Stock ideas: CLSA says India sending contra buy signal, shares top underdog shares to buy

Stock ideas: CLSA says India sending contra buy signal, shares top underdog shares to buy

Stocks to buy: Foreign brokerage CLSA called stocks such as ONGC and DLF as underdogs. It also likes NTPC. On ONGC, CLSA said the upstream stock is pricing in a Brent crude price lower than the current price.

ShareCalling NTPC a decadal growth opportunities, CLSA sees 18 catalysts for NTPC to outperform in 2025, a fourth year running. s of RattanIndia Power surged 7.27 per cent to Rs 11.94 on Friday, with its market capitalization hitting Rs 6,400 crore mark.

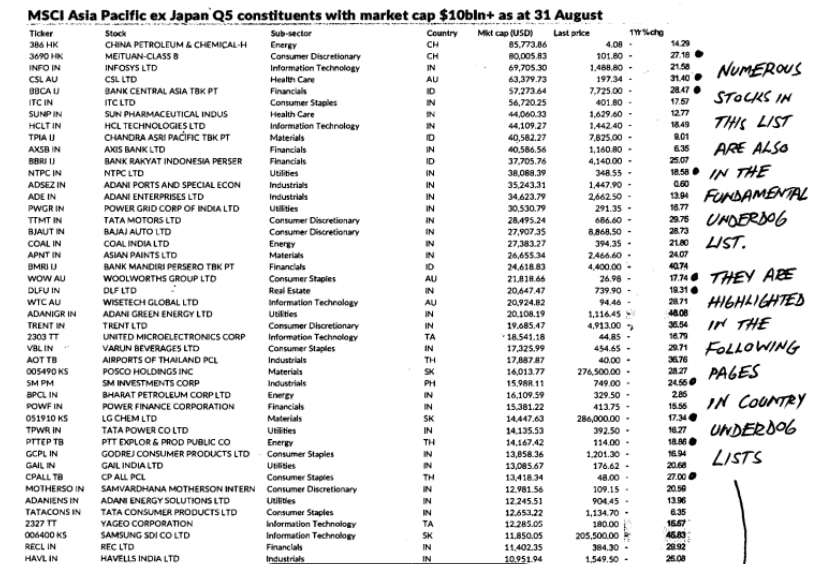

CLSA in its India strategy note said India's relative valuation is at four-year low, saying sentiment as suggested by its India bull bear index has fallen into extreme bearish zone at 10.1 per cent bullish suggesting a contra signals. The foreign brokerage called stocks such as ONGC and DLF as underdogs. It also likes NTPC.

Advertisement

In the case of ONGC, CLSA said the upstream stock is pricing in a Brent crude price lower than the current price, which it believes have a limited downside given a big increase in OPEC supply is more or less over. The ONGC management's confident commentary on driving strong production growth over the next three years is interesting, CLSA said, adding that ONGC continued to offer an attractive dividend yield of 6 per cent, one of the highest among Indian largecap stocks. CLSA said ONGC is trading in line with its historical average PE and 20 per cent below the global peer average PE and that of Oil India. It finds ONHC attractive in the context of promising production growth prospects. The brokerage suggested a target price of Rs 320 on the stock.

Advertisement

Source: CLSA

Source: CLSA

Calling NTPC a decadal growth opportunities, CLSA sees 18 catalysts for NTPC to outperform in 2025, a fourth year running. NTPC is back in a deep-value zone, trading at a 10 times FY27CL EPS (ex-value of its holding in NTPC Green) with a 3 per cent dividend yield (FY26CL),) which is 2 9 times the Nifty. CLSA said all of NTPC's businesses have option value as it is a market leader with a 24 per cent share of the third-largest power market in the world transitions.

CLSA suggested a target of Rs 459 on the stock. It sees upside risk to the target. "This is as it greens its energy mix with its lofty 60GW of non-fossil energy (NFE) goal by FY32 but also as it drives the decarbonisation of the industry with Its green molecules. We forecast 45 per cent EPS & 230 bps ROE growth over FY25-27. We see NTPC as back in deep-value zone," it said.

Advertisement

CLSA said DLF's housing portfolio has over-shadowed its annuity portfolio over the past four years, which is now the largest among all developers in India. DLF targets annual rental Income to grow from Rs 5,100 crore in FY25 to over Rs 10,000 crore by FY30.

"DLF is already generating significant cash flow in both its housing and rental portfolios. More importantly, the scale and stickiness of rental ash flow significantly _ hedges against the cyclicality of the housing portfolio. We believe DLF is better placed than peers due to its higher margin and OCF, its lower spending on land, Its large, growing rental portfolio, and its net cash balance sheet. We reiterate our HC O-PF rating," CLSA said.

"Given a robust rental growth outlook and steady growth in residential presales, we believe DLF can deliver an annualized return of 18 per cent over the next five-years. We estimate the contribution of rental business to rise from 21 per cent in our 1-year SOTP of Rs 1,025/share to 28 per cent in our FY30 estimated value of Rs 1,540/share, and is reassuring for its long-term valuation," CLSA said.

Disclaimer: Business Today provides stock market news for informational purposes only and should not be construed as investment advice. Readers are encouraged to consult with a qualified financial advisor before making any investment decisions.

ShareCalling NTPC a decadal growth opportunities, CLSA sees 18 catalysts for NTPC to outperform in 2025, a fourth year running. s of RattanIndia Power surged 7.27 per cent to Rs 11.94 on Friday, with its market capitalization hitting Rs 6,400 crore mark.

ShareCalling NTPC a decadal growth opportunities, CLSA sees 18 catalysts for NTPC to outperform in 2025, a fourth year running. s of RattanIndia Power surged 7.27 per cent to Rs 11.94 on Friday, with its market capitalization hitting Rs 6,400 crore mark.

")