India isn’t atmanirbhar in fertilisers yet

India isn’t atmanirbhar in fertilisers yetWith Iran attacking the gas fields of Qatar and Saudi Arabia early Thursday morning, India’s food and nutritional security is now threatened by disruption to fertiliser supplies. India will face disruption of feedstocks or raw materials such as natural gas (LNG), potash, and sulphur required to produce fertilisers, as well as ready-made or finished fertilisers like urea, Diammonium Phosphate (DAP), and Muriate of potash (MOP).

Also read: BT EXPLAINER: Why Iran's attack on Qatar's Ras Laffan is a terrible news for the world

Both these countries are major suppliers of these feedstocks and finished fertilisers of India. In addition to the partial closure of the Strait of Hormuz, Thursday’s attack potentially threatens to close the Red Sea route too.

The West Asia war is also severely testing India’s energy security due to the restricted supply of crude oil and gas (LNG and LPG). India’s import dependency has risen over the years. The Ministry of Petroleum and Natural Gas data show, in FY25, India’s import dependency for crude oil was 90.5%, LNG 50%, and LPG 66%. In the case of fertiliser, it was 68.6%, as per the Indian Council for Research on International Economic Relations (ICRIER).

Also read: Will Hormuz crossings cost more? Iran considers tolls on global shipping route

A bright spot amidst supply crisis

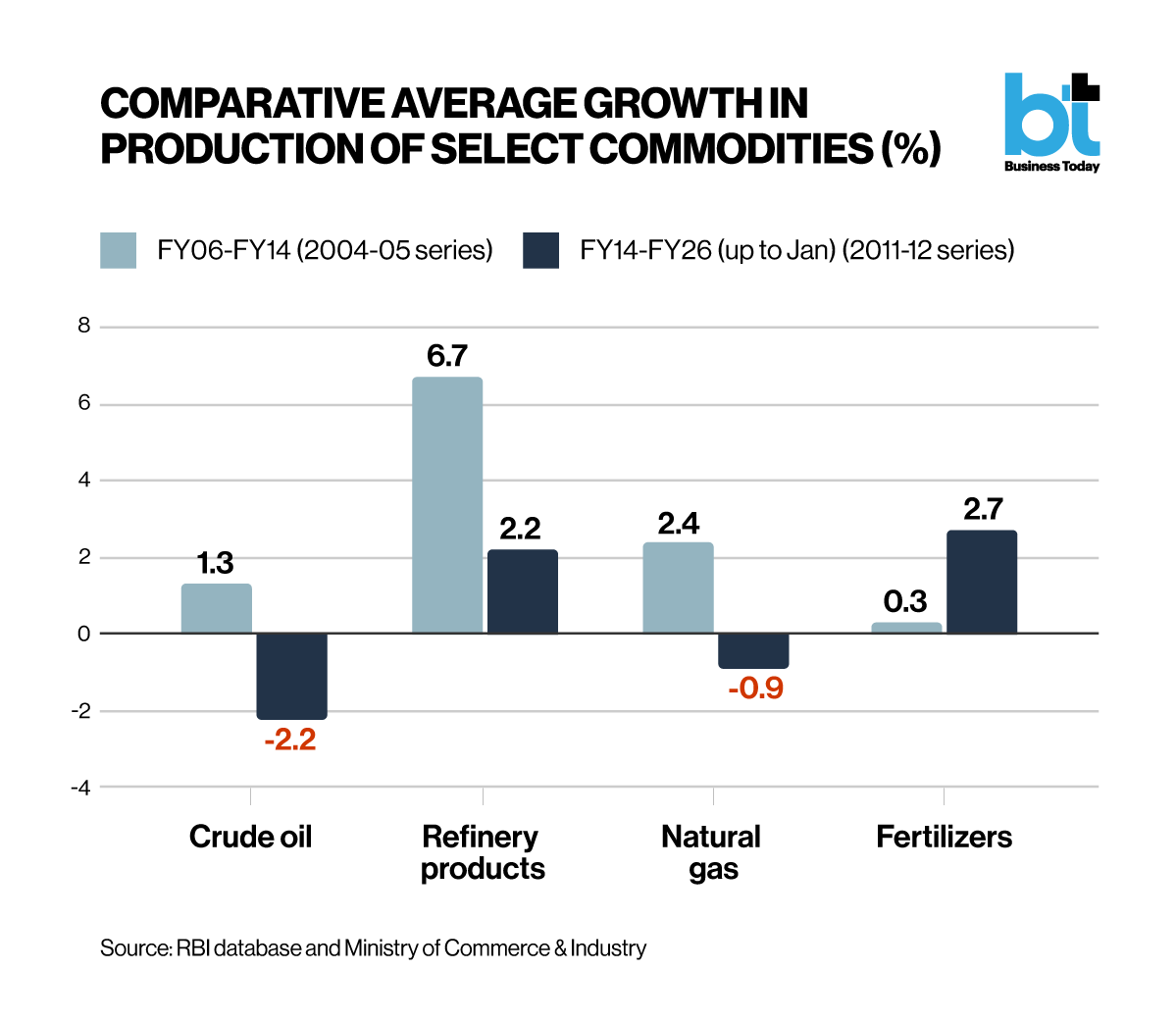

A comparative study of the growth in the Index of Industrial Production (IIP) for core industries in the current 2011-12 series against the 2004-05 series shows that the average growth in crude oil, refinery products (which includes Liquid Petroleum Gas or LPG), and natural gas (LNG) fell sharply, while that of fertilisers went up.

