Kotak Mahindra Bank saw a 10% increase in net interest income (NII) during the June quarter, amounting to Rs 6,842 crore.

Kotak Mahindra Bank saw a 10% increase in net interest income (NII) during the June quarter, amounting to Rs 6,842 crore. Kotak Mahindra Bank saw a 10% increase in net interest income (NII) during the June quarter, amounting to Rs 6,842 crore.

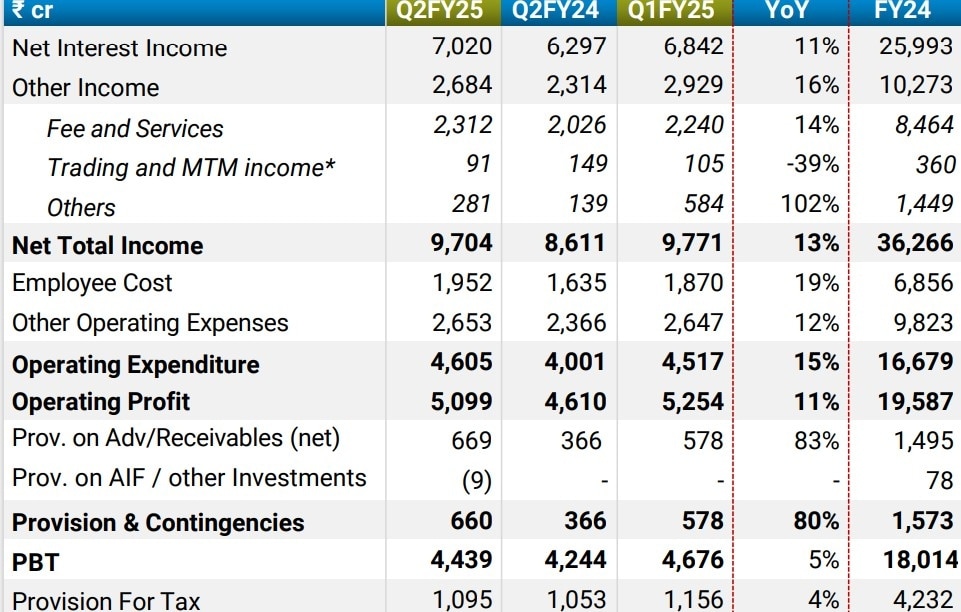

Kotak Mahindra Bank saw a 10% increase in net interest income (NII) during the June quarter, amounting to Rs 6,842 crore.Private lender Kotak Mahindra Bank announced on October 19 that its standalone profit after tax (PAT) for Q2FY25 was Rs 3,344 crore, reflecting a 5% YoY growth compared to Rs 3,191 crore in the same period of the previous year. The rise in profits was offset by a substantial increase in provisions made during the quarter.

The bank's net interest income (NII) for Q2 FY25 stood at Rs 7,020 crore, marking an 11% increase from Rs 6,297 crore in the corresponding quarter of FY24.

The bank's net interest margin (NIM) was 4.91% for Q2, lower from 5.22% recorded in Q2FY24.

As of September, gross net performing assets rose to 1.49% from 1.72% YoY and net NPA also rose to 0.43% from 0.37% YoY.

At the consolidated level, Return on Assets (ROA) for Q2FY25 (annualized) was 2.53% (2.68% for Q2FY24). Return on Equity (ROE) for Q2FY25 (annualized) was 13.88% (14.99% for Q2FY24).

Consolidated Capital Adequacy Ratio as per Basel III as of September 30, 2024, was 22.6% and CET I ratio was 21.7% (including unaudited profits).

Consolidated Networth as at September 30, 2024 was Rs 147,214 crore (including increase in reserves due to RBI’s Master Direction on Bank’s investment valuation of Rs 4,777 crore and gain on KGI divestment of Rs 2,730 crore). The Book Value per Share at September 30, 2024 was Rs 740 (Rs 605 at September 30, 2023).

Standalone results

The Bank reported a Profit After Tax (PAT) of Rs 3,344 crore for Q2FY25, an increase of 5% YoY from Rs 3,191 crore in Q2FY24. Net Interest Income (NII) for Q2FY25 rose to Rs 7,020 crore from ₹6,297 crore in Q2FY24, up 11% YoY. The Net Interest Margin (NIM) was 4.91% for Q2FY25.

Fees and services for Q2FY25 increased to Rs 2,312 crore from rs 2,026 crore in Q2FY24, up 14% YoY. Operating profit for Q2FY25 rose to Rs 5,099 crore from Rs 4,610 crore in Q2FY24, up 11% YoY.

