Physical gold, jewellery, coins and bars, and digital gold often appear safer and simpler, but can quietly erode returns.

Physical gold, jewellery, coins and bars, and digital gold often appear safer and simpler, but can quietly erode returns.For decades, Indian investors have turned to gold as a hedge against inflation and a safe haven during market turmoil. In recent years, the yellow metal has strengthened that reputation by delivering returns that have often outpaced traditional fixed-income instruments such as fixed deposits and bonds. Yet, while gold’s price performance has impressed, experts warn that taxation can make or break the real returns investors finally take home.

Abhijit Chokshi, a SEBI-registered research advisor, recently highlighted how the form in which gold is bought can sharply alter post-tax outcomes. Illustrating with a simple example, he said two investors could each put Rs 5 lakh into gold, yet one could walk away tax-free while the other could lose up to Rs 1.5 lakh purely due to how their investment was structured. “Most Indians lose up to 30% of their gold returns just in taxes. It’s not the price of gold that hurts you — it’s the form you bought it in,” Chokshi said.

Gold investment and taxes

As equity markets remain volatile and geopolitical risks rise, gold has regained importance in portfolios. But in FY2025–26, Chokshi argues, gold is no longer just a safe asset — it is a strategic one, where tax efficiency is as critical as price appreciation.

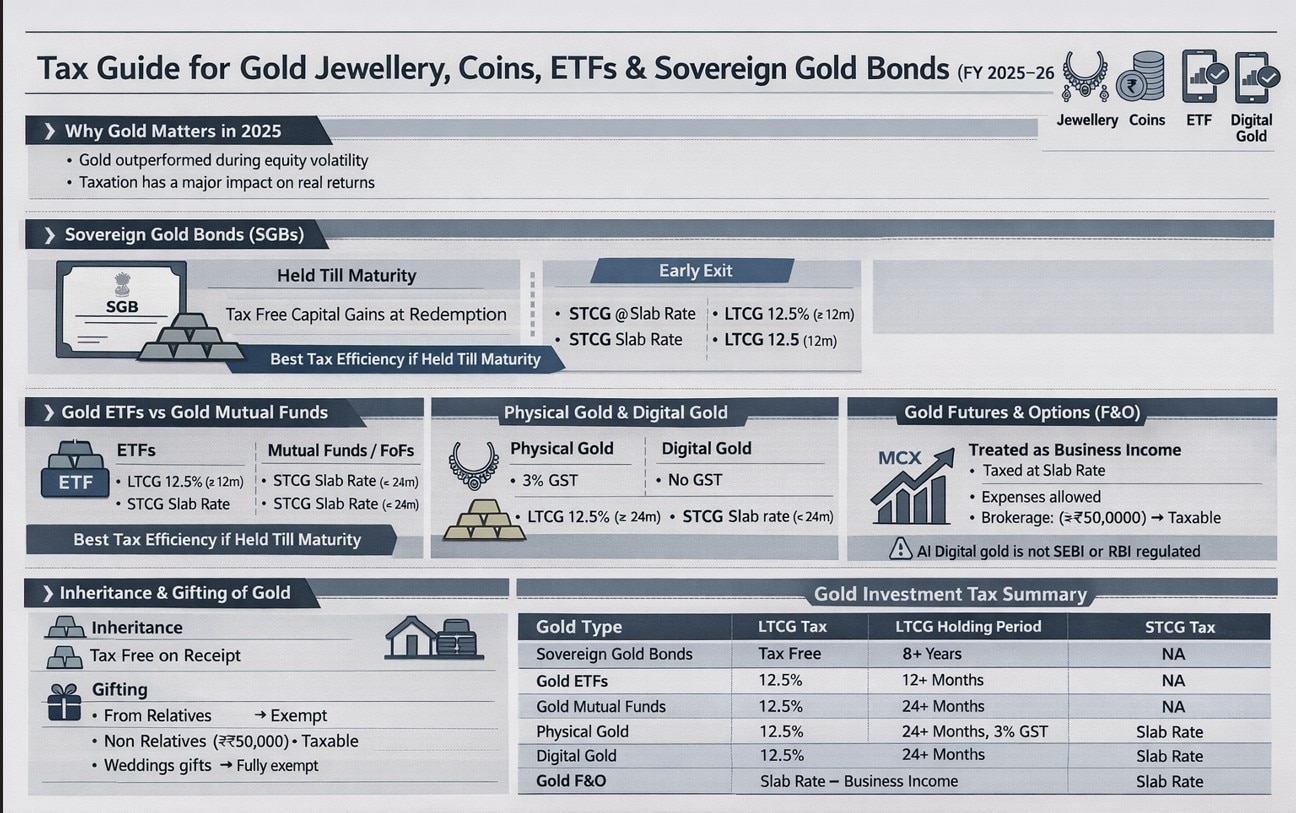

Among the various options, Sovereign Gold Bonds (SGBs) stand out as the most tax-efficient vehicle. While the annual 2.5% interest is taxed at the investor’s slab rate, capital gains at redemption after the eight-year maturity are completely tax-free. Selling SGBs before maturity attracts short-term capital gains tax if held under a year, and long-term capital gains tax of 12.5% without indexation if sold between one and eight years. For long-term investors, however, holding till maturity can make SGBs the most rewarding post-tax option.

