Elara said rupee weakness could help pharma, CDMO, textiles, IT services and upstream oil & gas companies. (AI-generated image)

Elara said rupee weakness could help pharma, CDMO, textiles, IT services and upstream oil & gas companies. (AI-generated image)Elara Securities, in its latest analysis of Nifty earnings since 2009 covering 65 quarters, said rupee depreciation has supported reported sales more consistently than earnings quality. The brokerage added that the final impact on earnings depends on cost pass-through, import intensity and balance sheet exposure.

On Thursday, the domestic currency was trading 4 paise lower at 96.30 against the greenback, down for the fourth straight session. According to Elara's strategy note, in sharp depreciation phases, defined as annual rupee weakness of more than 5 per cent, median Nifty50 sales growth rises to 14.9 per cent, aided by inflation and pricing action. Profit after tax growth, however, lags at 11.6 per cent, compared with 16.8 per cent during phases of rupee appreciation, the broking firm said.

Elara said a weak rupee can flatter nominal growth, but crude prices, imported inputs, freight costs, forex debt servicing and delayed pass-through absorb part of the benefit before it reaches profit after tax. It said that in past sharp-depreciation phases, energy, consumer staples and financials showed better PAT conversion, while IT retained top-line translation support but PAT lagged sales.

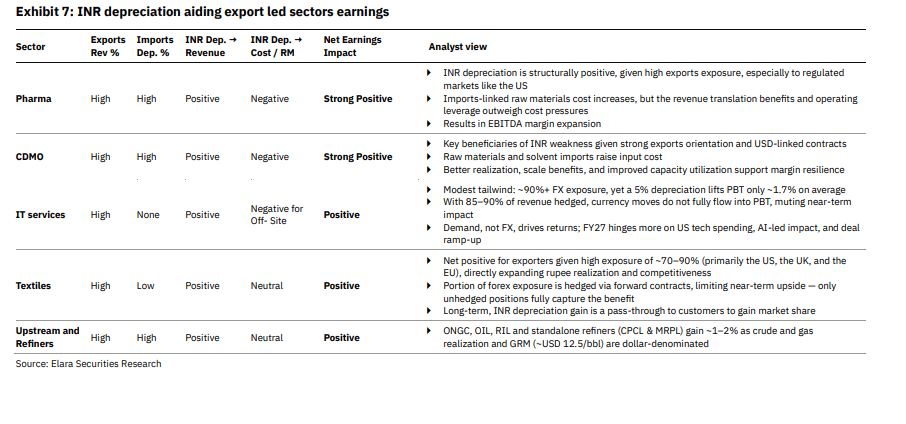

"The Nifty forex sensitivity analysis shows weak INR beneficiaries are not simply the highest exporters, but companies where currency gains flow through P&L after hedges, imported cost, and FX liabilities. We see two set of beneficiaries: exports-led beneficiaries: pharma, CDMO, IT services, textiles, upstream & refiners; realization- and pricing-led beneficiaries: steel, aluminium, and automobile," it said.

It said the ongoing rupee depreciation cycle may not replicate the earlier trend exactly.

"The US-Iran truce and Brent below $75/bbl reduce probability of an extreme cost shock, but two consecutive years of above-trend rupee depreciation means restocking at higher landed cost can still pressure Q1-Q2FY27 margin," it said.

Stocks and sectors to watch

Elara said rupee weakness could help pharma, CDMO, textiles, IT services and upstream oil & gas companies.

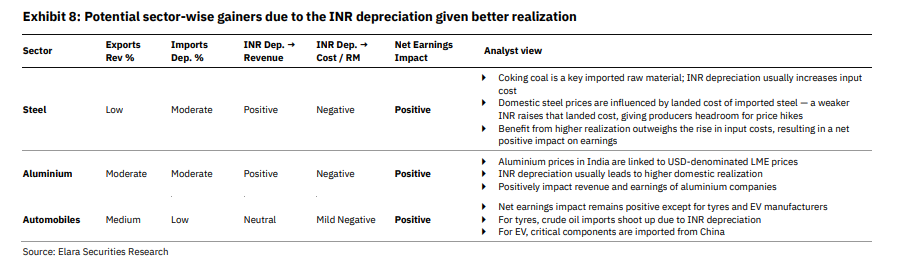

Elara also sees realisation- and pricing-led benefits for companies whose revenues are derived in the domestic market but whose prices track global and landed cost, as a weaker rupee lifts realisation to offset higher input cost. These include steel, aluminium and automobile companies.

