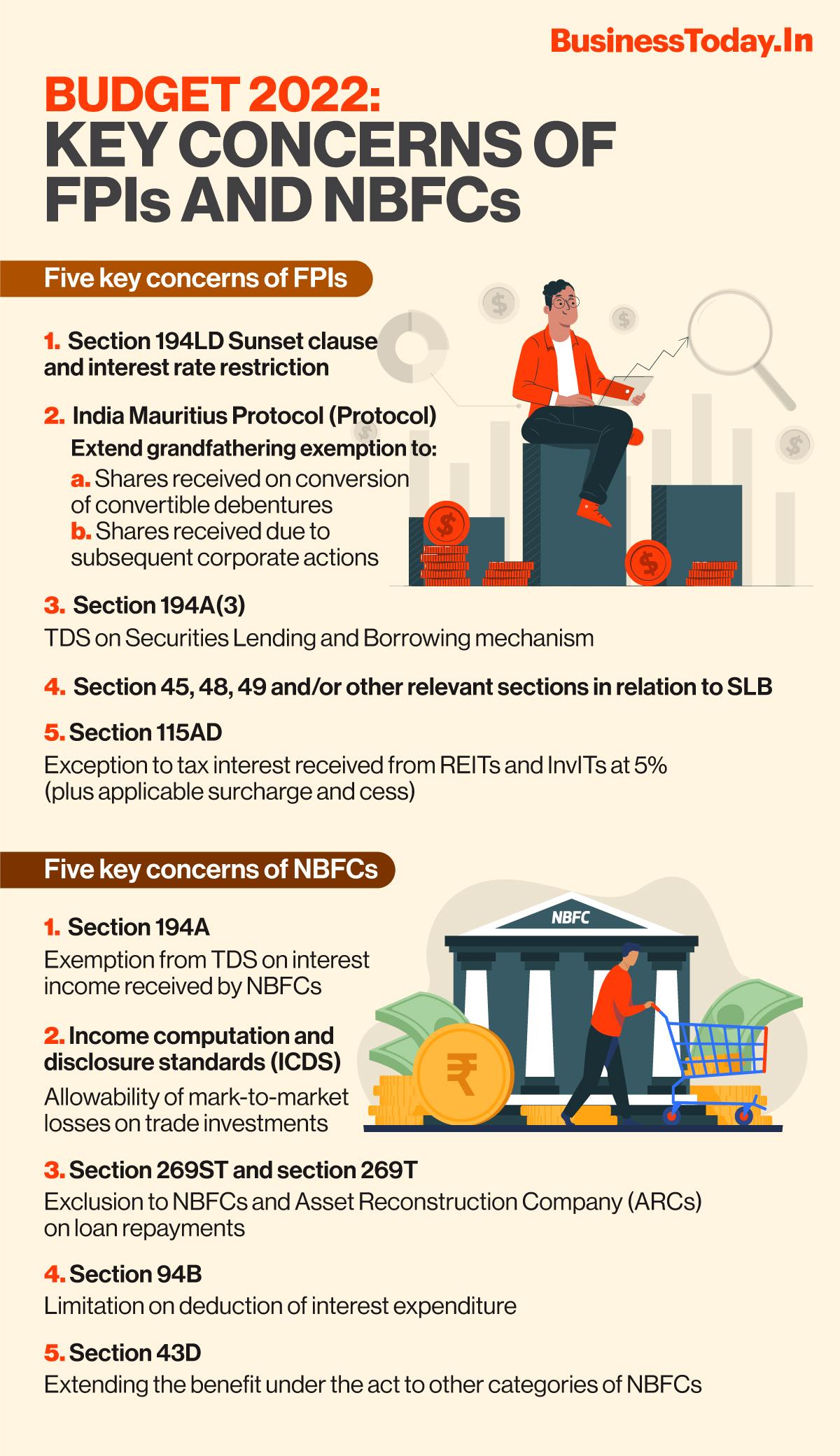

Foreign portfolio investors (FPIs) will be concerned with sections that deal with the taxation and exemption from taxation for investment instruments held. There are five key concerns of FPIs: -

