The ruling highlights the importance of documentation in property transactions involving demolition or structural changes.The ruling highlights the importance of documentation in property transactions involving demolition or structural changes.

The ruling highlights the importance of documentation in property transactions involving demolition or structural changes.The ruling highlights the importance of documentation in property transactions involving demolition or structural changes.In a ruling that could provide relief to property sellers facing disputes over capital gains calculations, the Hyderabad Bench of the Income Tax Appellate Tribunal (ITAT) has held that expenses incurred to demolish an existing structure on land before its sale can be considered for deduction while computing Long Term Capital Gains (LTCG).

The tribunal’s decision came in the case of a taxpayer, Mr. Reddy, who had sold land along with an old structure for ₹2 crore but faced resistance from the tax department over whether demolition-related costs could be included while calculating his capital gains. While the ITAT did not grant a final outright relief, it sent the matter back to the Assessing Officer (AO) for verification, indicating that such costs could indeed qualify as legitimate deductions under Section 48 of the Income Tax Act if properly substantiated.

The background of the dispute

According to Sujit Bangar, Founder and Managing Director of TaxBuddy.com, Mr. Reddy had originally purchased the property in 2012. The property consisted of land along with a cement shed structure.

In February 2017, he sold the property for ₹2 crore. While computing capital gains, he claimed an indexed cost of acquisition of ₹1,83,20,863 and reported a Long Term Capital Gain of about ₹16.69 lakh.

However, a key point of dispute arose from an additional claim of ₹11,24,472 linked to the demolition of the old structure that existed on the land.

Before the sale was executed, the cement shed on the property had to be demolished. According to the taxpayer, the structure was in a condition that required demolition and the buyer had specifically requested that the land be transferred as plain vacant land.

Why the tax officer rejected the claim

Despite this explanation, the Assessing Officer refused to allow the deduction while computing capital gains.

The tax department raised several objections. First, the final registered sale deed mentioned only the transfer of land and did not specifically reflect the demolished structure. Second, officials argued that the scrap value arising from the demolition had not been properly accounted for in the computation.

Another major concern was documentation. The tax officer stated that proper evidence supporting the demolition expenses had not been adequately furnished.

Because of these issues, the deduction linked to the demolished structure amounting to ₹11.24 lakh was disallowed while calculating the capital gains.

ITAT’s interpretation of the law

When the matter reached the Income Tax Appellate Tribunal, the Hyderabad bench examined whether such demolition expenses could legally qualify for deduction under capital gains provisions.

The tribunal clarified that such expenditure could fall into two permissible categories under Section 48.

First, it could be treated as cost of improvement if the demolition was carried out to enhance the value or usability of the property before its transfer.

Alternatively, it could be treated as expenditure incurred wholly and exclusively in connection with the transfer of the property, particularly if removing the structure was necessary to complete the sale.

However, the tribunal emphasised that the taxpayer must establish the factual basis of the claim.

Verification ordered by ITAT

Rather than granting an immediate relief, the ITAT directed the Assessing Officer to re-examine the case and verify several key aspects.

These include whether the structure actually existed on the property, whether it was demolished before the transfer took place, and whether there is sufficient documentary evidence supporting the demolition expenditure.

Only after verifying these details can the tax officer determine whether the deduction should be allowed while computing capital gains.

Capital gains taxes on property sales

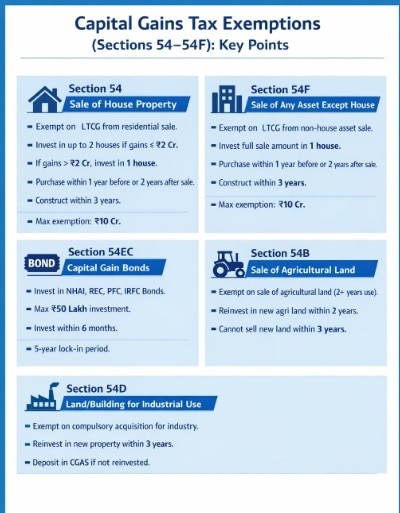

The Income Tax Act provides several exemptions under Sections 54 to 54F that can help taxpayers reduce or eliminate capital gains tax if certain conditions are met. Section 54 allows exemption on long-term capital gains from the sale of a residential property if the gains are reinvested in another house property. Taxpayers can invest in up to two houses if capital gains do not exceed ₹2 crore, a benefit allowed once in a lifetime.

