A recent State Bank of India research report flagged the sharp rise in unsecured loans as a potential risk to the banking system. A recent State Bank of India research report flagged the sharp rise in unsecured loans as a potential risk to the banking system.

A recent State Bank of India research report flagged the sharp rise in unsecured loans as a potential risk to the banking system. A recent State Bank of India research report flagged the sharp rise in unsecured loans as a potential risk to the banking system. Unsecured loans, such as personal loans, credit card borrowing and some education loans, are credit facilities extended without collateral, based largely on the borrower’s income profile and credit history. While widely used for personal needs, they carry higher interest rates and, crucially, invite closer examination from tax officials if supporting paperwork is inadequate.

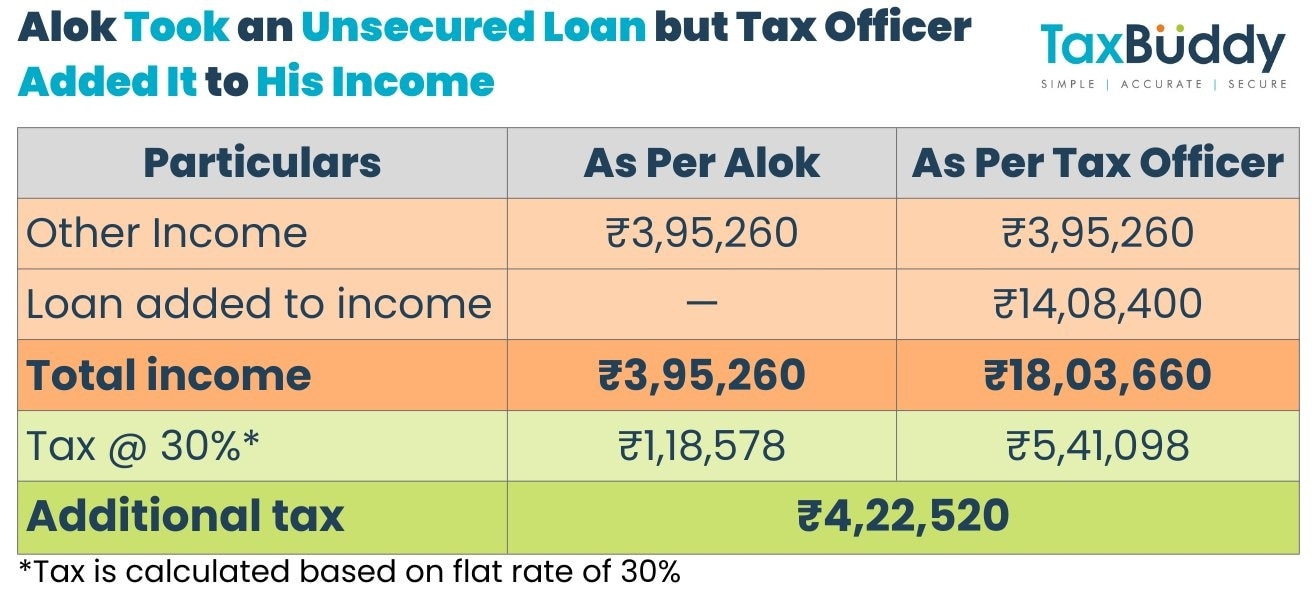

That risk played out starkly in the case of Alok, whose unsecured loan of Rs 14.08 lakh was treated as undisclosed income by a tax officer, resulting in a tax demand of Rs 4.57 lakh. The case, decoded by tax advisory platform TaxBuddy, highlights how gaps in documentation around unsecured borrowings can quickly escalate into major tax disputes—and how proper evidence can help taxpayers defend themselves.

Alok had filed his income tax return declaring a total income of Rs 3.95 lakh. During assessment proceedings, the tax officer scrutinised unsecured loans reflected in his accounts and questioned their genuineness. In the absence of immediate satisfaction on the nature of the borrowings, the officer added the entire unsecured loan amount of Rs 14.08 lakh to Alok’s income, raising his assessed income to ₹18.03 lakh.

The financial impact was significant. With the income pushed into the highest tax slab, Alok’s tax liability rose from about Rs 1.19 lakh to Rs 5.41 lakh, an additional burden of more than Rs 4.2 lakh — solely because the loan was treated as income rather than a liability.

