Over the past decade, MF AUM climbed steadily from ₹21.3 lakh crore in 2017 to over ₹80 lakh crore by 2025.Over the past decade, MF AUM climbed steadily from ₹21.3 lakh crore in 2017 to over ₹80 lakh crore by 2025.

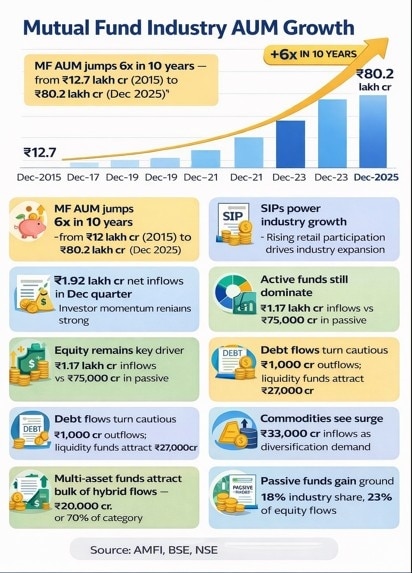

Over the past decade, MF AUM climbed steadily from ₹21.3 lakh crore in 2017 to over ₹80 lakh crore by 2025.Over the past decade, MF AUM climbed steadily from ₹21.3 lakh crore in 2017 to over ₹80 lakh crore by 2025.India’s mutual fund industry has expanded more than six-fold over the past decade, with assets under management (AUM) touching ₹80.23 lakh crore as of December 2025, underscoring a structural shift in household savings towards market-linked instruments, according to a Motilal Oswal Mutual Fund study.

The industry’s AUM has grown from about ₹12 lakh crore in December 2015 to over ₹80 lakh crore in December 2025, supported by rising retail participation, sustained SIP inflows, deeper digital penetration and greater investor awareness. December 2025 alone saw systematic investment plan (SIP) inflows of around ₹31,000 crore, highlighting the increasing role of disciplined investing in driving long-term growth.

Over the last 10 years, the industry has consistently scaled up, with AUM rising to ₹21.3 lakh crore in 2017, ₹26.5 lakh crore in 2019, ₹37.7 lakh crore in 2021 and ₹50.8 lakh crore in 2023, before crossing the ₹80 lakh crore mark in 2025. The expansion reflects broader participation across retail and institutional investors, regulatory support and the steady financialisation of household savings.

Where the money flowed in December quarter

Investor allocation trends during the quarter ended December 2025 point to a diversified, multi-asset approach. According to the “Where the Money Flows” report, the mutual fund industry recorded estimated net inflows of ₹1.92 lakh crore during the quarter.

Active funds accounted for ₹1.17 lakh crore of these inflows, while passive strategies attracted ₹75,000 crore, highlighting the continued dominance of active management even as passive investing gains ground. Equity funds remained the biggest contributor, with net inflows of ₹1.12 lakh crore.

Within equities, broad-based strategies dominated investor preferences, accounting for about 88% of active equity flows and nearly ₹98,000 crore in inflows. Large-cap passive funds, flexicap active funds and arbitrage strategies emerged as key beneficiaries, reflecting a mix of long-term allocation and tactical positioning.

Debt, commodities and hybrid trends

Debt funds, however, saw marginal pressure, with net outflows of around ₹1,000 crore during the quarter, reflecting caution amid uncertainty over the interest rate trajectory. That said, flows within the segment were mixed. Liquid funds attracted strong inflows of about ₹27,000 crore, largely driven by short-term parking of surplus funds, while constant maturity funds recorded inflows of ₹3,100 crore. Corporate bond funds also saw steady interest, supported by institutional participation.

On the other hand, target maturity funds and gilt funds witnessed outflows of approximately ₹3,200 crore and ₹2,000 crore, respectively, indicating selective repositioning by investors.

Commodity funds emerged as a key growth driver, recording net inflows of ₹33,000 crore during the quarter — a sharp 56% increase on a quarter-on-quarter basis. The surge reflects sustained investor interest in hard assets, both as an inflation hedge and a portfolio diversification tool, amid volatile equity and bond markets.

