Residential activity remained buoyant through Q3 2025, with sales touching Rs 1.52 lakh crore.Residential activity remained buoyant through Q3 2025, with sales touching Rs 1.52 lakh crore.

Residential activity remained buoyant through Q3 2025, with sales touching Rs 1.52 lakh crore.Residential activity remained buoyant through Q3 2025, with sales touching Rs 1.52 lakh crore.India’s residential real estate market has outpaced equity markets with a robust 15% total return over the past year, driven primarily by infrastructure upgrades across major cities. According to new data from the 1 Finance Housing Total Return Index (TRI), the index jumped from 228 in September 2024 to 263 in September 2025, marking one of the strongest annual performances in recent years.

The TRI is India’s first independent benchmark built on actual transaction data from RERA-registered projects. It uses a weighted average model that includes per-square-foot rates, rental yields and city-level population to provide a realistic picture of housing returns across India’s top markets.

Sales hit Rs 1.52 lakh crore

Residential activity remained buoyant through Q3 2025, with sales touching Rs 1.52 lakh crore. Greater Mumbai continues to be India’s most expensive housing market with an average rate of Rs 33,762 per sq ft, while Pune’s unsold inventory rose to 2,69,348 units—highlighting strong supply but persistent demand.

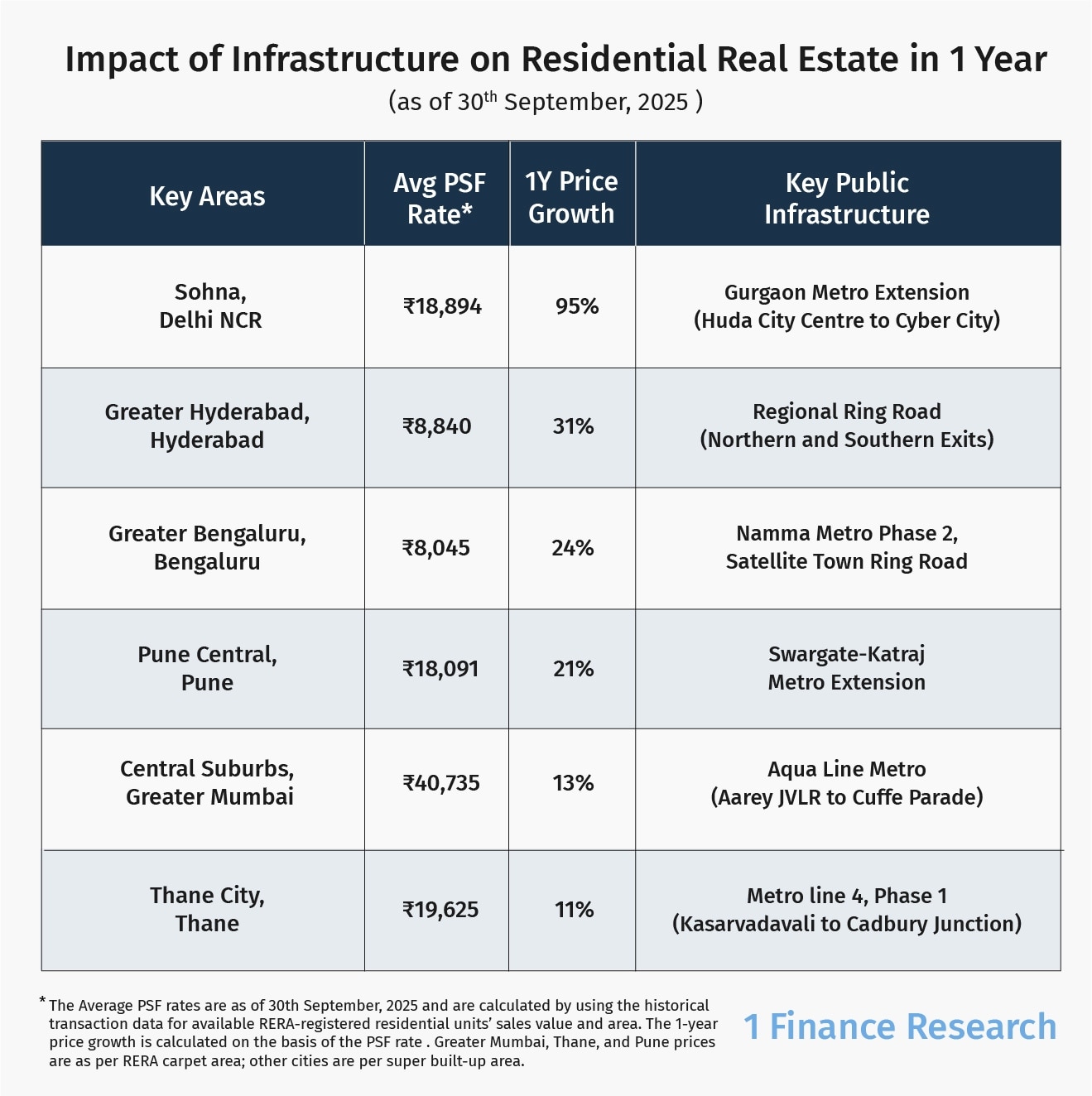

Hyderabad saw a 12% jump in per sq ft prices to Rs 9,100 over the year, spurred by progress on the Regional Ring Road (RRR), which is set to boost connectivity to outer districts. In the Delhi NCR region, nearly 60% of unsold stock is more than five years old, reflecting a clear shift toward new premium launches with better amenities and stronger connectivity.