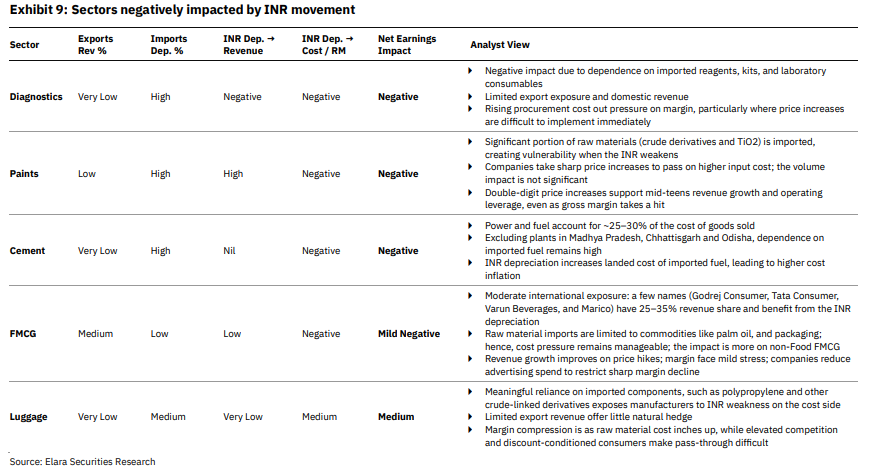

The brokerage added that consumer discretionary, healthcare and materials may see sharper slippages, reflecting either imported-cost pressure, weak pass-through or sector-specific earnings headwinds. Diagnostics, paints, cement, FMCG and luggage are among the sectors where meaningful imported inputs and limited immediate pass-through can lead to margin compression, the brokerage said.

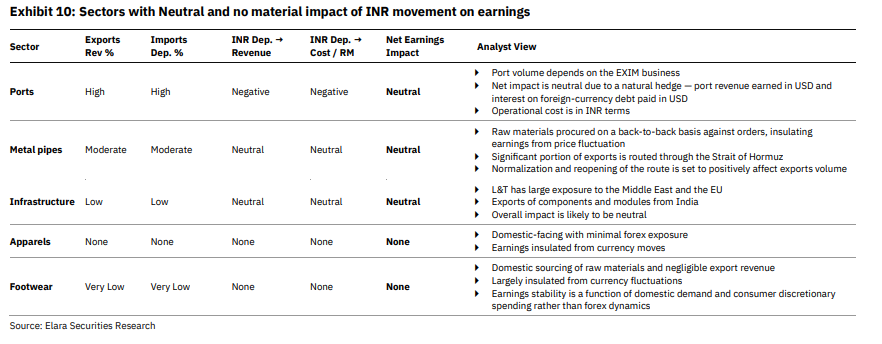

Meanwhile, ports, metal pipes, infrastructure, apparel and footwear offer a natural dollar revenue-cost hedge, or minimal forex exposure altogether.

OnePlus likely to exit India by 2027 amid Oppo’s restructuring plans

OnePlus likely to exit India by 2027 amid Oppo’s restructuring plans RIL Q1 results 2026: Jio may add 70-95 lakh subscribers; Retail to log healthy growth

RIL Q1 results 2026: Jio may add 70-95 lakh subscribers; Retail to log healthy growth 'When you set ₹5 crore goal, you...': Zerodha's Nithin Kamath recalls when he wanted to retire in Goa

'When you set ₹5 crore goal, you...': Zerodha's Nithin Kamath recalls when he wanted to retire in Goa Forget petrol! Why this ₹80/kg cow dung fuel is becoming India's latest energy bet

Forget petrol! Why this ₹80/kg cow dung fuel is becoming India's latest energy bet Thailand back to being visa-free for Indians, but you will still need this document: Check details

Thailand back to being visa-free for Indians, but you will still need this document: Check details ₹100 Crore TN Palani Temple Land Row: FIR Filed After 1.4 Acres Registered To Private Buyers

₹100 Crore TN Palani Temple Land Row: FIR Filed After 1.4 Acres Registered To Private Buyers Government Revises Windfall Tax: Impact On ONGC, HPCL, BPCL & Oil Prices

Government Revises Windfall Tax: Impact On ONGC, HPCL, BPCL & Oil Prices Arunachal Floods: Over 1 Lakh Affected, Roads Collapse, Relief Race Intensifies

Arunachal Floods: Over 1 Lakh Affected, Roads Collapse, Relief Race Intensifies Seafood Exporters Expect UK-Driven Export Growth Ahead

Seafood Exporters Expect UK-Driven Export Growth Ahead India’s First Hydrogen Train: PM Modi To Flag Off 10-Coach Green Rail On July 17

India’s First Hydrogen Train: PM Modi To Flag Off 10-Coach Green Rail On July 17 Rupee fall: 65 quarters of Nifty earnings since 2009 reveal stocks to watchRIL Q1 results 2026: Jio may add 70-95 lakh subscribers; Retail to log healthy growth

Rupee fall: 65 quarters of Nifty earnings since 2009 reveal stocks to watchRIL Q1 results 2026: Jio may add 70-95 lakh subscribers; Retail to log healthy growth Dixon Technologies shares rise 7%, up 50% from 52-week low; here's why

Dixon Technologies shares rise 7%, up 50% from 52-week low; here's why Wipro, TechM shares gain ahead of Q1 results today: Earnings preview

Wipro, TechM shares gain ahead of Q1 results today: Earnings preview  Hindalco Industries, among FIIs' favourites, gets a fresh price target from Kotak; here's why

Hindalco Industries, among FIIs' favourites, gets a fresh price target from Kotak; here's why