Hybrid funds continued to attract healthy allocations. Multi-asset funds accounted for nearly 70% of hybrid category inflows, with investments of about ₹20,000 crore. Balanced advantage funds and aggressive hybrid funds also recorded inflows of ₹3,100 crore and ₹3,900 crore, respectively, underscoring demand for dynamically managed asset allocation strategies.

Thematic and passive funds

Thematic mutual funds, however, faced net outflows during the quarter. Passive PSU funds led the decline with outflows of around ₹6,300 crore, while manufacturing and infrastructure themes together saw outflows of nearly ₹3,000 crore. In contrast, select themes such as defence, business cycle and consumption continued to attract investor interest, collectively garnering about ₹2,000 crore in inflows. The defence theme alone drew nearly ₹1,000 crore.

Passive funds continued their steady rise, accounting for roughly 18% of the industry’s overall market share. Within equities, passive large-cap funds captured a significant portion of flows, while debt passive products posted moderate growth. Commodity-based ETFs were a standout, with inflows of around ₹33,000 crore during the quarter.

A diversified investor approach

Overall, the December 2025 quarter reflects an increasingly diversified investor mindset. While equities remained the preferred asset class through broad-based and systematic approaches, the resurgence in commodity allocations points to a growing focus on inflation protection and diversification. Passive investing continues to gain traction, accounting for about 23% of equity flows, hough active strategies remain central to portfolios.

The data underscores a maturing mutual fund industry, where investors are spreading allocations across asset classes and strategies, aligned with long-term structural growth themes and evolving macroeconomic conditions.

Sarvam's Vivek Raghavan on why sovereign AI is no longer optional

Sarvam's Vivek Raghavan on why sovereign AI is no longer optional BT Explainer: Why the government has ended a key exemption for cough syrups

BT Explainer: Why the government has ended a key exemption for cough syrups RIL AGM ahead: Shareholders gain Rs 1 lakh cr in three days; analysts unveil price targets

RIL AGM ahead: Shareholders gain Rs 1 lakh cr in three days; analysts unveil price targets India expands global hunt for rare earth supplies, eyes Russia's Tomtor deposit

India expands global hunt for rare earth supplies, eyes Russia's Tomtor deposit") Here's why HCLTech is betting $150 million on Sarvam

Here's why HCLTech is betting $150 million on Sarvam Pharma Stocks Rally Far From Over? Expert Sees New Growth Era For Indian Drugmakers Amid Global Expansion

Pharma Stocks Rally Far From Over? Expert Sees New Growth Era For Indian Drugmakers Amid Global Expansion Banking Stocks Set For 15-20% Upside? Expert Sees Deep Value In These Private Banks

Banking Stocks Set For 15-20% Upside? Expert Sees Deep Value In These Private Banks Where Is India's Mutual Fund Money Going? Exclusive Analysis With Dhirendra Kumar

Where Is India's Mutual Fund Money Going? Exclusive Analysis With Dhirendra Kumar G7 Summit 2026: India Today Reports From Évian As World Leaders Gather

G7 Summit 2026: India Today Reports From Évian As World Leaders Gather India Macro Outlook: Oil Prices Ease, Rupee Stabilizes, But Inflation Risks Rise

India Macro Outlook: Oil Prices Ease, Rupee Stabilizes, But Inflation Risks Rise SpaceX shares jump over 8% in pre-market trading; details here

SpaceX shares jump over 8% in pre-market trading; details here ITC shares: Price targets for investors as stock trades near 52-week low

ITC shares: Price targets for investors as stock trades near 52-week low  Why are aluminium prices and metal stocks tumbling after easing of West Asia tensions?

Why are aluminium prices and metal stocks tumbling after easing of West Asia tensions? Sensex, Nifty extend winning run; investor wealth rises Rs 19.9 lakh crore in 3 sessions

Sensex, Nifty extend winning run; investor wealth rises Rs 19.9 lakh crore in 3 sessions Reliance shareholders alert for dividend! What RIL AGM 2026 notice says on payment

Reliance shareholders alert for dividend! What RIL AGM 2026 notice says on payment