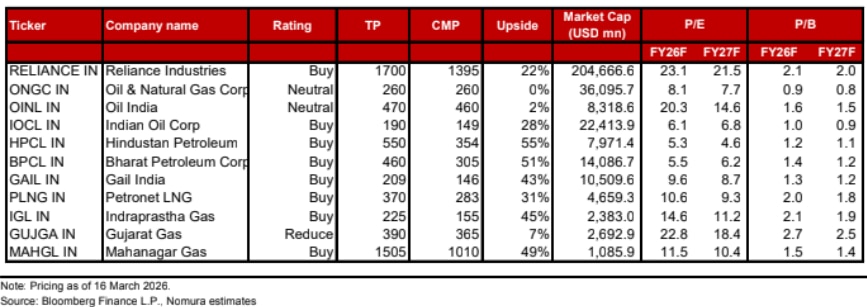

Nomura prefers GAIL due to its tariff-based business model with minimal margin impact from ongoing volatility in gas prices.

Nomura prefers GAIL due to its tariff-based business model with minimal margin impact from ongoing volatility in gas prices.Nomura on Thursday said refining is the best way to play the West Asia crisis, adding that Reliance Industries Ltd (RIL) is its top pick. The foreign brokerage said Indian refiners with a significantly higher exposure to diesel (50 per cent of output) should benefit materially from strong diesel cracks. GAIL (India) Ltd will be the least impacted among among gas players, the foreign brokerage said.

Nomura said RIL is the only refiner, in its coverage, that will likely benefit from increased refinery margins due to its insignificant fuel retailing footprint, which is less than 10 per cent of refinery throughput in terms of volume. Overall, Nomura estimated a 2.3 per cent increase in consolidated Ebitda for Reliance Industries for every $1 per barrel increase in refinery margins.

"Oil marketing companies (OMC), on the other hand, will likely lose much more on petrol and diesel retailing than the incremental benefit accrued on refining, in our view," it said.

Since the war broke in Iran, cracks for diesel and aviation turbine fuel (ATF) have surged to levels not seen before and are currently tracking at $76 per barrel and $107 per barrel against a normal run rate of $15-20 per barrel over the past several quarters.

This has been mainly driven by a combination of factors such as refinery rundowns due to crude shortages and damages owing to drone/missile attacks, West Asia oil product supplies not reaching end markets and China banning the export of refined products.

"We prefer GAIL due to its tariff-based business model with minimal margin impact (and 12% higher tariff from Jan 2026) from ongoing volatility in gas prices. We expect 20 per cent transmission volume impact on GAIL as lower imported LNG volume will likely be cushioned by a meaningful share of domestic gas volumes, which remain unaffected," Nomura said.

It said GAIL will also likely see some upside in the marketing segment and LPG production, as the government may allocate higher APM (Administered Price Mechanism) gas to counter LPG shortages.

On Petronet LNG, it said the company as an LNG importer may see meaningful volume impact (up to 40 per cent) from Qatar Energy declaring force majeure, though Ebitda margin may not correct due to a 5 per cent annual tariff escalation from January 2026," Nomura said.

"We think that if crude prices remain above $100 per barrel by the end of March, there is a strong case to bring back SAED (Special Additional Excise Duty) also called the windfall tax on domestic oil producers like

ONGC (ONGC IN, Neutral) and Oil India (OINL IN, Neutral)," it said.

Act.") Exam reforms: Tech titan Nandan Nilekani picked by PM Modi to fix national public examination system

Exam reforms: Tech titan Nandan Nilekani picked by PM Modi to fix national public examination system  'Tax officers struggled for own land': Nirmala Sitharaman slams laidback attitude of govt depts

'Tax officers struggled for own land': Nirmala Sitharaman slams laidback attitude of govt depts CBDT issues new crypto reporting guidance: No new tax, but exchanges must track and report all transactions

CBDT issues new crypto reporting guidance: No new tax, but exchanges must track and report all transactions Did Cockroach Janta Party's 'Chalo Sansad' 2.0 threat trigger Dharmendra Pradhan's resignation? What we know so far

Did Cockroach Janta Party's 'Chalo Sansad' 2.0 threat trigger Dharmendra Pradhan's resignation? What we know so far 'Will discharge my responsibilities with complete humility': Pralhad Joshi after being appointed Education Minister

'Will discharge my responsibilities with complete humility': Pralhad Joshi after being appointed Education Minister AI Data Centers, Aerospace & Gas Turbines: What's Powering Indo-MIM's Future Growth?

AI Data Centers, Aerospace & Gas Turbines: What's Powering Indo-MIM's Future Growth? Best Healthcare Stocks: Gaurang Shah's Outlook On Apollo Hospitals, Fortis & The Manipal Health IPO

Best Healthcare Stocks: Gaurang Shah's Outlook On Apollo Hospitals, Fortis & The Manipal Health IPO Is Indo-MIM's IPO Valuation Justified? Here's Why The Company Sees Strong Growth Ahead

Is Indo-MIM's IPO Valuation Justified? Here's Why The Company Sees Strong Growth Ahead Treasury Bills Explained: Why T-Bills Are One Of The Safest Short-Term Investment Options

Treasury Bills Explained: Why T-Bills Are One Of The Safest Short-Term Investment Options FDs vs Markets: Where Should You Keep Your Short-Term Money?

FDs vs Markets: Where Should You Keep Your Short-Term Money? Gland Pharma stock: Price target of Rs 3,250 likely in medium term, says analyst

Gland Pharma stock: Price target of Rs 3,250 likely in medium term, says analyst  Metal recycling stocks to buy: Gravita, Pondy Oxides, Jain Resource among top picks

Metal recycling stocks to buy: Gravita, Pondy Oxides, Jain Resource among top picks TRIL shares: Should you average the falling stock? Here's 'fixed and final' stop loss

TRIL shares: Should you average the falling stock? Here's 'fixed and final' stop loss Adani Power: 45 GW target, Rs 2 lakh crore capex plan among conference call highlights

Adani Power: 45 GW target, Rs 2 lakh crore capex plan among conference call highlights  ITC Hotels, Chalet, Ventive, IHCL, SAMHI: Hotel stocks to buy despite travel disruptions

ITC Hotels, Chalet, Ventive, IHCL, SAMHI: Hotel stocks to buy despite travel disruptions Beyond mutual funds: Why analysts see SBI Funds' alternative asset business as a long-term growth engine

Beyond mutual funds: Why analysts see SBI Funds' alternative asset business as a long-term growth engine 'Ashamed of it...': Manoj Muntashir calls Adipurush his biggest mistake, seeks country's forgiveness Exam reforms: Tech titan Nandan Nilekani picked by PM Modi to fix national public examination system 'Tax officers struggled for own land': Nirmala Sitharaman slams laidback attitude of govt depts

'Ashamed of it...': Manoj Muntashir calls Adipurush his biggest mistake, seeks country's forgiveness Exam reforms: Tech titan Nandan Nilekani picked by PM Modi to fix national public examination system 'Tax officers struggled for own land': Nirmala Sitharaman slams laidback attitude of govt depts and several prominent national institutes. (Representational photo)") Delhi targets traffic bottlenecks on Aruna Asaf Ali Marg with ₹1.97 crore elevated road study

Delhi targets traffic bottlenecks on Aruna Asaf Ali Marg with ₹1.97 crore elevated road study