Experts say if you do not want to increase the tenure of the loan it is better to increase EMI provided it does not hurt the family cash flow.Experts say if you do not want to increase the tenure of the loan it is better to increase EMI provided it does not hurt the family cash flow.

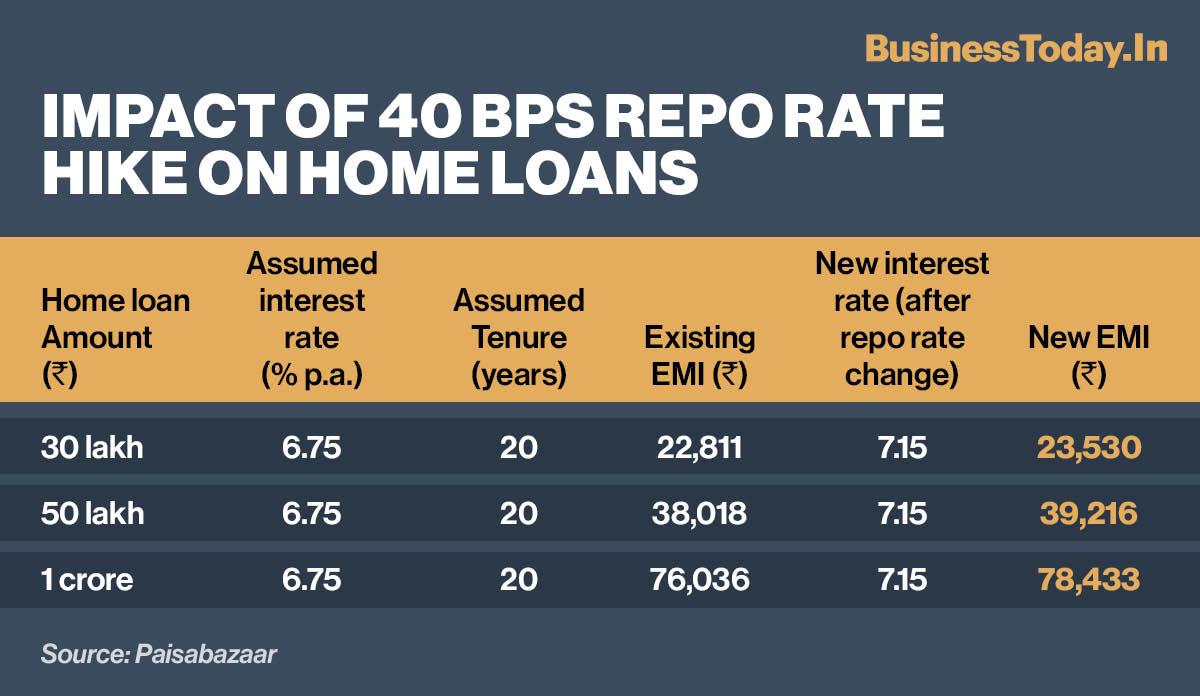

Experts say if you do not want to increase the tenure of the loan it is better to increase EMI provided it does not hurt the family cash flow.Experts say if you do not want to increase the tenure of the loan it is better to increase EMI provided it does not hurt the family cash flow.With banks increasing their benchmark lending rates for home loans you have two options either continue with the ongoing repayment schedule with a higher EMI or switch to a longer tenure with the same EMI amount. The banks are increasing home loan rates because the Reserve Bank of India announced on Tuesday 0.40 per cent hike in repo rate. Following the RBI hike, the credit cost for both existing as well as fresh borrowers will increase. In such a scenario is it good to increase the EMI or tenure of the loan with the rise in interest rates?

Experts say if you do not want to increase the tenure of the loan it is better to increase EMI provided it does not hurt the family cash flow. The default option of most of the banks is, however, to increase the tenure of the loan. “The existing borrowers will see their tenor go up. A home loan borrower with an outstanding principal of Rs 50 lakh and tenor of 20 years at 7 per cent interest could see their tenor extend by 18 months when interest moves up to 7.4 per cent. Borrowers who have taken a Marginal cost of funds-based lending rate (MCLR) will also feel the pressure, though it may take a little longer until the borrowers' loan reset before the new rates come into play for individual borrowers,” says Adhil Shetty, CEO, BankBazaar.com.

V Swaminathan, Executive Chairman, Andromeda and Apnapaisa adds, “A borrower can choose to increase their EMI outgo with the interest rate hike, which may depend on various factors like future income growth, contingency fund, or the possibility to avail another loan. Paying a higher EMI in such a scenario would reduce the amount saved every month. While if someone increases the tenure of the loan, they can save the extra amount and use it for repaying another loan or can invest the same for a return that can balance out the increased interest burden.”