Infrastructure the real driver

The study finds a direct link between infrastructure expansion and real estate appreciation. Upcoming metro lines, logistics corridors and upgraded arterial roads are reshaping demand patterns, particularly in peripheral regions previously considered too remote.

In Bengaluru, the operationalisation of Namma Metro’s Phase 2 Yellow Line and the expected launch of the Blue Line by 2026 are transforming access to the IT corridor. This enhanced mobility is a major reason behind the 24% price growth in Greater Bengaluru, connecting job centres with more affordable housing belts on the outskirts.

Hyderabad’s RRR project, meanwhile, is creating a logistics backbone for Pharma City and opening up new residential hotbeds around the northern and southern belts of the city. Demand has accelerated sharply in these newly connected pockets.

Greater Mumbai’s Aqua Line metro—from Aarey JVLR to Cuffe Parade—is already influencing prices, contributing to a 13% rise in central suburbs with rates touching ₹40,735 per sq ft.

Commenting on the data, Animesh Hardia, Senior Vice President of Quantitative Research at 1 Finance, said real estate continues to be plagued by misconceptions.

“Real estate stands as the most misunderstood asset class. Its drivers of value are not well recognised because on-ground intelligence is missing. Social media often paints it inaccurately by comparing top companies with the entire real estate market. What needs study is employment, infrastructure and traffic patterns. Without that, any view on real estate is half-baked,” he said.

Even with unsold inventory exceeding 11 lakh units across the top eight cities, the market continues its upward trajectory. Analysts say that infrastructure-led development is bridging the gap between city centres and emerging suburbs, making previously overlooked areas more attractive for both homebuyers and investors.

While excess supply in select pockets may moderate appreciation in the near term, the study concludes that India’s housing market remains firmly supported by end-user demand and accelerated infrastructure expansion—key factors that helped the sector outperform the stock market this year.

'Not targeted at India': Marco Rubio defends US visa changes amid concerns over H-1B, student visas

'Not targeted at India': Marco Rubio defends US visa changes amid concerns over H-1B, student visas 'There are stupid people in US too': Marco Rubio on racist remarks against Indian Americans

'There are stupid people in US too': Marco Rubio on racist remarks against Indian Americans Falta turns saffron: BJP deals fresh blow to Abhishek Banerjee in Diamond Harbour bastion

Falta turns saffron: BJP deals fresh blow to Abhishek Banerjee in Diamond Harbour bastion Relief for Indian techies? New US Green Card rule may not hit H-1B workers immediately

Relief for Indian techies? New US Green Card rule may not hit H-1B workers immediately Iran deal 'largely negotiated', Hormuz to be reopened soon: Donald Trump

Iran deal 'largely negotiated', Hormuz to be reopened soon: Donald Trump WHO Sounds Ebola Alarm | India Today’s Sneha Mordani Explains The Threat

WHO Sounds Ebola Alarm | India Today’s Sneha Mordani Explains The Threat Why Britain Keeps Changing Prime Ministers | Brexit, Chaos & UK Political Crisis Explained

Why Britain Keeps Changing Prime Ministers | Brexit, Chaos & UK Political Crisis Explained No Water In 45°C Heat! Why Raipur's Rewa Village Is Facing A Brutal Water Crisis

No Water In 45°C Heat! Why Raipur's Rewa Village Is Facing A Brutal Water Crisis Honda City launched, ZR-V e:HEV Coming Soon • Double Digit Growth Target • New SUVs Incoming

Honda City launched, ZR-V e:HEV Coming Soon • Double Digit Growth Target • New SUVs Incoming U.S. Tightens H-1B Rules As Visa Applications See Sharp 38% Decline

U.S. Tightens H-1B Rules As Visa Applications See Sharp 38% Decline Varun Beverages shares rebound 42% from March low: Is the rally sustainable?

Varun Beverages shares rebound 42% from March low: Is the rally sustainable? Vedanta Demerger: Systematix sees 186% upside? Target price explained for all 5 companies

Vedanta Demerger: Systematix sees 186% upside? Target price explained for all 5 companies Suzlon Energy, IEX, Reliance Power, ZEEL: How stocks with up to 35% retail stakes fared in 2026

Suzlon Energy, IEX, Reliance Power, ZEEL: How stocks with up to 35% retail stakes fared in 2026 IndusInd Bank shares climb 8% in a month; what investors can do?

IndusInd Bank shares climb 8% in a month; what investors can do? Tata Power Vs Adani Power: Expert shares preferred stock for short term amid peak power demand

Tata Power Vs Adani Power: Expert shares preferred stock for short term amid peak power demand