Gold ETFs and gold mutual funds, though linked to the same underlying asset, follow different tax rules. Gold ETFs qualify for long-term capital gains after 12 months, taxed at 12.5% without indexation, while gold mutual funds require a 24-month holding period for the same treatment. Short-term gains in both cases are taxed at slab rates, making holding period strategy essential.

Physical gold — jewellery, coins and bars — and digital gold often appear safer and simpler, but can quietly erode returns. Physical gold attracts 3% GST at purchase, while digital gold also carries GST. Both are taxed at 12.5% on long-term gains after 24 months, without indexation, and at slab rates for shorter holdings. Over time, these costs can significantly reduce effective returns.

For traders, gold futures and options present another risk. These are taxed as business income, with no capital gains benefits, though expenses such as brokerage can be deducted. Chokshi cautions that digital gold is not regulated by SEBI or the RBI, urging investors to tread carefully.

Tax planning can also help investors preserve gains. Provisions such as Section 54F, which allows reinvestment of gains into residential property, and Section 54EC, which permits investment in REC or NHAI bonds, offer legitimate ways to reduce capital gains tax.

Gold prices on a high

The renewed interest in gold comes amid a fresh rally in precious metals. Gold and silver recently surged to record levels in Asian trade as geopolitical tensions flared after fresh signals of potential escalation in the Middle East. Spot gold rose to around $4,635 an ounce, while silver jumped past $90, reinforcing gold’s role as a hedge against political and economic uncertainty.

The takeaway for investors is clear: gold may be a single metal, but it is treated as multiple assets by the taxman. Choosing the wrong form can cut real returns by as much as 30–50%. Choosing wisely, especially through tax-efficient vehicles like SGBs, can turn gold into a powerful long-term wealth builder — not just a safe haven, but a smart one.

HDFC Bank Q1 results: Net profit rises 5% to Rs 19,060 crore; NII up 6.7%; key takeaways

HDFC Bank Q1 results: Net profit rises 5% to Rs 19,060 crore; NII up 6.7%; key takeaways 'A once-in-a-lifetime opportunity': Skyroot CEO Pawan Chandana's words capture the significance of Vikram-1's historic launch

'A once-in-a-lifetime opportunity': Skyroot CEO Pawan Chandana's words capture the significance of Vikram-1's historic launch ICICI Bank Q1 results: Net profit rises 15.9% to Rs 14,805 crore; asset quality stays stable

ICICI Bank Q1 results: Net profit rises 15.9% to Rs 14,805 crore; asset quality stays stable ratio improved 17 basis points sequentially to 2.78 per cent. It was down 100 basis points from 3.78 per cent in the year-ago quarter.") PNB Q1 net profit soars 214% to Rs 5,253 crore on lower provision for income tax

PNB Q1 net profit soars 214% to Rs 5,253 crore on lower provision for income tax Vikram-1 launch: India's first private orbital rocket enters space; joins US, China

Vikram-1 launch: India's first private orbital rocket enters space; joins US, China Trump Threatens Iran’s “Pickaxe Mountain”: Why This Nuclear-Linked Bunker Is Hard To Hit

Trump Threatens Iran’s “Pickaxe Mountain”: Why This Nuclear-Linked Bunker Is Hard To Hit India Launches SHANTI Campaign For 2028-29 UNSC Seat As EAM Jaishankar Makes Global Reform Pitch

India Launches SHANTI Campaign For 2028-29 UNSC Seat As EAM Jaishankar Makes Global Reform Pitch Will BJP Project Yogi Adityanath As Its U.P. CM Face For 2027? Speculation Grows

Will BJP Project Yogi Adityanath As Its U.P. CM Face For 2027? Speculation Grows Sneha Mordani Ground Report: Can New Rules Stop Misuse Of High-Alcohol Medicines?

Sneha Mordani Ground Report: Can New Rules Stop Misuse Of High-Alcohol Medicines? Why FIIs Aren't Returning To India Yet | Punita Kumar Explains The Real Challenges

Why FIIs Aren't Returning To India Yet | Punita Kumar Explains The Real Challenges RIL Q1 results: O2C recovery drives broadly in-line quarter, says Equirus Securities

RIL Q1 results: O2C recovery drives broadly in-line quarter, says Equirus Securities IDBI Bank Q1 results: Net profit rises 5% to Rs 2,115 crore; NIM falls 54 bps QoQ

IDBI Bank Q1 results: Net profit rises 5% to Rs 2,115 crore; NIM falls 54 bps QoQ  Adani Ports: Post 30% rally in six months, more upside likely for the Adani Group stock?HDFC Bank Q1 results: Net profit rises 5% to Rs 19,060 crore; NII up 6.7%; key takeawaysICICI Bank Q1 results: Net profit rises 15.9% to Rs 14,805 crore; asset quality stays stable

Adani Ports: Post 30% rally in six months, more upside likely for the Adani Group stock?HDFC Bank Q1 results: Net profit rises 5% to Rs 19,060 crore; NII up 6.7%; key takeawaysICICI Bank Q1 results: Net profit rises 15.9% to Rs 14,805 crore; asset quality stays stable