Should you prepay? Home loans also give you an option to make prepayments without any charges. Experts suggest if one has enough savings then one can consider paying a small sum every year. “Long-term loans like home loans allow you to make prepayments. So your best option is to try to prepay your loan. While prepaying 5 per cent of your outstanding every year would be an optimal solution, even a small prepayment of one EMI per year can bring substantial savings,” says Shetty.

Swaminathan adds, “As home loans are big-ticket loans and involve a higher amount as compared to the other loans, it is not advisable to prepay a loan due to an interest rate hike and exhaust all your savings. One can opt for a part prepayment wherein they reduce the principal amount gradually so that the interest burden eases, and they can save more for principal repayment.”

The Reserve Bank of India (RBI) increased the key policy rates by 40 basis points (bps) in a surprise move on Wednesday. The latest RBI's move to increase the repo rate, however, is not an entirely unexpected decision against the backdrop of the rising inflation numbers due to the third wave of the pandemic and the Russia-Ukraine war. The US also intensified its fight against inflation by raising its benchmark short-term interest rate by 0.50 per cent. The Fed’s key rates are now in the range of 0.75 per cent to 1 per cent.

Naveen Kukreja, CEO and Co-founder, Paisabazaar.com says, “The interest rates for existing borrowers linked to repo rate or any other interest rate benchmarks, both internal as well as external, would remain the same till the next reset date of their loans. The new interest rate on their reset date will be calculated after factoring in the benchmark rate applicable on the reset date and credit spreads. This new interest rate will then remain in force till the next reset dates of their loans, irrespective of any repo rate changes by the RBI in the interim. The repo rate cut would not impact any loans availed at fixed interest rates.”

Also read: Equity investors are worried post RBI's rate hike decision on Wednesday; here’s why

Also read: Home loan EMIs are likely to shoot up post RBI rate hike; here’s how you can manage your payments

Also read: Experts explain how to manage your finances amid rising inflation

Also read: ICICI Bank hikes EBLR rate, interest rates on FDs after RBI repo rate hike; details here

Indian stocks boom as guns fall silent in West Asian ceasefire; oil plunges, Hormuz opens

Indian stocks boom as guns fall silent in West Asian ceasefire; oil plunges, Hormuz opens Tariff regulator asks Indian airports to cut some charges for airlines by 25%

Tariff regulator asks Indian airports to cut some charges for airlines by 25% HDFC, ICICI, SBI, Kotak Bank among 23 BFSI stocks to ‘Buy’ - Target prices

HDFC, ICICI, SBI, Kotak Bank among 23 BFSI stocks to ‘Buy’ - Target prices  Not AI models, AI applications are quietly driving India’s revenue streams: Report

Not AI models, AI applications are quietly driving India’s revenue streams: Report Tamil Nadu polls 2026: Lottery king Santiago Martin's wife, Vijay among richest candidates

Tamil Nadu polls 2026: Lottery king Santiago Martin's wife, Vijay among richest candidates Where Is The Smart Money Moving In Debt? | Fixed Income Strategy

Where Is The Smart Money Moving In Debt? | Fixed Income Strategy India Welcomes West Asia War Ceasefire, Speeds Up Evacuation Efforts Amid Regional Tensions

India Welcomes West Asia War Ceasefire, Speeds Up Evacuation Efforts Amid Regional Tensions “All Activities Are Going Well”: ISRO Chief Gives Big Update On India’s Gaganyaan Mission

“All Activities Are Going Well”: ISRO Chief Gives Big Update On India’s Gaganyaan Mission Artemis II Reconnects With Earth After Dramatic 40 Min Moon Blackout In Historic Deep Space Mission

Artemis II Reconnects With Earth After Dramatic 40 Min Moon Blackout In Historic Deep Space Mission #WATCH | Defence Stocks Comeback? How To Invest Smartly Now

#WATCH | Defence Stocks Comeback? How To Invest Smartly Now DCB Bank shares jump 7%; expert says management has 'HDFC Bank-like pedigree'

DCB Bank shares jump 7%; expert says management has 'HDFC Bank-like pedigree' Rs 90,000 crore deployed in markets by mutual funds in March, says Shweta Rajani

Rs 90,000 crore deployed in markets by mutual funds in March, says Shweta Rajani Suzlon, Tata Power, Adani Power, Adani Green, NPTC, Inox Wind: Q4 preview, target pricesHDFC, ICICI, SBI, Kotak Bank among 23 BFSI stocks to ‘Buy’ - Target prices

Suzlon, Tata Power, Adani Power, Adani Green, NPTC, Inox Wind: Q4 preview, target pricesHDFC, ICICI, SBI, Kotak Bank among 23 BFSI stocks to ‘Buy’ - Target prices  Ranbir Kapoor-mints multibagger returns; stock 13x in 6 yrs - Check 'Ramayana' connection

Ranbir Kapoor-mints multibagger returns; stock 13x in 6 yrs - Check 'Ramayana' connection