There is a rapid increase in the adoption of small-ticket personal loans, significantly shifting the credit industry landscape over the last four years.

There is a rapid increase in the adoption of small-ticket personal loans, significantly shifting the credit industry landscape over the last four years.  There is a rapid increase in the adoption of small-ticket personal loans, significantly shifting the credit industry landscape over the last four years.

There is a rapid increase in the adoption of small-ticket personal loans, significantly shifting the credit industry landscape over the last four years. In the second quarter of 2023, India’s retail credit market maintained its growth momentum, primarily fuelled by demand driven by consumption. The latest report from TransUnion CIBIL’s Credit Market Indicator (CMI) indicates a 15% year-on-year increase in credit supply, as measured by originations.

While the performance of most credit products remained steady, there are indications of risk accumulation in specific segments. The report also points out that borrowers’ profiles, preferences and payment habits are changing, as more consumers seek multiple credit products within a short time span.

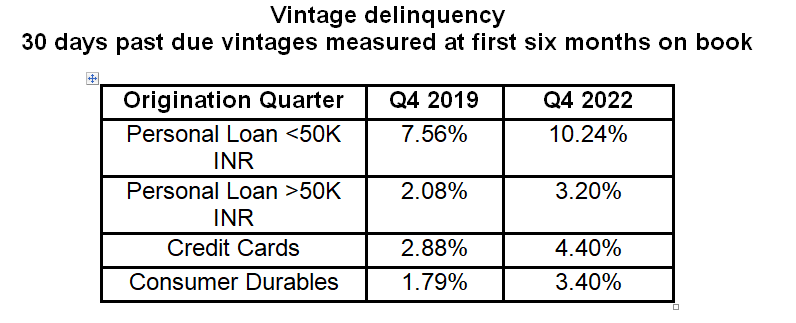

The report states that vintage delinquency trends revealed an uptick in Q4 2022 on consumption loan products compared to Q4 2019. Notably, personal loans of less than Rs 50,000 saw an increase to 10% from 7.56% in Q4 2019. The delinquencies for personal loans above Rs 50,000 and credit cards also increased to 3.20% and 4.40% (Q4 2022), from 2.08% and 2.88% in Q42019. Vintage delinquency is calculated as percentage of sanction amount on accounts ever 30+ days past due in six months from origination.

It was also observed that around 51% of consumers who availed of small-ticket personal loans in Q2 2023 already had more than four credit products at the time of availing another new loan, a sharp contrast to just 17% in the same category in Q2 2019.

There is a rapid increase in the adoption of small-ticket personal loans, significantly shifting the credit industry landscape over the last four years. The report states that since January 2022, small ticket loans below Rs 50,000, while accounting for a small share of retail balances, contributed approximately 25% of total origination volumes. Consequently, the proportion of credit-active consumers utilizing these loans escalated to 8% in June 2023 from 3% in June 2019.

Also read: When is the right time to start investing in mutual funds?

Also read: Exclusive interview: Meet Vishal Jain, the CEO of Zerodha Fund House

Delinquencies on small-ticket personal loans may offer a broader indication of financial stress as consumers potentially prioritize other payment obligations over personal loan repayments, suggesting a need for meticulous monitoring. “The latest CMI indicates financial stability with healthy retail credit growth and broadly stable delinquency levels, even though a few pockets show signs of risk build-up. At the same time, India’s large young population, coupled with low credit penetration in the new-to credit segment, provide huge untapped potential for accelerating credit growth and financial inclusion,” said Rajesh Kumar, MD and CEO of TransUnion CIBIL.

Growth was particularly noticeable amongst semi-urban and rural consumers. However, originations among the new-to-credit consumers witnessed a decrease of 4 percent, pointing to an untapped potential for accelerating financial inclusion considering India’s low credit penetration and large, young population.