Also Read: Budget 2022: What financial services sector expects from FM Sitharaman

1. Section 194LD Sunset clause and interest rate restriction: To encourage FPI investors to invest in rupee-denominated bonds, reduced TDS should be made perpetual and not expire on 30 June 2023. This rate should apply for interest paid to the extent of the SBI base rate plus 500 basis points. Accordingly, the increased TDS rate of 20% should apply only to the interest paid in excess of the prescribed cap.

2. India Mauritius Protocol (Protocol) - Extend grandfathering exemption to (a) shares received on conversion of convertible debentures; (b) shares received due to subsequent corporate actions: Suitable clarifications be issued to exempt: (a) income/gains on transfer of shares received after 1 April 2017 on conversion of convertible debentures held prior to 1 April 2017; (b) income/gains on transfer of shares received after 1 April 2017 due to corporate actions with respect to investments made by the shareholder prior to 1 April 2017.

3. Section 194A(3) - TDS on Securities Lending and Borrowing mechanism: The provisions of the Act, may be suitably amended to exempt the borrowing charges paid to National Securities Clearing Corporation Ltd (NSCCL). by the borrower on securities borrowed under the Securities Lending and Borrowing (SLB) scheme from provisions of tax deduction at source.

4. Section 45, 48, 49 and/or other relevant sections in relation to SLB: For the purpose of fling the annual income-tax return in India by the FPI, the cost of acquisition should be determined basis the fair market value (FMV) as on 31 March and should be taxed accordingly (and the difference if any in the capital gains should be adjusted in the subsequent years). The FMV as on the due date of advance tax/ date of payment, whichever is earlier should be considered for the purpose of discharging the advance tax liability (and the balance should be adjusted in the year in which the cost of acquisition is crystallised).

5. Section 115AD: To encourage FPI investors to invest in units of Business Trust it is suggested that an exception may be provided to tax interest received from REITs and InvITs at a concessional rate of 5% (plus applicable surcharge and cess) under section 115AD of the Act.

Also Watch: Will the banking sector get a booster shot in Budget 2022-23?

Non-banking finance companies (NBFCs) will seek to fortify their interests in the industry by clarifications around these five pointers:-

1. Section 194A - Exemption from TDS on interest income received by NBFCs: Since NBFCs are similar to banks, the benefit of the provisions of section 194A should also be extended to them, i.e., the interest income earned by NBFCs should be exempted from any TDS requirement. The NBFCs could continue to discharge their tax liability by way of advance taxes.

2. Income computation and disclosure standards (ICDS) - NBFCs - Allowability of mark-to-market losses on trade investments: It is suggested that NBFCs be exempted from the aforesaid requirement and be allowed a tax deduction for the loss recognised on an individual security basis and not for the category as a whole.

3. Section 269ST and section 269T - Exclusion to NBFCs and Asset Reconstruction Company (ARCs) on loan repayments: It is recommended that NBFCs and ARCs also should also be excluded from the purview of the provision of section 269ST and 269T of the Act to provide a boost to recoveries and consequently benefit this sector.

4. Limitation on deduction of interest expenditure under section 94B of the Act: It is recommended that along with banks and insurance companies, NBFCs should also be excluded from the provisions of section 94B of the Act. Since lending and borrowing money is an integral part of the business operations of NBFCs, this change will help the NBFCs to raise capital once again from their overseas associated enterprises.

5. Extending the benefit under section 43D of the Act to other categories of NBFCs: It is recommended that along with deposit-taking and systematically important non-deposit taking NBFCs, non-systematically important NBFCs should also be included within the purview of section 43D of the Act, in an attempt to reduce hardship for NBFCs.

These sub-sectors have analysed their requirements and now await the budget announcements to see the quantifiable impact it will have on their holdings, business and earnings.