The following graph maps these changes during FY06-FY14 in the 2004-05 series with that of FY14-FY26 (April-Jan) during the current series of 2011-12.

It is widely known that the growth in crude oil, refinery products, and natural gas is slackening due to various factors. Most oil fields are mature and witnessing decline, extraction becoming more expensive and technologically demanding, and few new discoveries are being made.

Why has fertiliser bucked the trend?

It is because several new fertiliser plants have been added in recent years. Some have come up in the place of closed urea plants (due to financial losses) with feedstocks changed from naphtha and fuel oil to cheaper natural gas (LNG).

Some of these developments in the 2020s, according to the Department of Fertilisers, include:

New urea plants have come up at the site of closed ones at Barauni, Gorakhpur, Sindri, and Ramagundam. A plant at a site in Talcher that closed earlier is under commissioning. All these are public sector undertakings.

Two diammonium phosphate (DAP) plants were commissioned at Sagar and Meghnagar.

One urea plant at Namrup and two DAP plants at Thal and Debari are coming up.

These are a fortuitous development because fertiliser supply is critical: (a) 46.1% of India’s total workforce is engaged in agriculture and allied activities (as per the Periodic Labour Force Survey of 2023-24) and (b) the agriculture and allied sector contributes over 19% to the GDP (as per the new 2022-23 series). It is also fortuitous that there isn’t an immediate threat to fertiliser supply as we are in a lean season. The winter crop (Rabi) is being harvested and Kharif sowing is some months away. The Centre told the Parliament on March 13 that no state had complained of shortages.

Why India isn’t atmanirbhar in fertilisers yet

Despite its critical role, fertiliser scarcity is chronic and routine.

Ritika Juneja, a research fellow at the ICRIER and the lead author of the study “Derisking Fertiliser Supplies for India amid Rising Geopolitical Risks,” published a few days ago, offers two major causes.

One is extreme import dependency. She says: “We don’t have sufficient feedstocks or raw materials to produce fertilisers. The majority of these, natural gas (LNG), rock phosphate, phosphoric acid, sulphur, ammonia, muriate of potash (MOP), are imported from the Gulf countries and others. We also import a significant amount of finished fertilisers.”

She lists Oman, Saudi Arabia, Qatar, the UAE, Jordan, and Israel as the Gulf countries India is dependent on, making it vulnerable to the disruptions in the Strait of Hormuz.

Her study shows, in FY25, the imported components of feedstocks accounted for 44.5% and imported finished fertilisers (urea, DAP, MOP) another 24.1% – taking the total import dependency to 68.6%. “Our effective self-sufficiency in fertilisers is, thus, only 31.4%," she states.

The second big factor is the excess demand for subsidised urea. She says: “The excess demand is reflected in diversion of subsidised urea for non-agricultural use and even across the borders to the tune of 20-25%.” This seems quite a moderation. The Economic Survey of 2016-17 had said: “41% of urea is diverted to industry or smuggled across borders”.

Diversion is indeed a chronic issue.

Jugal Kishore Mohapatra, former secretary in the Department of Fertilisers, told Business Today that India went for neem-coated urea (which slows down the release of nitrogen) to check diversion of subsidised urea for industrial use, but that didn’t work.

He argues that this was “because the neem coating was not done honestly, there was no quality control”. News reports suggest that industrial units have found easy ways to remove the neem coating, and the subsidised urea is extensively used in plywood units, cattle feed manufacturing units, and other industries.

Siraj Hussain, former secretary in the Ministry of Agriculture, adds a few more factors for India’s import dependence: “Most of the time it is cheaper to import fertilisers than produce them at home. Besides, fertiliser plants are getting old, and no new private investment is coming because of price control and other regulations.”

Mohapatra says India has a dual subsidy system in which a fixed subsidy is given for urea, while a variable one is given for phosphatic and potassic (P&K) fertilisers. Then there is distribution control through the Movement Control Order, which fixes monthly supply targets for fertilisers suppliers in specific areas. This deters private investment.

Way forward for Atmanirbhar Bharat

Experts have routinely suggested deregulating fertilisers, weaning away farmers from excessive use of urea, diversifying the source of feedstocks and finished fertilisers, and taking steps to incentivise private investment. Mohapatra insists on two additional measures that can go a long way to ensure India’s self-sufficiency.

