’s IPO timeline and partly due to the government’s stance on maintaining a stable “3+1” industry configuration. The home broadband segment is also expected to bolster sector-wide Ebitda, aided by strong subscriber additions and aggressive fixed-wireless access rollouts, particularly by Jio, which commands approximately 75 per cent share in 5G FWA.

") 'India Inc functions like zamindars': Navam Capital MD after Uday Kotak's wake-up call warning

'India Inc functions like zamindars': Navam Capital MD after Uday Kotak's wake-up call warning India may cut bond taxes, ease investment rules to attract foreign capital: Report

India may cut bond taxes, ease investment rules to attract foreign capital: Report Will RBI raise interest rates at upcoming MPC meet? Here’s what SBI chief says

Will RBI raise interest rates at upcoming MPC meet? Here’s what SBI chief says ₹10,000-crore support for aviation fuel: Will airfares stabilise after govt help?

₹10,000-crore support for aviation fuel: Will airfares stabilise after govt help? BT Explainer: Planning a rooftop solar system? New rule from June 1 could increase costs by this amount

BT Explainer: Planning a rooftop solar system? New rule from June 1 could increase costs by this amount Section 301 Tariffs Could Hit Indian Exports Just As Trade Deal Nears Completion

Section 301 Tariffs Could Hit Indian Exports Just As Trade Deal Nears Completion Market Masters With Aniruddha Sarkar | Top Stock Ideas, Market Outlook & Investment Strategy

Market Masters With Aniruddha Sarkar | Top Stock Ideas, Market Outlook & Investment Strategy The Retirement Strategy: NPS, SWP, Mutual Funds, Insurance & Passive Income Explained

The Retirement Strategy: NPS, SWP, Mutual Funds, Insurance & Passive Income Explained What’s Hot: Stocks, Gold & Big Money Moves | Daily Market Show | Business Today TV

What’s Hot: Stocks, Gold & Big Money Moves | Daily Market Show | Business Today TV Maruti's Flex-Fuel Car Launch: Ethanol Industry On Fuel Pricing, Mileage & Demand

Maruti's Flex-Fuel Car Launch: Ethanol Industry On Fuel Pricing, Mileage & Demand CMR Green Technologies IPO subscribed 2.46 times on Day 1; check latest GMP, other key details

CMR Green Technologies IPO subscribed 2.46 times on Day 1; check latest GMP, other key details Ola share price surged 10% amid heavy volumes; key details

Ola share price surged 10% amid heavy volumes; key details BT Closing Bell | Sensex recovers 850 pts from day's low on report of tax cut on foreign bonds

BT Closing Bell | Sensex recovers 850 pts from day's low on report of tax cut on foreign bonds IndiGo, SpiceJet, Taneja Aerospace, other aviation stocks jump up to 5%; here's why

IndiGo, SpiceJet, Taneja Aerospace, other aviation stocks jump up to 5%; here's why Reliance Jio IPO in focus ahead of AGM: What YES Securities said on valuations, growth & more

Reliance Jio IPO in focus ahead of AGM: What YES Securities said on valuations, growth & more