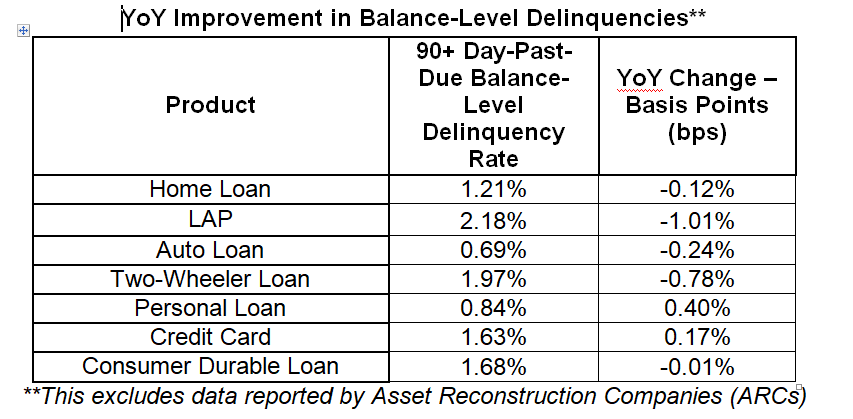

During Q2 2023, overall serious delinquencies, measured as 90 days or more past due, improved across product categories, barring credit cards and personal loans.

“The marked increase in the volume of consumption loans along with velocity indicates a clear call for lenders to monitor vintage delinquencies closely. Strong underwriting process, focused regular monitoring of consumer behaviour, and robust credit risk management practices are essential if these opportunities are to be nurtured for long-term profitable growth,” said Kumar.

Overall, India’s retail credit market continued to show sustained growth during Q2 2023, with consumption-led demand driving the need for credit. Credit supply (originations) grew at 15% year-over-year (YoY) compared to Q2 2022. Portfolio performance remained mostly stable compared to the same period in the prior year for most products.

Artemis 2 mission: Astronauts return to Earth after NASA's first Moon voyage in 50 yrs, splash down in Pacific Ocean

Artemis 2 mission: Astronauts return to Earth after NASA's first Moon voyage in 50 yrs, splash down in Pacific Ocean Fabindia eyes AI-first future as digital surge reshapes retail playbook, says William Bissell

Fabindia eyes AI-first future as digital surge reshapes retail playbook, says William Bissell Akshaya Tritiya 2026: How silver prices have moved since last year's Akshaya Tritiya

Akshaya Tritiya 2026: How silver prices have moved since last year's Akshaya Tritiya Akshaya Tritiya: ₹96,000 got you 10 gm gold in 2025 but what it gets you in 2026 is shocking

Akshaya Tritiya: ₹96,000 got you 10 gm gold in 2025 but what it gets you in 2026 is shocking LPG, CNG, PNG rates on April 11, 2026: Check latest prices in Delhi, Mumbai, Chennai, Kolkata

LPG, CNG, PNG rates on April 11, 2026: Check latest prices in Delhi, Mumbai, Chennai, Kolkata BJP’s Bengal Manifesto Puts UCC Front And Centre As Amit Shah Sharpens Attack On Mamata

BJP’s Bengal Manifesto Puts UCC Front And Centre As Amit Shah Sharpens Attack On Mamata Taigun Facelift Push: Volkswagen Targets Market Outperformance

Taigun Facelift Push: Volkswagen Targets Market Outperformance No Fuel Crisis: Govt Assures LPG, Petrol & Gas Supply Stability

No Fuel Crisis: Govt Assures LPG, Petrol & Gas Supply Stability #Podcast | #Episode10 | Exclusive: William Bissell, MD, Fabindia On Journey, AI-Transfomation & More

#Podcast | #Episode10 | Exclusive: William Bissell, MD, Fabindia On Journey, AI-Transfomation & More Market Rally Continues! Nifty Near 24,000, Bank Nifty’s Best Week Since 2021

Market Rally Continues! Nifty Near 24,000, Bank Nifty’s Best Week Since 2021 ITC, HUL shares offer up to 31% upside: Why brokerage sees a 'Buy' opportunity

ITC, HUL shares offer up to 31% upside: Why brokerage sees a 'Buy' opportunity 'Buy' Suzlon Energy, Paytm & GE Vernova shares: PL's analyst; check price targets

'Buy' Suzlon Energy, Paytm & GE Vernova shares: PL's analyst; check price targets 70% dividend stock: Rs 7/share - Check record date, returns | Do you own?

70% dividend stock: Rs 7/share - Check record date, returns | Do you own? Coforge, Persistent Systems, Happiest Minds: Should you buy these IT stocks ahead of Q4 earnings?

Coforge, Persistent Systems, Happiest Minds: Should you buy these IT stocks ahead of Q4 earnings? RIIL Q4 results 2026 date and time: Check quarterly earnings schedule of Reliance Group firm

RIIL Q4 results 2026 date and time: Check quarterly earnings schedule of Reliance Group firm