The first is to gasify coal – a thermo-chemical process that converts coal into synthesis gas or ‘syngas’ – as an alternate energy source for fertilisers (useful now that LNG production has fallen and import hampered due to the war in West Asia).

“China is the only country that has the technology, and it produces about 90% of ammonia through coal gasification. India should either develop the technology or seek it through joint ventures and also encourage the private sector to do so," Mohapatra suggests.

Last heard, the public sector Talcher urea plant, under commissioning (mentioned earlier) roped in a Chinese firm for coal gasification. Its success would determine how successful India’s “National Coal Gasification Mission”, launched in 2021 with a goal of achieving 100 million tonne coal gasification by 2030, will be.

The second measure Mohapatra suggests is to allow the private sector to import urea.

“This has been a long-pending issue. The private sector should be allowed to import urea, say 50% of the total import. The private sector has greater networking, which will bring efficiency," he proposes.

He draws attention to a similar plea made by former Chief Economic Advisor Arvind Subramanian in his Economic Survey of 2016-17. The report had objected to the fact that only three agencies, State Trading Corporation of India (STC), Metals and Minerals Trading Corporation of India (MMTC), and India Potash Limited (IPL), were allowed to import urea (canalisation) – adding another layer of regulation to aggravate the availability of urea.

India's largest airline IndiGo says Adani airline will be a huge conflict of interest

India's largest airline IndiGo says Adani airline will be a huge conflict of interest 'Giant leap in air defence': India successfully tests Kusha long-range missile for first time

'Giant leap in air defence': India successfully tests Kusha long-range missile for first time Who is Ashiss Kumar Dash, the new CEO-designate at IT major Infosys?

Who is Ashiss Kumar Dash, the new CEO-designate at IT major Infosys? From Haldiram’s to Lakshmi Mittal: Who made millions from Skyroot, India’s first private space unicorn

From Haldiram’s to Lakshmi Mittal: Who made millions from Skyroot, India’s first private space unicorn Switching from iPhone to Android? Google’s Android 17 just made it much easier; Here’s how

Switching from iPhone to Android? Google’s Android 17 just made it much easier; Here’s how Samsung India's Akshay Gupta Reveals Idea Behind New Foldable Form Factor

Samsung India's Akshay Gupta Reveals Idea Behind New Foldable Form Factor Why HFCL Raised Its FY27 Growth Target To 40% | Mahendra Nahata Exclusive

Why HFCL Raised Its FY27 Growth Target To 40% | Mahendra Nahata Exclusive Gold Vs Silver: Which Metal Should You Buy Now? Kunal Shah Decodes The Biggest Opportunities

Gold Vs Silver: Which Metal Should You Buy Now? Kunal Shah Decodes The Biggest Opportunities Nifty, Bank Nifty & Top Trading Picks | Market Masters With Prashant Shah

Nifty, Bank Nifty & Top Trading Picks | Market Masters With Prashant Shah Top 5 Safe Investment Options For You | Personal Finance

Top 5 Safe Investment Options For You | Personal Finance Sensex, Nifty extend losing streak to 4th day as Brent crude nears $100; more downside ahead?

Sensex, Nifty extend losing streak to 4th day as Brent crude nears $100; more downside ahead? Infosys Q1 earnings: IT major cuts FY27 revenue forecast amid muted demand expectations

Infosys Q1 earnings: IT major cuts FY27 revenue forecast amid muted demand expectations  Infosys Q1 FY27 profit rises 12%; board names Ashiss Kumar Dash as Salil Parekh's successor

Infosys Q1 FY27 profit rises 12%; board names Ashiss Kumar Dash as Salil Parekh's successor Twenty Microns shares in sideways trend, analyst suggests Rs 185 stop loss

Twenty Microns shares in sideways trend, analyst suggests Rs 185 stop loss Stovekraft shares trading in a range, ICICI Securities' analyst shares strategy

Stovekraft shares trading in a range, ICICI Securities' analyst shares strategy  'Don't spend ₹20 lakh to impress relatives': Bengaluru CA explains why a big wedding may not be the best financial decision

'Don't spend ₹20 lakh to impress relatives': Bengaluru CA explains why a big wedding may not be the best financial decision Next decade is about embedding tech in daily farming decisions: Godrej Agrovet CEO Sunil Kataria

Next decade is about embedding tech in daily farming decisions: Godrej Agrovet CEO Sunil Kataria 'Failure is okay, cheating is not': Sachin Tendulkar recalls father's lesson amid NEET agitation

'Failure is okay, cheating is not': Sachin Tendulkar recalls father's lesson amid NEET agitation South India scores high on healthy eating habits, but mental and financial wellbeing remain concerns: Survey

South India scores high on healthy eating habits, but mental and financial wellbeing remain concerns: Survey Office demand hits 48 mn sq ft: India's macro strengths shield property market from global shock

Office demand hits 48 mn sq ft: India's macro strengths shield property market from global shock