Jefferies upgraded JSW Steel, but prefers Tata Steel, mainly on valuations. For Tata Steel, the target stands at Rs 200, hinting at 23 per cent potential upside.

Jefferies upgraded JSW Steel, but prefers Tata Steel, mainly on valuations. For Tata Steel, the target stands at Rs 200, hinting at 23 per cent potential upside.  Jefferies upgraded JSW Steel, but prefers Tata Steel, mainly on valuations. For Tata Steel, the target stands at Rs 200, hinting at 23 per cent potential upside.

Jefferies upgraded JSW Steel, but prefers Tata Steel, mainly on valuations. For Tata Steel, the target stands at Rs 200, hinting at 23 per cent potential upside. Jefferies in its latest note on steel sector said India offers a bright spot in the world largely devoid of volume growth in commodities. The foreign brokerage said domestic steel companies may offer strong 8-10 per cent volume CAGR over FY25-27, with safeguard duty aiding profitability.

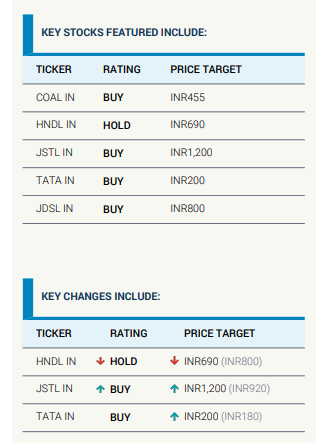

Jefferies called Tata Steel Ltd and Jindal Stainless as its preferred Buys. It also upgraded JSW Steel to 'Buy' from 'Hold', retaining its 'Buy' on Coal India. The broking firm downgraded Hindalco Industries to 'Hold' from 'Buy' on muted earnings growth and rising debt over FY25-27.

"We raise our FY25-27 EPS by 22-29 per cent for Tata Steel and by 23-24 per cent for JSW Steel on higher steel prices; our FY26-27 EPS for Tata Steel is 4-15 per cent above Street estimate. Steel stocks are trading

above last 10-year average PB, but valuations are likely to sustain, given healthy volume growth and potential margin expansion," Jefferies said.

This brokerage upgraded JSW Steel, but prefers Tata Steel, mainly on valuations. For Tata Steel, the target stands at Rs 200, hinting at 23 per cent potential upside. JSW Steel's target at Rs 1,200, Jindal Stainless' at Rs 800 and Coal India's at Rs 455 suggests up to 23 per cent upside ahead.

Jefferies said China's 2024 exports of carbon and stainless steel were the highest in a decade, which has been a drag on prices. But Asian conversion spread is 30 per cent below long term-average, and the 18-year history shows favorable risk-reward for owning steel stocks at spot spreads, Jefferies said.

On Hindalco, Jefferies said China has a net deficit in primary aluminum, which supported aluminum prices in 2024. But prices have fallen 9 per cent since mid-March due to tariff concerns.

"We cut Hindalco's FY26-27 EPS by 7-10 per cent on lower aluminum prices and lower Novelis volumes given concerns on US auto and specialty demand," Jefferies said. It believes the stock is not expensive, but is unlikely to perform given lackluster earnings growth and rising debt over FY25-27E. The brokerage suggested a target of Rs 690 on Hindalco.

On Jindal Stainless, the brokerage said it is a leader in India's fast-growing stainless steel (SS) market.

The company has lower Ebitda per tonne volatility and better balance sheet against Indian carbon steel players, it said.

"FY25 was a tough year for JDSL but a potential expansion in China SS spread can boost JDSL profitability. We expect 10 per cent volume and 21 per cent EPS CAGR with 17 per cent ROE over FY25-27E. Its 11x FY26E EV/Ebitda is reasonable given SS premium over carbon steel globally. We initiate on JDSL with Buy and Rs 800 target," it said.

have reduced their holdings in Rajesh Exports over the past three years.") Rajesh Exports ownership snapshot: LIC holds 10.8%; check FII stake and more

Rajesh Exports ownership snapshot: LIC holds 10.8%; check FII stake and more Gold, silver no longer just safe havens? Wealth managers back a new allocation strategy

Gold, silver no longer just safe havens? Wealth managers back a new allocation strategy has flagged container pendency that they said are adding to huge losses. (Representational photo)") Why are container train operators facing issues at Adani’s Mundra Port?

Why are container train operators facing issues at Adani’s Mundra Port? Mamata, Abhishek vs 'Asli TMC': How Trinamool Congress turned against itself in 2 weeks

Mamata, Abhishek vs 'Asli TMC': How Trinamool Congress turned against itself in 2 weeks From TikTok to trillions! How this Chinese man overtook Mukesh Ambani in Asia’s wealth race

From TikTok to trillions! How this Chinese man overtook Mukesh Ambani in Asia’s wealth race Retire At 60 With ₹7 Crore? Hard Facts About Inflation & Expenses

Retire At 60 With ₹7 Crore? Hard Facts About Inflation & Expenses EV & Power Capex: Aniruddha Sarkar's Hidden Stock Bets

EV & Power Capex: Aniruddha Sarkar's Hidden Stock Bets Retirement Planning Made Easy: SIP, NPS, PPF & EPF Strategy To Build Massive Wealth

Retirement Planning Made Easy: SIP, NPS, PPF & EPF Strategy To Build Massive Wealth Cabinet Clears ₹10,000 Cr ATF Fund To Shield Airlines From Fuel Shock

Cabinet Clears ₹10,000 Cr ATF Fund To Shield Airlines From Fuel Shock Section 301 Tariffs Could Hit Indian Exports Just As Trade Deal Nears Completion

Section 301 Tariffs Could Hit Indian Exports Just As Trade Deal Nears Completion India’s infrastructure opportunity is a multi-decade growth story: Adani Group

India’s infrastructure opportunity is a multi-decade growth story: Adani Group Adani Portfolio reports record FY26 capex of Rs 1.53 lakh crore; EBITDA hits all-time high

Adani Portfolio reports record FY26 capex of Rs 1.53 lakh crore; EBITDA hits all-time high Defence stock jumps over 30% in 2026 so far, up 9% today – Order win from BEL, Q4 results and more

Defence stock jumps over 30% in 2026 so far, up 9% today – Order win from BEL, Q4 results and more SpaceX IPO price out: Valuation, risks, growth explains — All what investors should know

SpaceX IPO price out: Valuation, risks, growth explains — All what investors should know Jain Irrigation, MSTC, Savita Oil shares rise up to 17%

Jain Irrigation, MSTC, Savita Oil shares rise up to 17%