Mumbai-based Krutti Sundar Patra, 33, is a senior manager in a public sector bank and he is planning to get married soon. He lives in his own house, which he bought in 2015. His father, a senior citizen, and his mother, aged 59, live in Odisha, and both are financially dependent on him. Patra wants to retire comfortably, and he is already saving for it. "I also want to go to Amsterdam for my dream vacation. So, I want to start financial planning early on to reach these goals," he says.

Cash Flow and Net Worth

Patra's monthly income is `65,000, and he spends `37,000 per month, including the home loan EMI of `15,000. Another `15,000 a month is spent to meet the personal expenses of his dependent parents. He also pays an annual premium of `61,000 for his life insurance policies. According to financial planner Pankaj Mathpal, Patra should lower his budget for some of his future goals and curtail his expenses to increase his monthly savings. He should also convert his life insurance policies (except the term plan) to paid-up status to reduce premium. It will help him manage his cash flow better and save more for his future financial goals.

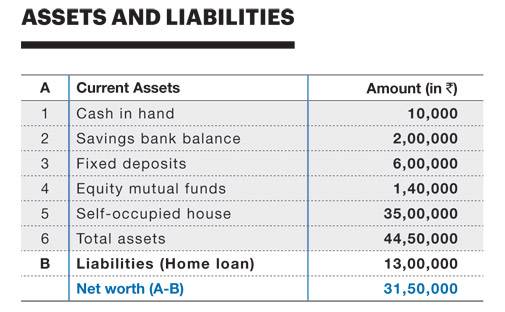

The total value of Patra's financial assets is `9.50 lakh, out of which `6 lakh is invested in bank fixed deposits and `2 lakh is kept in a savings account. He has also put `1.40 lakh in equity-oriented mutual fund schemes. Patra has a self-occupied house, and its current value is `35 lakh. He has taken a home loan for buying the house, and the current outstanding is `13 lakh (see table Assets and Liabilities).

Taking Care of Essentials

Contingency fund: The total balance in Patra's savings account is `2 lakh while he has a mandatory monthly expense of `52,000. It means he has an adequate contingency fund, covering expenses for around four months. But considering the low interest rate on savings bank accounts, he should only keep `50,000 there, and the balance can be parked in a liquid fund scheme under a mutual fund (see table Cash Flow Management).

Health cover: A health insurance provides financial coverage for most medical emergencies. Patra is covered by the group health insurance policy of his employer and the sum insured is `3 lakh. However, his parents do not have any health cover. He should immediately buy individual health insurance policies for his parents.

Life insurance: Patra's parents are financially dependent on him, and he also has an outstanding liability in the form of a home loan. To mitigate any future risk, he has already bought a term insurance plan with `75 lakh sum assured. He also has additional life insurance cover of `10.50 lakh for which he pays an annual premium of `61,000. As Patra has adequate insurance cover via the term plan he has bought, he should think of converting other policies to paid-up status.

Setting Financial Goals

Buying a car: Patra wants to buy a car in 2018 but considering his limited resources, he should postpone it for the next three years (see table Goals to Achieve). Also, he should link the mutual fund investments, recently started via the SIP route, to achieve this goal. He is expected to accumulate `2 lakh in three years with a monthly investment of `5,000 in mutual funds. The rest of the amount to buy a car can be raised through a car loan.

Own marriage: Patra wants to get married within a year, and according to the information provided by him, it will cost him around `10 lakh. As he has limited surplus money (except the money reserved for contingency), he should lower the budget for his marriage.

Children's education, marriage: Considering his limited monthly savings, we advise him to plan for these goals only after his marriage. With some additional income from his wife, it could be easier to plan for these goals.

Buying another house: Patra wants to buy another house after three years. He is currently living in his own house, which he bought two years ago. Its current market value is `35 lakh, and the home loan outstanding is `13 lakh. He is paying an interest of 9.05 per cent, which is higher than the current rate of interest offered by most banks. As he is working in a public sector bank, he must be aware of this scenario. With the reduction in the rate of home loan interest, he should try and get a reduction in EMI, which will help him save more money for his future financial goals. Considering a 10 per cent annual appreciation in the property rate, the value of the house is expected to be `46.58 lakh and the cost of the second house that he wants to buy is expected to be about `66.55 lakh after three years. Therefore, he will have a surplus of `34.58 lakh after repaying the current home loan. Patra can use the net sales proceeds from his existing house for the down payment and raise the rest as a home loan when he buys the new house.

Dream vacation: He is planning to go on a vacation in 2020, which will cost him around `1.22 lakh, taking into account that such vacations now cost around `1 lakh, and inflation could rise to 7 per cent. He should start investing `3,000 per month for going on his dream vacation.

Retirement corpus: Considering the current expected cost of retirement to be `1 crore, Patra should plan to accumulate around `4 crore for his retirement corpus. Besides contributing `13,000 per month to the National Pension System, he will have to invest `17,000 a month to amass the desired amount. It may not be possible for him to save the required amount from his current monthly income but he should immediately start investing `5,000 per month in a diversified equity fund via SIP and increase the SIP amount periodically to achieve the desired goal.

The bottom line: Patra should immediately transfer `1.50 lakh to liquid funds from his savings bank account. He can stay invested in fixed deposits as he will need the money within a year to meet his marriage expenses. All mutual fund schemes he has selected for SIP are good, and he should continue to invest in these schemes. Also, he should add ICICI Prudential Balanced Advantage Fund, Aditya Birla Sun Life Pure Value Fund and Mirae Asset Emerging Bluechip Fund to his portfolio.