These predictions have been made after careful and extensive analysis of government documents, industry standards and behaviour of taxation trends.

The intent is to streamline the administrative, financial and taxation systems to bring modernity, accuracy, and fairness in all spheres of the financial services ecosystem.

(The author is Associate Director, Grant Thornton Bharat and Amit Kedia, Chartered Accountant, Mumbai.)

This year's Union Budget is keenly awaited to analyse the impact it will have on financial services sector and the sub-sectors within.

This year's Union Budget is keenly awaited to analyse the impact it will have on financial services sector and the sub-sectors within. Vinod Aggarwal, Vice Chairman of Eicher Motors; Sanjeev Arora, President, Motion Business at ABB India; Palash Srivastava, Deputy Managing Director at IIFCL and Nilesh Tribhuvan, Managing Partner, White & Brief Advocates & Solicitors") BT Infra Summit 2026: What will power India's next growth spurt?

BT Infra Summit 2026: What will power India's next growth spurt? BT Infra Summit 2026: How Sagarmala 2.0 is going to steer India's maritime growth

BT Infra Summit 2026: How Sagarmala 2.0 is going to steer India's maritime growth Why Bloomberg isn't ready to add Indian bonds yet despite sweeping market reforms

Why Bloomberg isn't ready to add Indian bonds yet despite sweeping market reforms BT Infra Summit 2026: India's energy security needs a new playbook as clean power, storage and grid modernisation take centre stage

BT Infra Summit 2026: India's energy security needs a new playbook as clean power, storage and grid modernisation take centre stage ITR filing 2026: WazirX launches free crypto tax reporting platform ahead of ITR deadline

ITR filing 2026: WazirX launches free crypto tax reporting platform ahead of ITR deadline Data Centres, Space & A Stable Rupee: India's Blueprint For The Next Growth Cycle

Data Centres, Space & A Stable Rupee: India's Blueprint For The Next Growth Cycle Red Sea Crisis: How Global Shipping Lines Are Navigating Another Major Disruption

Red Sea Crisis: How Global Shipping Lines Are Navigating Another Major Disruption Why EV Trucks Are Still Missing From India's Highways | BT Infrastructure Summit 2026

Why EV Trucks Are Still Missing From India's Highways | BT Infrastructure Summit 2026 #BTInfrastructureSummit: Powering India's New Growth Spurt With Infra, Investment & Innovation

#BTInfrastructureSummit: Powering India's New Growth Spurt With Infra, Investment & Innovation Why Indians Feel Foreign Infrastructure Is Better: Hitachi India CEO Breaks It Down

Why Indians Feel Foreign Infrastructure Is Better: Hitachi India CEO Breaks It Down Maruti Suzuki Q1 results: Profit slips 9% YoY to Rs 3,447 crore; revenue climbs 36%

Maruti Suzuki Q1 results: Profit slips 9% YoY to Rs 3,447 crore; revenue climbs 36% ITC Q1 results: Profit slips 16% to Rs 4,394 crore YoY; revenue climbs 28%

ITC Q1 results: Profit slips 16% to Rs 4,394 crore YoY; revenue climbs 28% BTTV Exclusive: M&M CEO Rajesh Jejurikar on Q1 earnings, business outlook, order book and more

BTTV Exclusive: M&M CEO Rajesh Jejurikar on Q1 earnings, business outlook, order book and more  Nifty IT stocks rebound in July as semiconductor shares falter; reverse AI trade at play?

Nifty IT stocks rebound in July as semiconductor shares falter; reverse AI trade at play? Dixon Technologies Q1 earnings: Net profit at Rs 718 crore, revenue rises 21%

Dixon Technologies Q1 earnings: Net profit at Rs 718 crore, revenue rises 21% Can AI Create Wealth For Everyone? DSCI CEO Explains The Future

Can AI Create Wealth For Everyone? DSCI CEO Explains The Future