Section 54F applies when long-term capital gains arise from the sale of assets other than a house property, provided the entire sale proceeds are invested in one residential house.

Under Section 54EC, taxpayers can invest up to ₹50 lakh in specified bonds issued by institutions such as NHAI, REC, PFC or IRFC within six months to claim exemption.

Section 54B offers relief when agricultural land used for at least two years is sold and the gains are reinvested in new agricultural land.

Section 54D applies to capital gains from compulsory acquisition of industrial land or buildings.

Key takeaway for taxpayers

The ruling highlights the importance of documentation in property transactions involving demolition or structural changes.

Tax experts say taxpayers planning similar transactions should retain records such as the original purchase deed showing the existence of the structure, confirmation from the buyer requesting vacant land, proof that demolition took place before the transfer, and bills or payment records relating to the demolition work.

If properly documented, such expenses may legitimately reduce the taxable capital gains arising from the sale of property.

IMF flags fiscal risks for India as oil prices rise

IMF flags fiscal risks for India as oil prices rise Why retail investors are looking beyond fixed deposits

Why retail investors are looking beyond fixed deposits RBI announces $5 bn USD/INR swap auction to infuse long-term liquidity into banking system

RBI announces $5 bn USD/INR swap auction to infuse long-term liquidity into banking system Sanjeev Sanyal is working on THIS big reform: 'Every citizen should have a fair chance of...'

Sanjeev Sanyal is working on THIS big reform: 'Every citizen should have a fair chance of...' Ferrari set to get 30% cheaper in India ahead of India-EU FTA rollout

Ferrari set to get 30% cheaper in India ahead of India-EU FTA rollout Sundar Pichai Unveils "Ask YouTube" And Revolutionary Voice-Powered "Docs Live" At Google I/O

Sundar Pichai Unveils "Ask YouTube" And Revolutionary Voice-Powered "Docs Live" At Google I/O Sanjeev Sanyal Debunks Bureaucracy Myths, Highlights 1970s-80s Post-Independence Bad Laws

Sanjeev Sanyal Debunks Bureaucracy Myths, Highlights 1970s-80s Post-Independence Bad Laws GST Council May Simplify Tax Rules For Ola, Uber & Rapido; Cab Fares Could See Impact

GST Council May Simplify Tax Rules For Ola, Uber & Rapido; Cab Fares Could See Impact RITES Q4 Results 2026: Profit Dips, Revenue Jumps 28% | CMD Rahul Mithal Speaks

RITES Q4 Results 2026: Profit Dips, Revenue Jumps 28% | CMD Rahul Mithal Speaks How Resilient Is Dubai And The Broader UAE Property Market?

How Resilient Is Dubai And The Broader UAE Property Market? Coforge, Infosys, TCS, KPIT Tech, TechM shares: Why returns from IT stocks may stay capped

Coforge, Infosys, TCS, KPIT Tech, TechM shares: Why returns from IT stocks may stay capped Top stocks in news: RIL, Apollo Hospitals, ITC, Glenmark, RVNL, Jubilant Food, JK Cement

Top stocks in news: RIL, Apollo Hospitals, ITC, Glenmark, RVNL, Jubilant Food, JK Cement NCDEX launches India's first weather derivatives contract, effective from this date

NCDEX launches India's first weather derivatives contract, effective from this date Rs 7-9 petrol, diesel price hike inevitable; weak OPEC good for India: Energy expert Narendra Taneja | Exclusive

Rs 7-9 petrol, diesel price hike inevitable; weak OPEC good for India: Energy expert Narendra Taneja | Exclusive This pharma stock jumps 11% as Q4 profit surges 200%; announces 721% dividend payout — details here

This pharma stock jumps 11% as Q4 profit surges 200%; announces 721% dividend payout — details here