TaxBuddy explained that unsecured loans often attract such additions because they are granted without collateral, making them easier for tax officers to challenge if paperwork is weak. In such cases, officers may argue that the funds represent unaccounted income rather than genuine borrowings.

However, Alok chose not to rely on arguments alone. Instead, he focused on evidence. He submitted loan confirmation letters from the lenders and furnished bank statements to establish a clear money trail showing that the funds were received as loans. These documents were critical in demonstrating the identity of the lenders and the genuineness of the transactions.

The matter eventually reached the income tax tribunal. In its observations, the tribunal noted that Alok had discharged his initial burden by producing basic documentary proof in support of the unsecured loans. Crucially, it pointed out that the tax department had failed to bring any material evidence to contradict the confirmations or the bank trail provided by the taxpayer.

The tribunal held that mere suspicion cannot replace proof, and once a taxpayer furnishes prima facie evidence, the onus shifts to the department to establish otherwise. On this basis, it ruled that the addition of ₹14.08 lakh was unjustified and directed its deletion, effectively quashing the additional tax demand.

The case comes at a time when unsecured lending is expanding rapidly in India. A recent State Bank of India research report flagged the sharp rise in unsecured loans as a potential risk to the banking system. According to the report, unsecured advances increased from ₹2 lakh crore in FY05 to ₹46.9 lakh crore in FY25, with their share in total bank advances rising to 24.5%. Public sector banks account for about half of this exposure.

For taxpayers, Alok’s case offers a clear takeaway: unsecured loans are legitimate, but only if backed by solid documentation. Loan confirmations, lender details and a transparent banking trail can make the difference between a routine assessment and a costly tax dispute.

Major relief! Price of 19 kg LPG cylinder cut by ₹183.50; check new rates

Major relief! Price of 19 kg LPG cylinder cut by ₹183.50; check new rates Anthropic’s Claude Fable 5, Mythos 5 global access cleared by US govt; Global rollout starts July 1

Anthropic’s Claude Fable 5, Mythos 5 global access cleared by US govt; Global rollout starts July 1 KPIT Technologies clarifies on H1 FY27 revenue outlook as stock slumps to 52-week low

KPIT Technologies clarifies on H1 FY27 revenue outlook as stock slumps to 52-week low Advit Jewels delivers 37% listing gains; Cordelia Cruise turns into a wealth destroyer

Advit Jewels delivers 37% listing gains; Cordelia Cruise turns into a wealth destroyer Agnikul, ICEYE tie up to explore sovereign satellite and launch system in India

Agnikul, ICEYE tie up to explore sovereign satellite and launch system in India Road Deaths In India: Nitin Gadkari Exposes The Deadly Impact Of Irresponsible Driving!

Road Deaths In India: Nitin Gadkari Exposes The Deadly Impact Of Irresponsible Driving! "Designed,Developed, & Manufactured In India": Rajnath Singh Calls For New Era Of Defence Excellence

"Designed,Developed, & Manufactured In India": Rajnath Singh Calls For New Era Of Defence Excellence Adani Ports Gets $1.4 Billion Boost As MSC Buys 49% Stake In Vizhinjam Port

Adani Ports Gets $1.4 Billion Boost As MSC Buys 49% Stake In Vizhinjam Port Oyo's Parent Company Files Updated DRHP To SEBI, Check Full Details Here

Oyo's Parent Company Files Updated DRHP To SEBI, Check Full Details Here Nifty Ends H1; Looks Ahead To Gains

Nifty Ends H1; Looks Ahead To Gains Ola shares extend gains as Q1 FY26 registrations nearly double; what analysts are saying

Ola shares extend gains as Q1 FY26 registrations nearly double; what analysts are saying Va Tech Wabag shares gain 6% on ‘Large’ order win in Austria

Va Tech Wabag shares gain 6% on ‘Large’ order win in Austria  Vedanta Iron shares rally over 62% in two weeks; company issues clarification on price movement

Vedanta Iron shares rally over 62% in two weeks; company issues clarification on price movement Knack Packaging IPO opens today: Should you subscribe? Check price band, latest GMP & moreKPIT Technologies clarifies on H1 FY27 revenue outlook as stock slumps to 52-week low

Knack Packaging IPO opens today: Should you subscribe? Check price band, latest GMP & moreKPIT Technologies clarifies on H1 FY27 revenue outlook as stock slumps to 52-week low