As of September 30, 2024, the Bank had 5.2 crore customers (compared to 4.6 crore as of September 30, 2023).

Customer Assets, including Advances (incl. IBPC & BRDS) and Credit Substitutes, increased by 18% YoY to Rs 450,064 crore as of September 30, 2024, from rs 380,412 crore as of September 30, 2023.

Advances (incl. IBPC & BRDS) increased by 17% YoY to Rs 419,108 crore as of September 30, 2024, from Rs 357,012 crore as of September 30, 2023.

Kotak Mahindra Bank and subsidiaries

PAT of Bank and key subsidiaries given below:

PAT (₹ crore) Q2FY25 Q2FY24

Kotak Mahindra Bank 3,344 3,191

Kotak Securities 444 324

Kotak Mahindra Life Insurance 360 247

Kotak Mahindra Prime 269 208

Kotak Asset Management & Trustee Company 197 124

Kotak Mahindra Investments 141 126

Kotak Mahindra Capital Company 90 27

BSS Microfinance 16 108

"Kotak Mahindra Bank's financial results for the quarter ending September 30, 2024, presented a mixed bag. The bank's net profit growth came out to be subdued largely due to higher provisions and nominal growth in its net interest income. The bank's asset quality remains a concern at this juncture as there were higher fresh slippages and lower upgradation and recoveries. However, the significant compression in NIMs is a concern, even though they remain better in the current high-interest rate environment. This compression is due to the rise in high-cost of deposits, an industry-wide trend that Kotak Mahindra Bank hasn't been immune to. The increasing reliance on these high-cost deposits is squeezing margins, creating a challenging scenario for the bank," said Manish Chowdhury, Head of Research, Stoxbox.

"On a positive note, the Bank has made notable progress on core banking resilience, business continuity action plan, cyber security and digital payments frameworks. External auditor fully engaged in validating items actioned upon by the bank. Kotak Mahindra AMC, the bank’s asset management subsidiary, has been impressive. The growth in AUM, driven by new equity NFO and an increase in SIPs, indicates strong investor confidence and effective management of the funds. Looking ahead, the bank faces significant challenges," he added.

Hormuz blockade: Trump says NATO allies refused to join US military ops against Iran

Hormuz blockade: Trump says NATO allies refused to join US military ops against Iran A decade-old idea returns: Arvind Panagariya backs electric cooking as LPG tightens

A decade-old idea returns: Arvind Panagariya backs electric cooking as LPG tightens Where Gen Z wants to work and why in 2026

Where Gen Z wants to work and why in 2026 BT EXPLAINER: Why Indian basket crude oil at $143 a barrel is more expensive than Brent and WTI

BT EXPLAINER: Why Indian basket crude oil at $143 a barrel is more expensive than Brent and WTI 'Iran posed no imminent threat': US counterterror chief Joe Kent quits over Iran war

'Iran posed no imminent threat': US counterterror chief Joe Kent quits over Iran war LPG Shortage Hits UP As Vendors Turn To Coal Bhattis, Raising Pollution Concerns

LPG Shortage Hits UP As Vendors Turn To Coal Bhattis, Raising Pollution Concerns West Asia War Impact: Markets, Crude & What Investors Should Do

West Asia War Impact: Markets, Crude & What Investors Should Do IT Stocks Fall Deep: Value Opportunity Or Value Trap?

IT Stocks Fall Deep: Value Opportunity Or Value Trap? Gold Vs Silver: Long-Term Investment Strategy Explained

Gold Vs Silver: Long-Term Investment Strategy Explained ₹19,000 Crore Via Minimum Balance Charges? Raghav Chadha Questions Banks

₹19,000 Crore Via Minimum Balance Charges? Raghav Chadha Questions Banks CPSE ETF likely to rise 25% in a year, says Ashish Chaturmohta

CPSE ETF likely to rise 25% in a year, says Ashish Chaturmohta EV incentives coming? Tata Motors PV, TVS, Ather, M&M shares among likely beneficiaries

EV incentives coming? Tata Motors PV, TVS, Ather, M&M shares among likely beneficiaries Sensex jumps 1,507 pts in 2 days, Nifty tops 23,550; will stock market extend gains on March 18?

Sensex jumps 1,507 pts in 2 days, Nifty tops 23,550; will stock market extend gains on March 18? US average diesel prices cross $5 a gallon as West Asia war tests global economy

US average diesel prices cross $5 a gallon as West Asia war tests global economy Adani Enterprises says NCLT approves resolution plan for Jaiprakash Associates

Adani Enterprises says NCLT approves resolution plan for Jaiprakash Associates